This week’s big bond market news was the release of the December Meeting Minutes. Let’s begin by looking at the Fed’s then current view of the US economy:

Total nonfarm payroll employment expanded at a faster monthly rate in October and November than in the third quarter. The unemployment rate ticked down to 5.0 percent in October and remained at that level in November; over the 12 months ending in November, the unemployment rate fell 3/4 percentage point. Both the labor force participation rate and the employment-to-population ratio increased slightly, on net, over October and November. The share of workers employed part time for economic reasons was flat, on balance, in recent months after declining considerably over the previous year. The rates of private-sector job openings, hires, and quits were little changed in October from their average levels in the third quarter. Recent measures of the gains in labor compensation were mixed: Over the four quarters ending in the third quarter, compensation per hour in the business sector advanced at a strong 3-1/2 percent rate, while the employment cost index rose at a more moderate 2 percent pace. Average hourly earnings for all employees increased 2-1/4 percent over the 12 months ending in November.

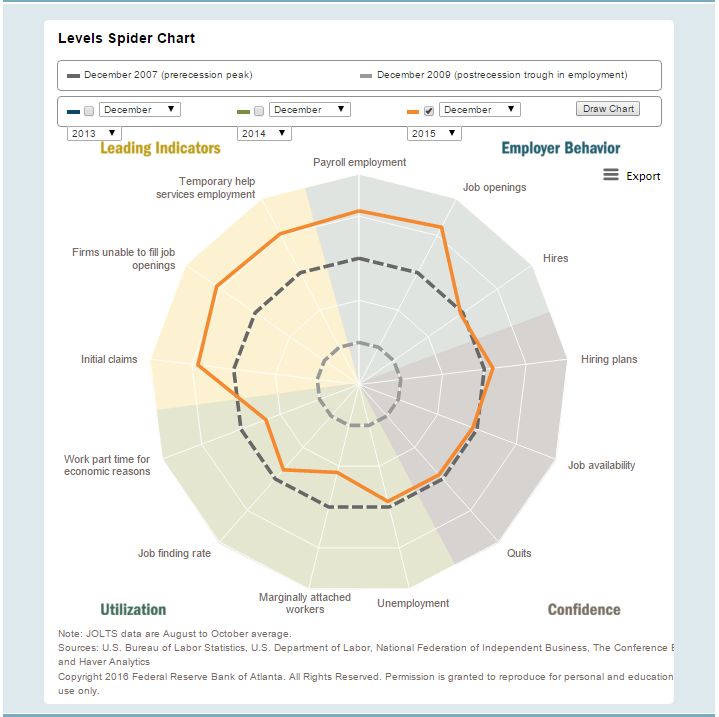

Clearly the 5% unemployment rate is the primary number in the above paragraph. But while this statistic forms the core of their analysis, they use a broader range of metrics, including the labor force participation rate and the employment to population ratio, to flesh out their thinking. This is a new and key development. This Spider Chart from the Atlanta Fed best shows the diverse data sets used in the Fed’s analysis:

The 5% unemployment rate alone is enough for the Fed to argue the economy is at full employment, thereby complying with half their dual mandate. While some measures of labor utilization remain a bit weak, the counter-argument isn’t strong enough to outweigh the importance of the 5% unemployment rate.

Manufacturing production increased in October, although output in the mining sector continued to decrease. Automakers' assembly schedules and broader indicators of manufacturing production, such as the readings on new orders from national and regional manufacturing surveys, generally pointed to a slow pace of gains in factory output in the coming months. Information on crude oil and natural gas extraction through early December indicated further declines in mining output.

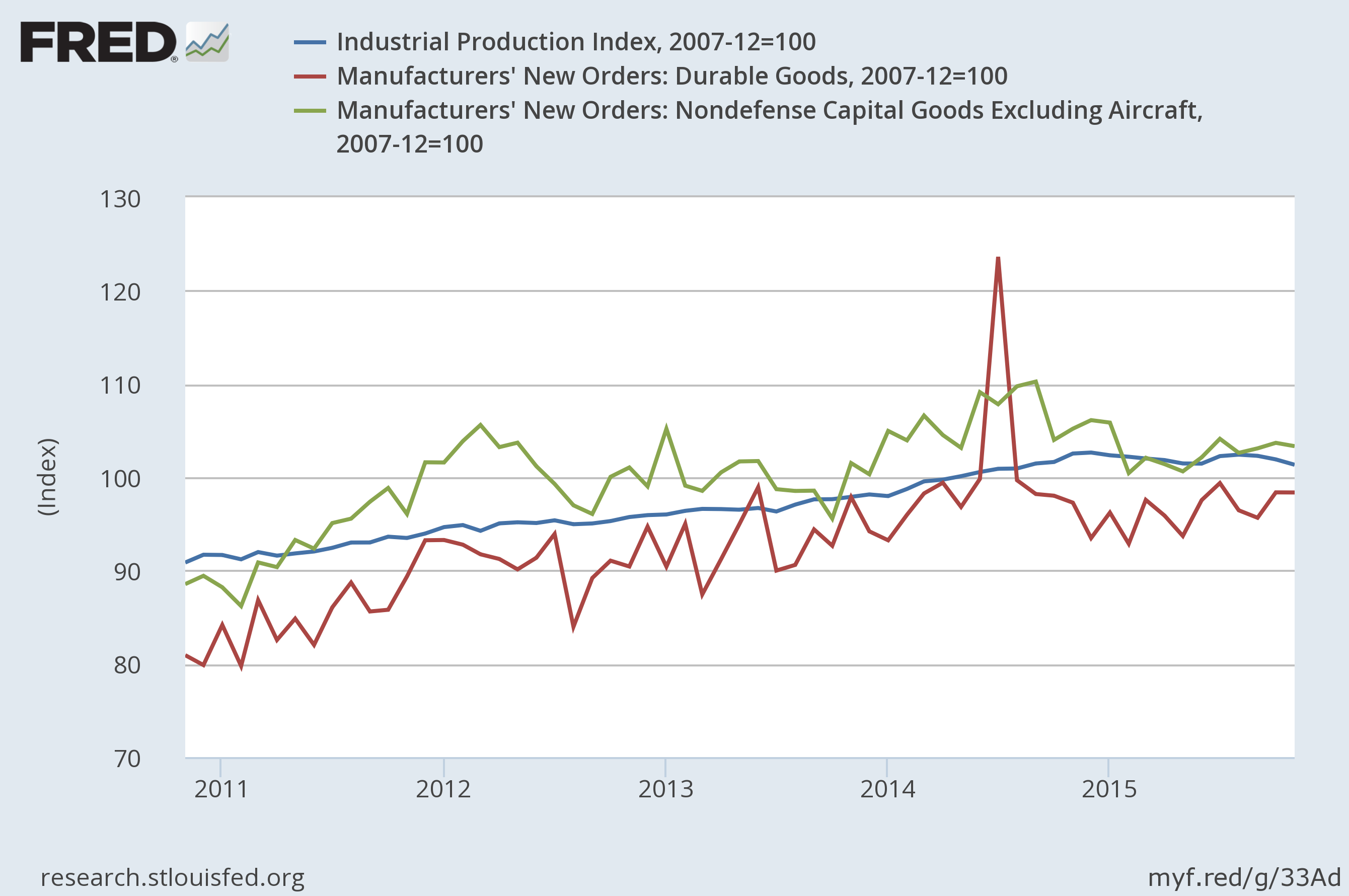

The shallow industrial recession is curiously absent from their discussion. Overall industrial production – an important coincident indicator – has stalled for the last year. New orders for durable goods flat-lined for a bit longer. And new orders for non-defense capital goods excluding aircraft is moving slightly lower:

These figures – even when considered together – don’t indicate we’re in a recession. The manufacturing sector can’t cause a recession by itself. But the duration and breadth of these numbers weakness is concerning.

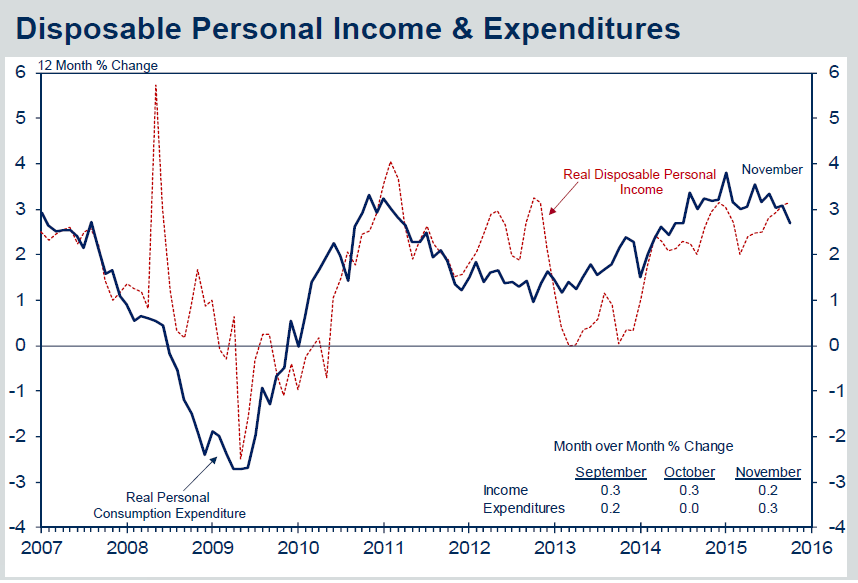

Real personal consumption expenditures (PCE) appeared to be rising at a solid rate in the fourth quarter. The components of the nominal retail sales data used by the Bureau of Economic Analysis to construct its estimate of PCE increased in October and moved up at a faster pace in November, while the rate of sales of light motor vehicles remained high. Household spending was supported by strong growth in real disposable income in September and October, and households' net worth was bolstered by recent gains in home values. In addition, consumer sentiment in the University of Michigan Surveys of Consumers improved a little in November and early December.

Although PCEs Y/Y rate of change is lower for his expansion, there is no denying the US consumer is holding up his end of the economic bargain by spending at a decent pace. Most important is the continual uptick in auto sales. Service spending is still positive. However, non-durable purchases are weak. But these don’t comprise a large percentage of PCEs. And looking at the overall level of PCEs, we see strong Y/Y growth:

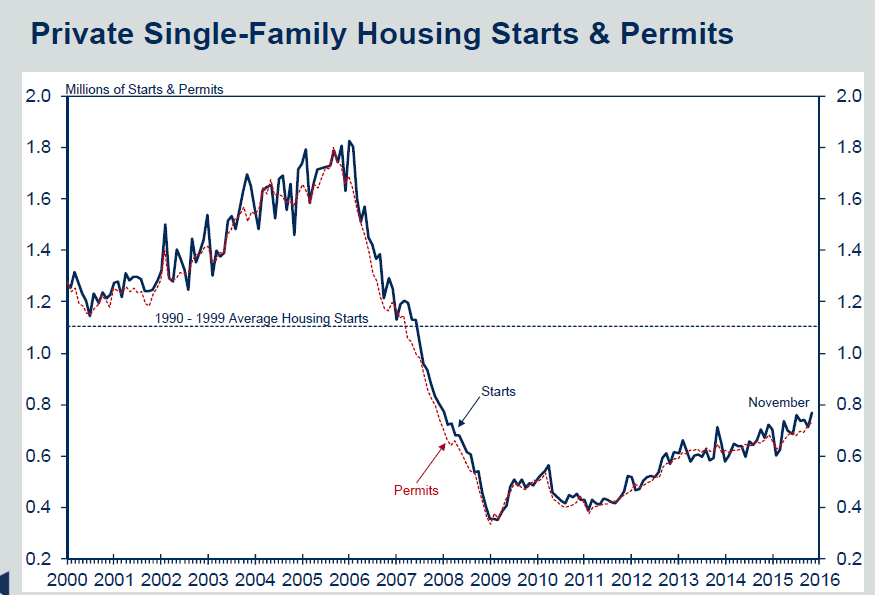

Recent information on activity in the housing sector was mixed. Starts of new single-family homes were somewhat lower in October than in the third quarter, although building permits moved up. Meanwhile, starts of multifamily units declined. Sales of new homes rose in October, while existing home sales decreased.

These are two of the most important data points in the US economy right now; their importance can’t be overstated. With both rising it’s nearly impossible to argue that a recession is on the horizon.

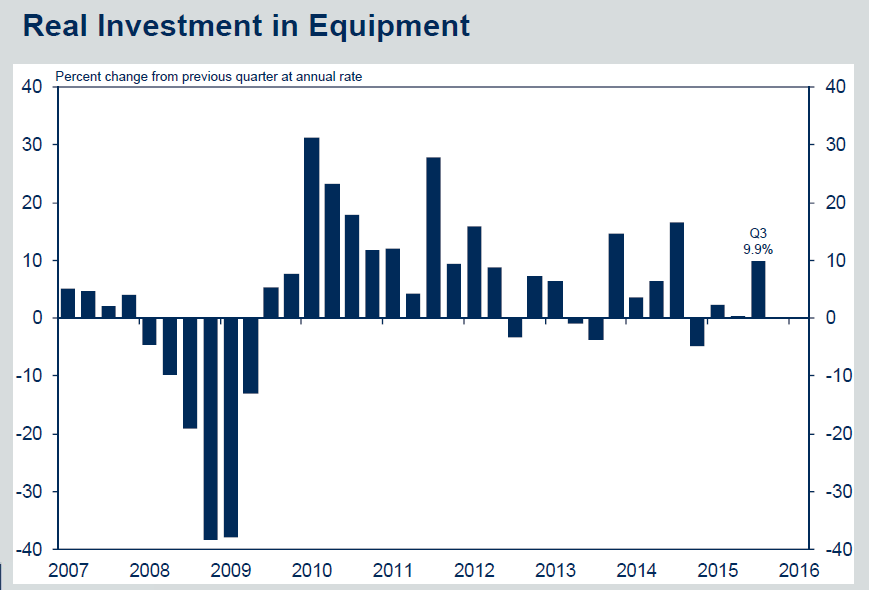

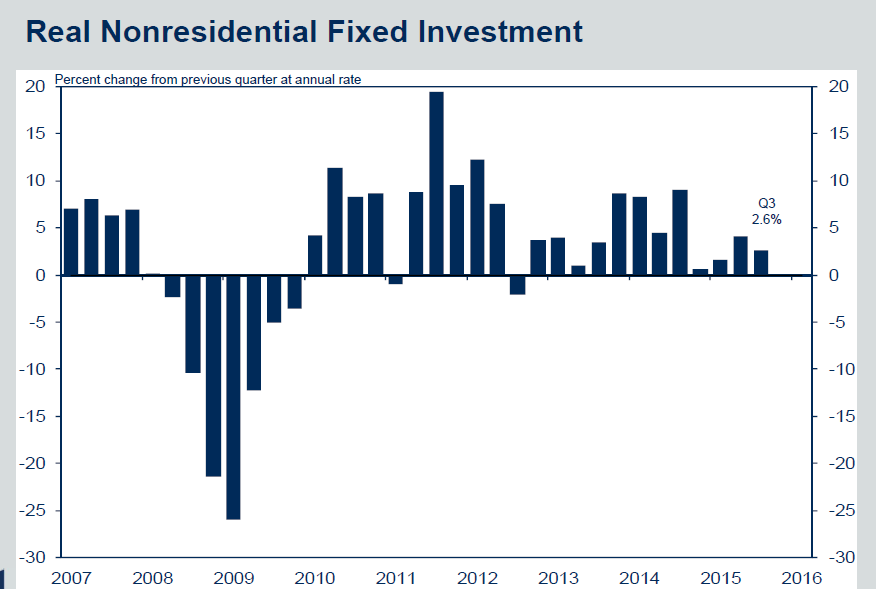

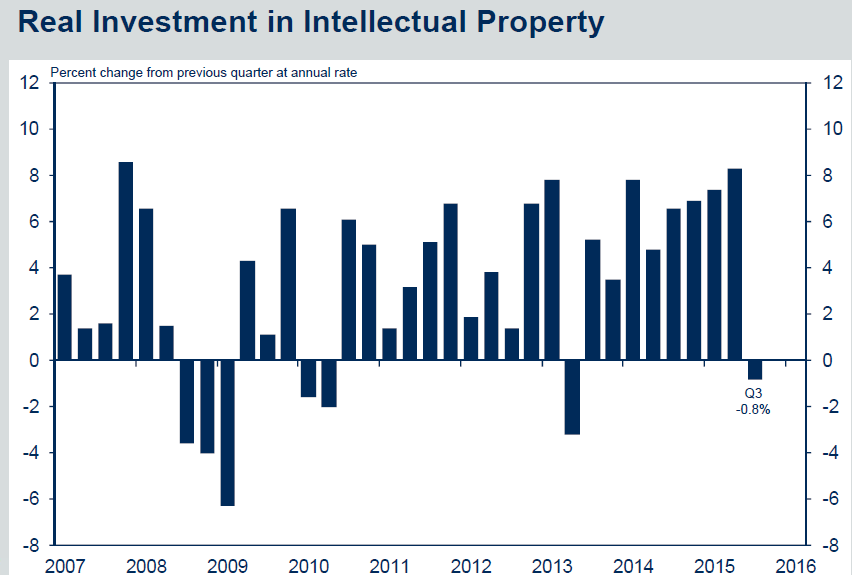

Real private expenditures for business equipment and intellectual property products increased at a solid pace in the third quarter, but business spending growth looked to be slowing somewhat in the fourth quarter. Nominal shipments of nondefense capital goods excluding aircraft edged down in October, although new orders for these capital goods continued to move up. Recent readings from national and regional surveys of business conditions were consistent with more modest increases in business equipment spending than in the third quarter. Firms' nominal spending for nonresidential structures excluding drilling and mining rose in October, although available indicators of drilling activity, such as the number of oil and gas rigs in operation, continued to fall through early December.

While fixed equipment investment increased 9.9% Q/Q in 3Q15, the preceding three quarters were fairly weak. Non-residential investment numbers were low for the last year. And intellectual property investment contracted on a Q/Q basis:

Like the industrial production numbers, the Fed appears to have a more bullish view of the business investment than a look at broader measures would indicate.

And like employment, the Fed is now using a broader number of inflation measures:

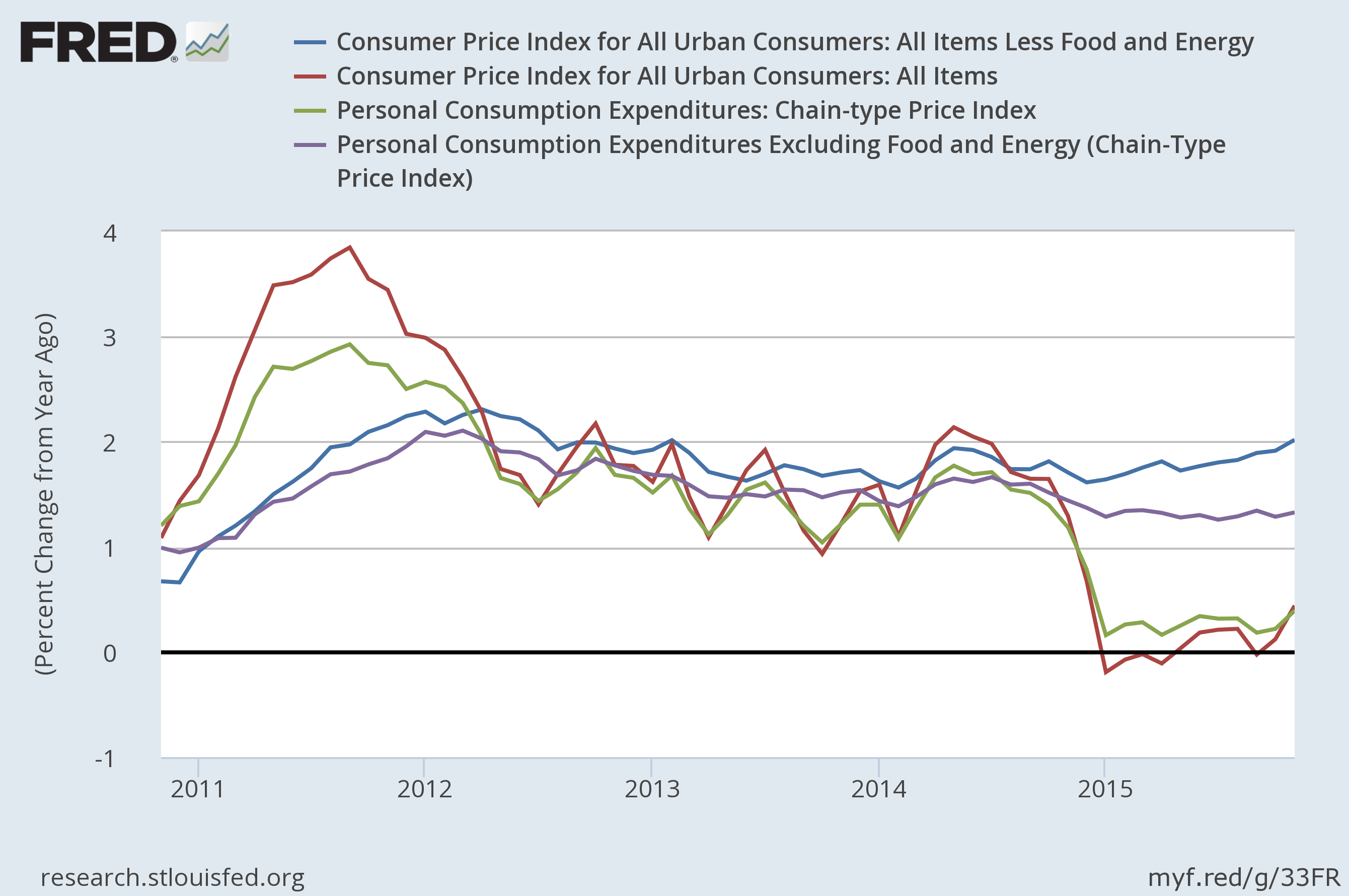

Total U.S. consumer prices, as measured by the PCE price index, rose only 1/4 percent over the 12 months ending in October, held down by large declines in consumer energy prices. Core PCE inflation, which excludes changes in food and energy prices, was 1-1/4 percent over the same 12-month period, partly restrained by declines in the prices of non-energy imported goods. Over the 12 months ending in November, total consumer prices as measured by the consumer price index (CPI) rose 1/2 percent, while core CPI inflation was 2 percent. Survey measures of expected longer-run inflation were relatively stable, although they showed some hints of having edged slightly lower: In November and early December, the Michigan survey measure continued to run somewhat below its typical range of the past 15 years, though historical patterns suggest that these relatively low readings may have reflected softness in total inflation and energy prices. The measures from both the Survey of Professional Forecasters for the fourth quarter and the Survey of Primary Dealers in December moved down slightly.

There are five different measures mentioned above: total and core PCEs, total and core CPI and several measures of inflation expectations. Let’s take a look at the CPI and PCE numbers:

Core PCE and CPI have consistently printed between 1.25% and 2% over the last year. The total numbers, however, are both near 0%. Obviously, the Fed believes that commodity prices will rebound, bringing the core numbers up to their 2% price target. Inflation expectations are clearly contained, as this chart of the different between the 10 year treasury and 10 year TIPS shows:

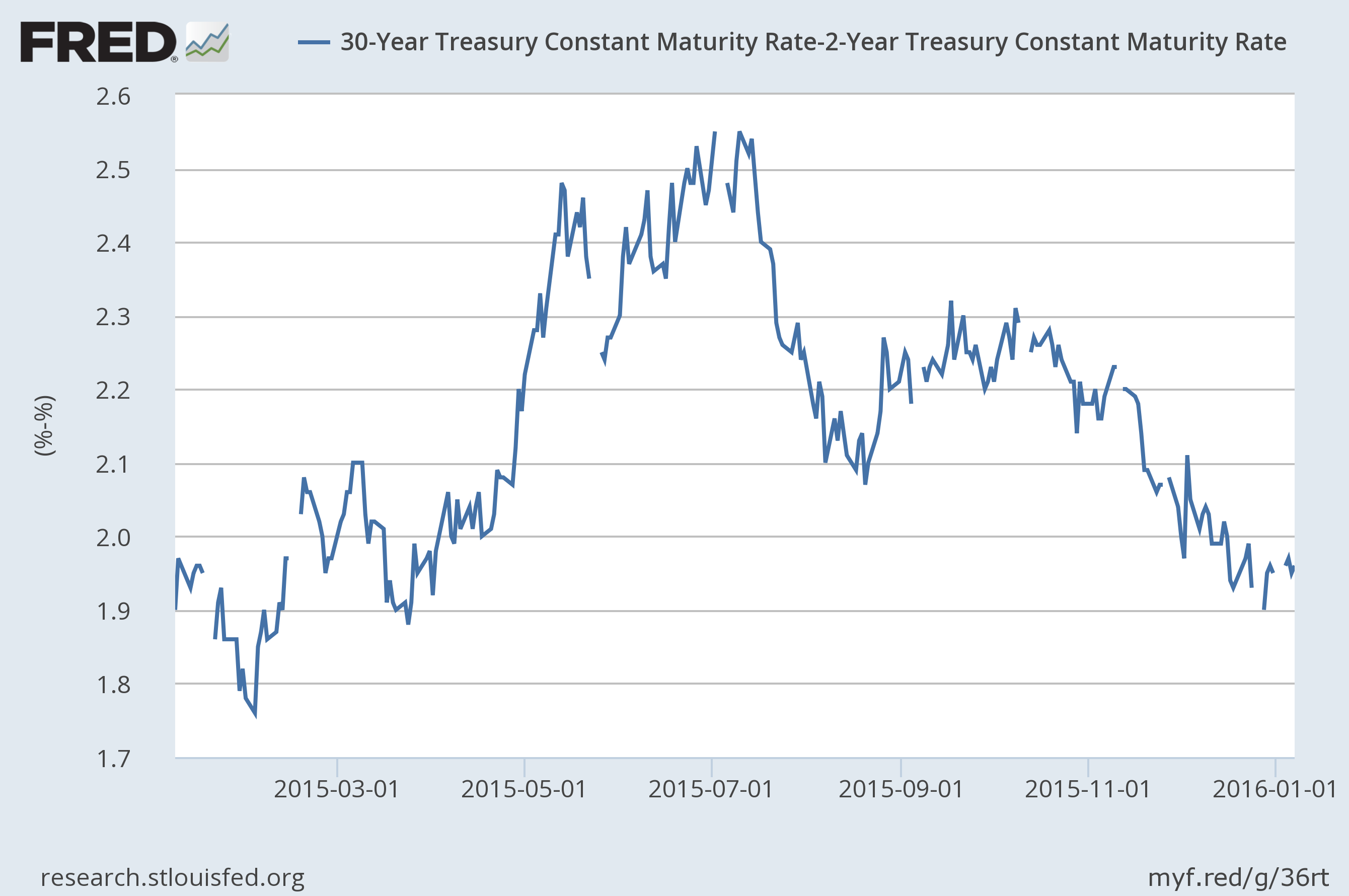

The treasury market does not share the Fed’s economic optimism:

The 30-2 yield spread has dropped nearly 50 basis points in the last six months. This shows a remarkable lack of confidence in growth prospects.

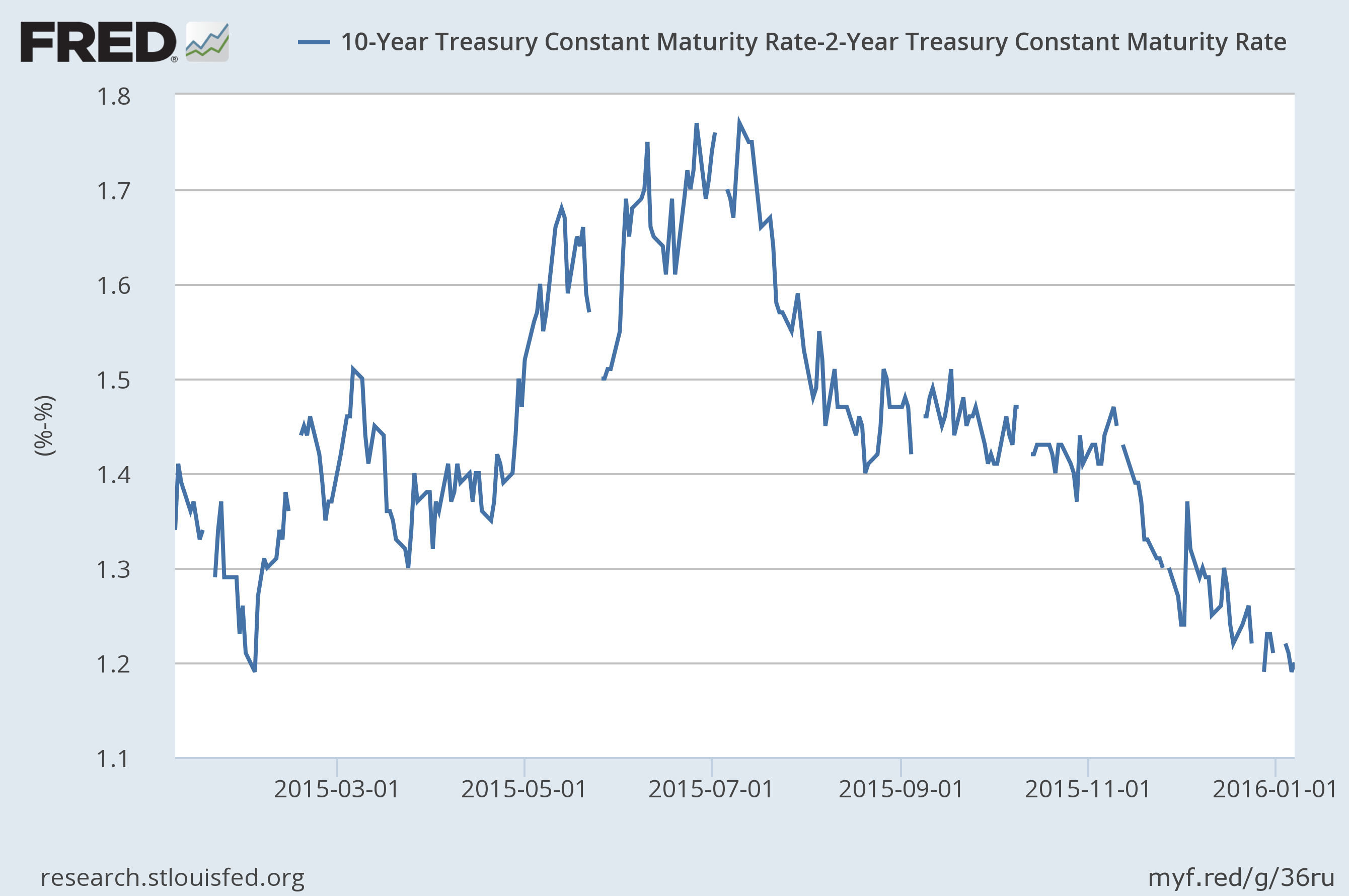

And the 10-2 spread is just as concerning:

It has dropped a little over 50 basis points over the same length of time.

If the bond market shared the Fed’s optimism, we’d be seeing yield spreads widen. We’re seeing just the opposite.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis