Despite the change to a new year, the primary problems of the world economy remain.

- Although China continues growing near 7%, recent numbers point to a slowdown.

- Commodity producers face lower demand for their raw material exports, lowering overall growth.

- Oil prices remain low thanks to a supply glut (see here and here).

- The causes of low inflation continues to confound central bankers.

- Overall global growth is weakening.

And now we have an added problem: the Chinese response to weaker domestic markets has been haphazard. From Bloomberg:

What does seem to worry investors is how deftly, or ineptly, Chinese authorities will manage a stock market that’s gone from boom to bust and back again more times in the past 12 months than most major peers do over the course of a decade. After policy makers took extreme steps to prop up shares last summer, analysts are struggling to gauge how Beijing will react to a renewed bout of volatility that threatens to weigh on business and consumer confidence.

The Financial Times adds this nuance:

The central issue is the classic dichotomy of the modern Communist Party as it seeks more market oriented policies but retains an inherent distrust of risk — leading to a reluctance to let markets be the final arbiter of either equity prices or foreign exchange rates.

This contradiction at the heart of the party’s economic and financial reforms was laid bare in August, when China’s central bank surrendered its power to set the renminbi’s “daily fix” against the US dollar wherever it wanted and instead tied it to the previous day’s close. The People’s Bank of China has since spent tens of billions of its foreign-exchange reserves in an effort to keep the currency from falling too sharply against the dollar.

The week started off poorly: Markit announced the tenth consecutive month of Chinese manufacturing contraction. Payrolls and demand (both domestic and international) declined while production dropped for 7 of the last 8 months. Although Chinese services expanded slightly, they printed their lowest reading in 17 months. And the composite reading was 49.4. Finally, another month of weak price pressures points to potential demand weakness.

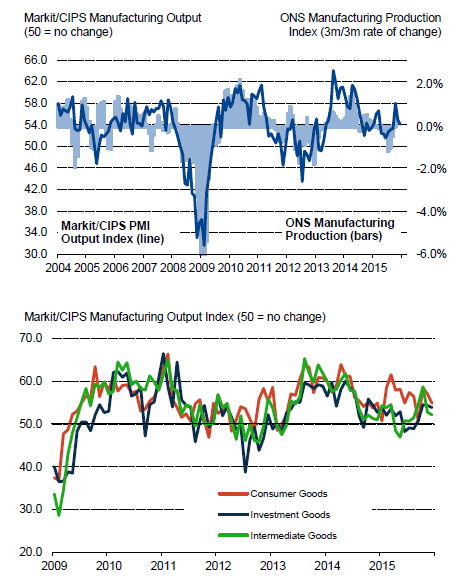

UK news was positive. The manufacturing PMI printed at 51.9, with overall production at 54. All three sectors contributed to growth:

Best of all, new export orders increased for the fourth consecutive month – which is impressive, considering the Sterling’s overall strength versus the euro:

The service sector number was a very positive 55.5 with new and outstanding business readings increasing.

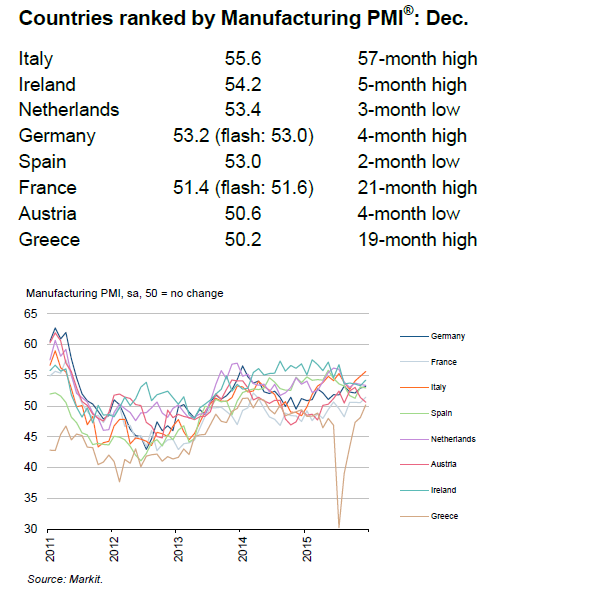

Markit’s EU data points to continued expansion. The EU’s composite reading was 54.3 with manufacturing reported at 52.3 – the highest since 4/14. All major countries’ manufacturing sectors (even Greece) are expanding:

Germany’s PMI was 53.2; new and export orders rose. Italy’s was the highest since 3/11. EU service sectors reported a solid headline number of 54.3, with an increase in new business and overall optimism. France was the only country whose service sector was contracting. Inflation, however, is still weak, with a .2% Y/Y reading. Unemployment continues to move lower, this time by .1% to 10.5%. However, retail sales were also lower buy .3% M/M.

Japan’s composite Markit reading was 52.2, with a manufacturing number of 52.6. New orders were the highest in 14 months, while production was the highest in 20 months. Export orders increased for the third consecutive month. Service sector growth was also positive, with a 51.5 reading. New orders were reported as “strong.” While neither reading highlights a “booming” economy, they do indicate one growing modestly. To that end, consider this analysis offered by Mr Takehiro Sato, Member of the Policy Board of the Bank of Japan:

