US Equity and Economic Review: Don't Be Too Spooked By the Sell-Off (At Least, Not Yet), Edition

The US economy is bifurcated: manufacturing is in a mild recession while services are solidly expanding. The ISM manufacturing index printed below 50 for the second consecutive month with a reading of 48.2. New orders and production were also below 50, although exports orders expanded slightly. Only 6 of 18 industries are growing, while 10 of 18 are contracting. With the strong dollar, weak emerging economies and oil slowdown, these readings shouldn’t be surprising.

In contrast, the service sector continues to grow, with a top line reading of 55.3. Activity printed a very positive 58.7 while production was no less bullish at 58.2. 11 of 16 industries are growing. The report’s anecdotal comments are very uniformly strong:

- "Business continues to be strong for consulting/operational outsourcing of real estate operations." (Management of Companies & Support Services)

- "Professional and skilled craft labor is difficult to find." (Construction)

- "Continued downturn in global energy pricing has given way to reduced costs from vendors." (Mining)

- "We see continued spend demand higher than any months of this year; however, productivity reaches its peak and projects have to be carried over to 2016." (Professional, Scientific & Technical Services)

- "Holiday shopping volume is in line with forecast." (Retail Trade)

- "Currently very busy in the holiday rush season. Purchasing of supplies, postage & freight, and direct labor all more than double non-holiday periods." (Transportation & Warehousing)

- "The supply chain is faster than in previous years and equipment is more readily available." (Wholesale Trade)

- "Construction projects continue at a record pace." (Educational Services)

While it’s east to cherry-pick the manufacturing data to argue a recession is at hand, the case is still “wobbly.” Analysts can correctly argue services will keep the economy afloat for the time being.

US car sales were up 2% Y/Y and down 5% M/M. Doug Short offers this chart, which uses a 9 month moving average:

Bloomberg places these numbers in historical perspective:

By the time Tuesday’s reports conclude, analysts still predict sales will topple the annual American record set 15 years ago, buoyed by Americans’ renewed love of pickups and SUVs, cheap gasoline, easy credit and a strengthening labor market. Industrywide sales were forecast to exceed an 18 million sales rate for a record fourth straight month.

.....

A confirmed record for 2015 would mark a sixth straight year of growing U.S. sales, the longest streak since World War II. The surge is owed in part to buyers who were soothed by job and wage growth, falling gasoline prices and carmakers who upgraded their lineups and used discounts and cut-rate financing to draw shoppers to showrooms

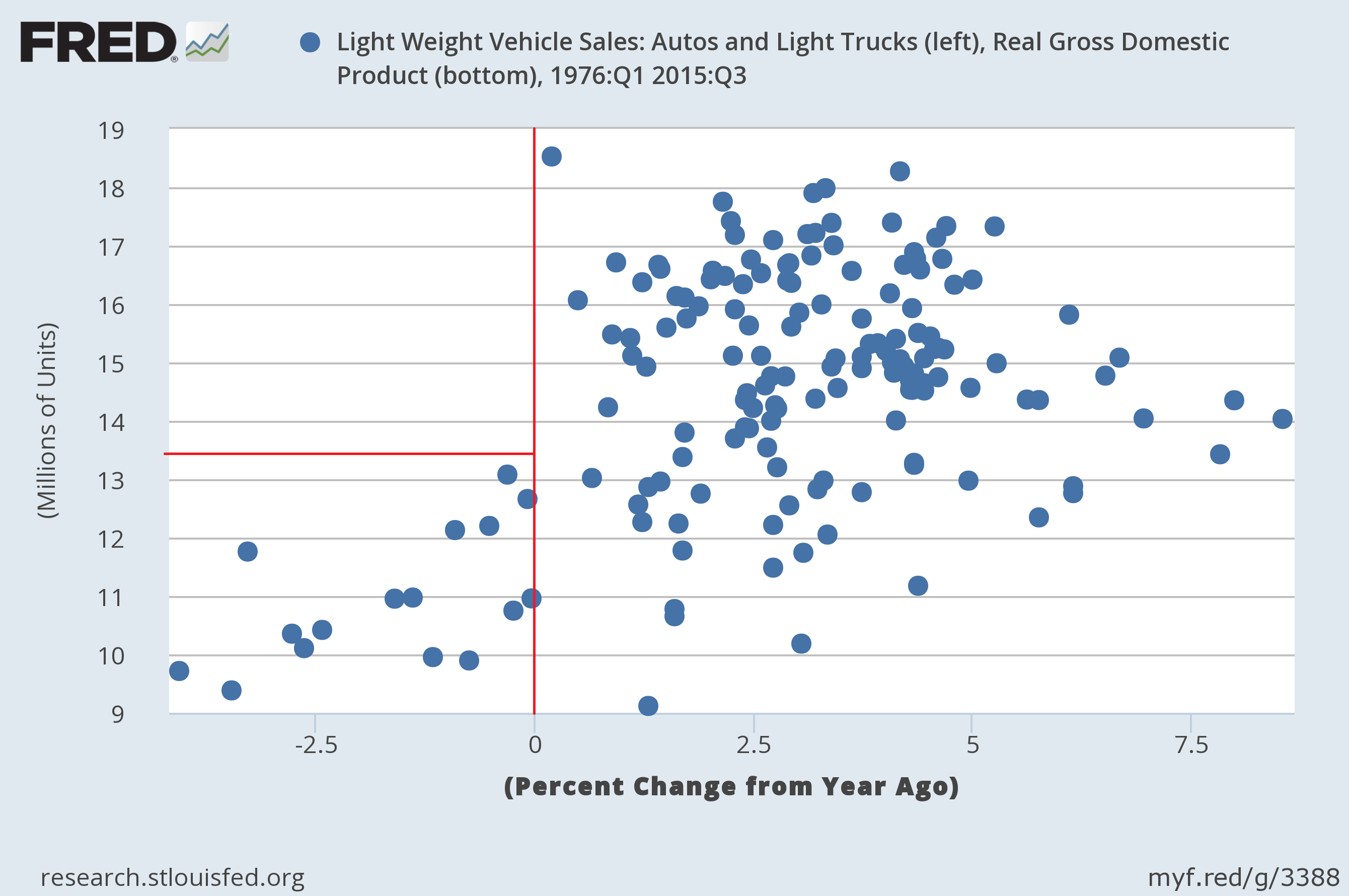

It’s difficult to understate the importance of these numbers. As the following scatter chart shows, auto sales have to be at a far lower level for there to by any talk of a recession:

Finally, the latest employment report was very positive, with a headlines number of 298,000. More importantly, the BLS revised the preceding two months higher by 50,000. Weak wage growth was the one weak point in the report. But all other points were positive.

The Atlanta Fed’s GDP Now Model is predicting 4Q GDP of .8%. The Moody’s GDP Nowcast is 1.4%. Both dropped sharply over the last few weeks. The Cleveland Fed’s yield curve prediction is 1.9%.

The Atlanta Fed’s Recession probability indicator shows a 13.3% recession probability; the NY Fed’s model is 3.56%.

Economic Conclusion: this week’s data was very encouraging, especially in light of the market volatility. While the shallow industrial recession continues, the service sector is growing. And with this sector a much larger percentage of the economy, it should be able to counter-balance industrial weakness. The US consumer’s record-setting appetite for durable goods is very positive. And the last jobs print of the year was very encouraging.

Market Update: The market is still expensive. The current and forward PEs of the SPYs and QQQs are 22.95/23/25 and 17.44/20.04, respectively. And there is little reason to argue for stronger revenue growth. From Factset:

The estimated revenue decline for Q4 2015 is -3.3%. If this is the final revenue decline for the quarter, it will mark the first time the index has seen four consecutive quarters of year-over-year revenue declines since Q4 2008 through Q3 2009. Six sectors are expected to report year-over-year growth in revenues, led by the Telecom Services and Health Care sectors. Four sectors are expected to report a year-overyear decline in revenues, led by the Energy and Materials sectors.

Zacks also sees lower revenue growth of 4.7%. And no one is calling for a meaningful increase. Should these forecasts be accurate, then we can expect more downward pressure on stock prices.

For regular readers of this column, last week’s sharp sell-off shouldn’t be surprising. For the last six months, I’ve noted the following:

- The market is expensive, meaning it needs additional revenue growth to continue rallying.

- But we’re entering our fourth quarter of overall revenue declines.

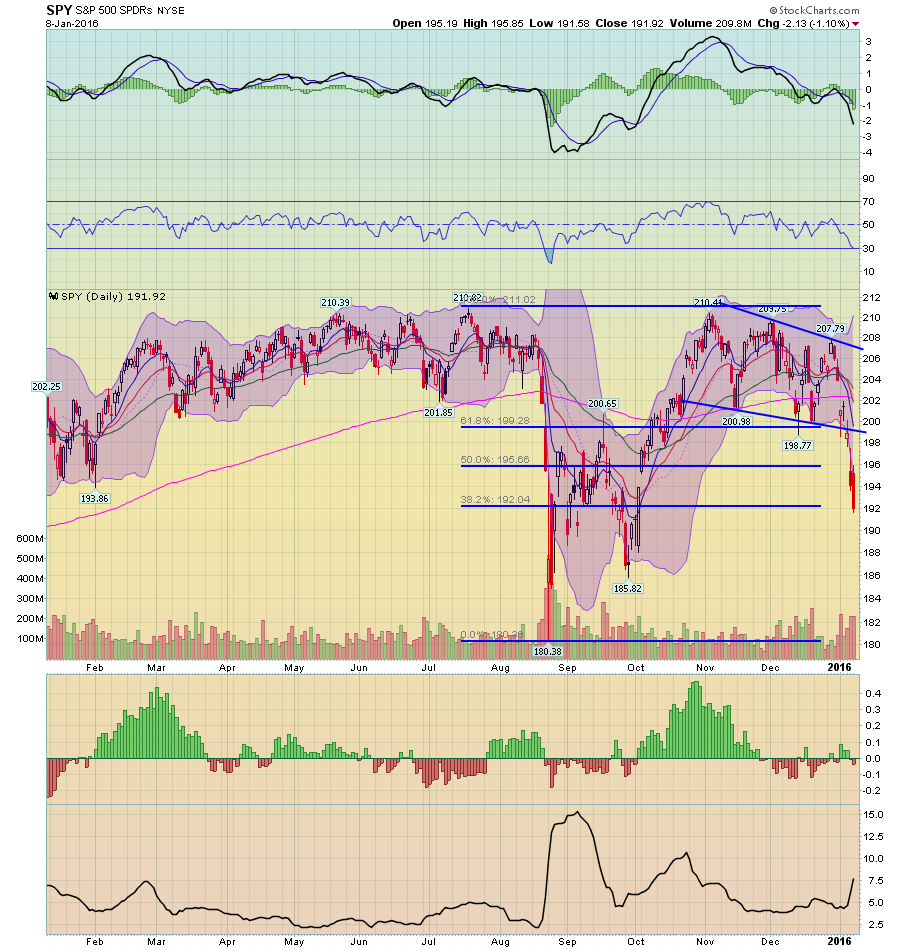

- Earlier this year, the SPYs couldn’t move beyond the 210-212 price level.

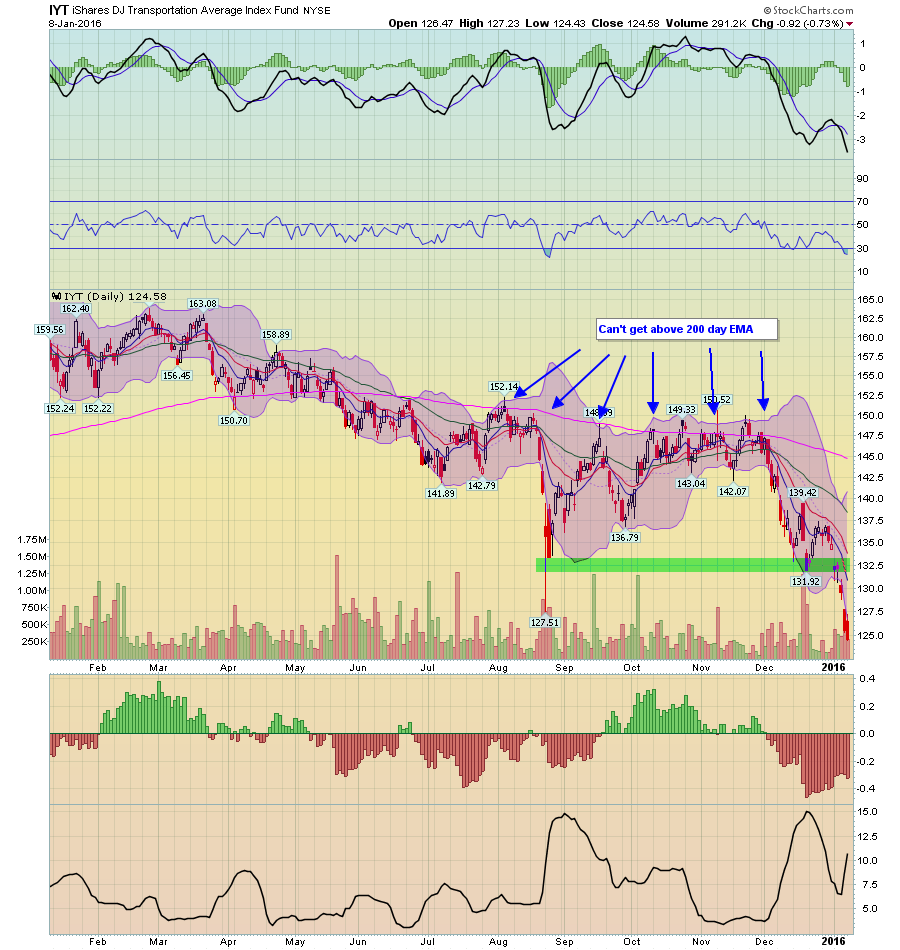

- The transports have moved lower for the last six months

- Two months ago, the IWMs couldn’t maintain momentum above their 200 day EMA

- Sector performance recently turned very defensive, with health care, staples and utilities gaining.

All the market needed was a selling catalyst, which the Chinese market provided.

Let’s look at the technicals, starting with the IWMs (Russell 2000):

Prices have been below the 200 day EMA since early August. In mid-August, they rallied above this indicator twice, but couldn’t maintain their momentum. Last week, prices fell through support in the mid ~106s. The index is down 18.63% from its absolute 1 year high.

The IYTs fell below the 200 day EMA in mid-May. Starting in mid-August, prices tried to rally above the 200 day EMA 7 times, but couldn't make it above that technical landmark. The index is down 23% from its absolute 1-year high.

The QQQs were the best performing average until last week, when they fell through the technically important level of ~109. Now prices are below the 200 day EMA.

The SPYs – which are only down ~9% from their absolute 1-year highs – are below their 200 day EMA. They also fell through the support of their downward sloping price channel.

Conclusion: Overall, this week’s sell-off isn’t surprising in light of the weakening technical and fundamental environment. Prices for riskier equities (IWMs) have been weak for nearly 6 months. Transports – whose price action should theoretically confirm broader upward price movement – have been in a bear market (below the 200 day EMA) for 7 months. The SPYs couldn’t get above the 110-112 price level for all of 2015. And now the QQQs have fallen below their 200 day EMA. And the “average” stock is now in a bear market. Turning to the fundamentals, the market has been expensive for over a year. Combine that with near year-long stalling revenue growth, and you have the recipe for a sell-off. All the market needed was a catalyst, which China provided. But, despite the problems, the US economy is still in decent shape. At this point, between consumer spending and housing, there is more than enough strength to keep from falling into a recession.

(c) Hale Stewart