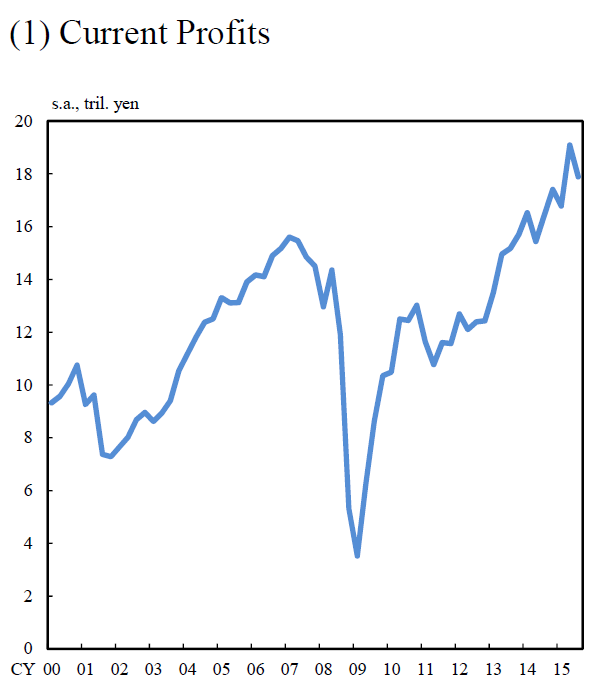

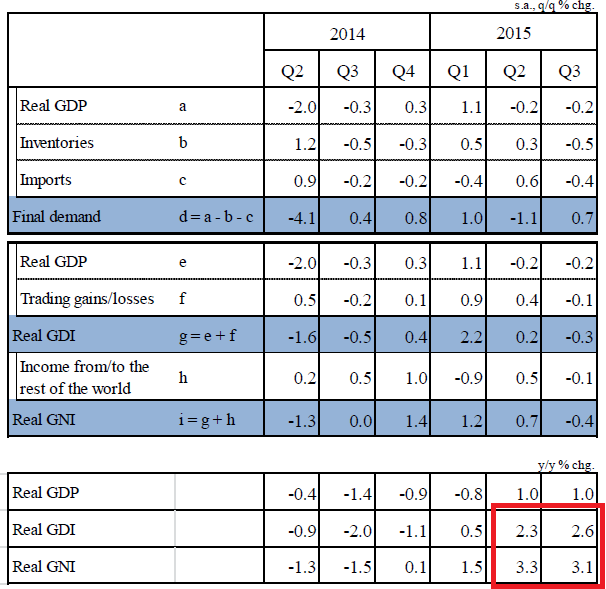

Given this situation, there are views, mainly among overseas media, that Japan's economy has technically entered a recessionary phase due to the slowdown in emerging and commodity-exporting economies, particularly China. That being said, on the back of an increase in receipts of income from overseas business reflecting the yen's depreciation, as well as an improvement in the terms of trade due to the declines in energy and commodity prices, firms have seen record profits, which consequently is reflected in gross national income (GNI) and gross domestic income (GDI) having been on clear increasing trends compared to GDP.

To Mr. Sato’s points, consider this chart of corporate profits:

They have increased solidly for the last two years. And while recent GDP readings have been weak, income numbers are fairly strong:

Finally, LEIs declined .3 to 103.9 while CEIs increased 3 points to 116.6.

Canadian manufacturing remains in negative territory, with the Markit composite number dropping to 47.5 – its sharpest drop in 5 years. The report was uniformly bearish:

There were widespread reports that subdued business confidence had resulted in lower spending levels and delays to new projects, particularly in the energy sector. Manufacturers responded to the latest fall in new work by lowering their inventories and initiating price discounting strategies. Moreover, payroll numbers decreased for the sixth month running amid a sharp and accelerated fall in work-in-hand across the sector.

The Canadian stock market entered a bear market. Bank of Canada head Poloz offered the following analysis of Canada’s macro economy in a recent policy speech

The fact is that a decline in commodity prices such as the one we have seen is one of the most complex shocks that a policy-maker can face. We know that the overall effect on Canada is unambiguously negative because of the loss of income from exporting commodities I mentioned earlier. Nevertheless, at the global level, the positive effects on importing countries will more than offset the negative effects on exporting countries, yielding a net positive impact on global growth.

However, the real complexity appears beneath the surface, where the drop in commodity prices sets in motion sectoral and regional forces that can take years to play out. These include higher consumer spending in response to lower energy costs, falling investment and employment in the economy’s resource sector, and rising investment and employment in the non-resource sectors—in other words, the reverse of what we saw from 2002 to 2014.

There is no simple policy response in this situation. The forces that have been set in motion simply must work themselves out. The economy’s adjustment process can be difficult and painful for individuals, and there are policies that can help buffer those effects, but the adjustments must eventually happen.

…..

Let’s consider for a moment how this works. As I said, lower resource prices mean lower income for Canada as a whole. Economic growth slows, as it did early last year. At first, the slowdown was concentrated in oil-producing regions as companies cut investment spending. But then it began to spill over into other sectors through supply chains and lower consumption spending as workers were laid off. In this context, and in anticipation of the spreading fallout, the Bank lowered interest rates to help buffer the economy and keep inflation aimed at our targe

Canada nearly experienced a technical recession last year. 2016 does not look good.

The Australia Industry Group released its three sector reports. The manufacturing number expanded for a sixth consecutive month: although it dropped .6, it was still positive with a 51.9 reading. 5 of 8 sectors expanded and 5 of 7 sub-indexes grew. Services, however, contracted for a third consecutive month. Only 2 of 9 sectors expanded with 5 of 6 sub-indexes declining. Finally, the construction index dropped 3.9 to 46.8. New orders declined for all four sectors. The combined picture of these three indexes is weak. While manufacturing is expanding, the breadth of service sector and construction weakness shows a slowing economy.

So, as the new year starts, the world economy is still in a difficult situation. The Chinese slowdown is impacting a number of developing countries, slowing their top-line growth. Deflationary pressures continue. But now, we have an event (the Chinese market drop) that triggered concerns about global, leading to action (a global sell-off). Don't be surprised to see increased volatility in the coming few months.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis