FOMC Preview: Liftoff Is Imminent, but What’s the Flight Plan?

As usual, I am late in getting out holiday cards; I have no gift ideas for anyone on my list; and my Halloween decorations are still all over the house. But this year, I have an excuse. I can just blame the Federal Reserve when my children complain that there is nothing under the tree.

The Federal Open Market Committee (FOMC) gathering next week became a “live” meeting when the Fed declined to act in September. Those who follow U.S. monetary policy have, therefore, had to stay close to their desks and stay away from the punch bowl.

When interest rates were reduced to near zero in 2008, many thought that they wouldn’t stay there for long. Seven years (to the day) afterwards, the Federal Reserve is finally expected to increase the range for short-term rates by 25 basis points. Statements from Fed officials have all but guaranteed the outcome; it would be great surprise and a great blow to the Fed’s credibility if nothing happened next Wednesday afternoon.

Analysts and markets have already moved on from speculating about the launch date and are intently focused on the trajectory for the mission. This was always the more important aspect for economic and market performance. We anticipate that the Fed will offer a message of studied restraint; rates will go up further in 2016, but only very slowly.

Here is our take on the elements that will be addressed during next week’s discussions.

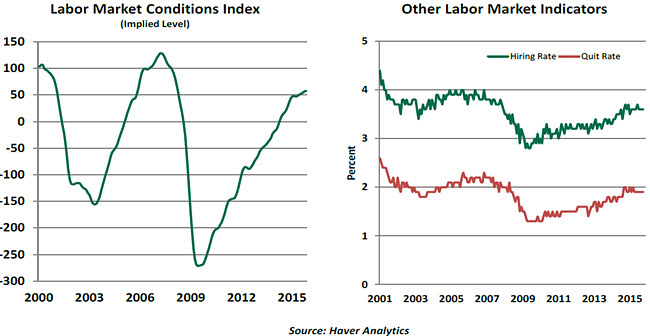

We are not at full employment. Beneath the aggregates, one senses that many who have gotten back to work in the past few years are not in their ideal jobs. But the rising quit rate (close to its pre-crisis high) suggests that people are trading up.

It is not necessary for the Fed to fully achieve its employment or inflation mandates before beginning the long process of normalizing policy; it merely has to have confidence that the goals will be reached. For the job market, the destination is in sight.

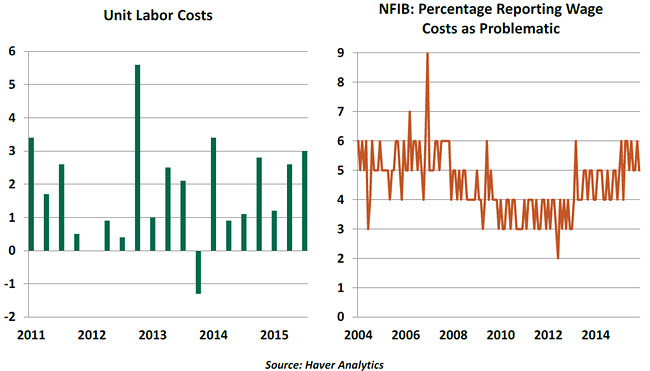

Inflation is well below the targeted level. For some on the FOMC, the discussion ends there; they view the 2% objective as a kind of average to be achieved over time. Because core inflation has been below the target for the past 3-1/2 years, there are those who think the economy should be allowed to run “hot” for a while to compensate.

For others, conditions remain too close to deflation for comfort. Central banks typically view inflation that is too low and too high asymmetrically, with the former of greater concern.

Nonetheless, core inflation is likely to creep upward as labor market slack diminishes and oil prices eventually stabilize. The dollar may not get too much stronger if the Fed offers a soothing message. And to adherents of monetarism, M2 is growing at about 6% and bank lending is growing at nearly 8%. Both would suggest higher inflation ahead.

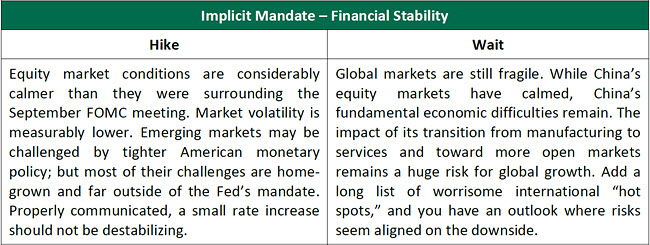

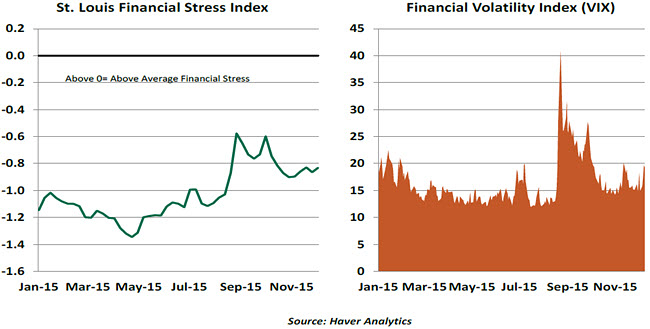

The Fed does not set policy to achieve certain stock market outcomes and resents being depicted that way. If equities can hold their values as interest rates begin to normalize, it would be a strong positive statement about the fundamentals underneath asset prices. The financial system is much more settled than it was in 2008, so the likelihood is very small that a small interest rate increase would be destabilizing.

There will be a lot to digest after the announcement is made. The statement containing the action will offer shadings on the economic outlook; it will also identify any dissenters to the decision. Based on past remarks, several participants will be somewhat uncomfortable with raising interest rates. But if the hike is paired with a temperate message (a “dovish tightening”) it could turn skeptics into adherents.

The formal statement will also likely contain details on how the Fed plans to steer interest rates toward their new equilibrium. Each element of the new range (0.25% to 0.5%) must be re-calibrated. The upper end is the easy part: the interest rate on excess reserves will be increased by fiat. But the other components (the federal funds rate and the interest rate on the Fed’s reverse repurchase program) will require market transactions whose parameters will be outlined in the post-meeting communication.

An updated summary of economic projections (SEP) will be released. Known more colloquially as “the dot chart,” the SEP offers a consensus view of growth and the optimal course for overnight interest rates. If the median forecast shows a shallow normalization, markets can rest assured. But it will also be important to see if the dispersion around the central tendency has changed.

And finally, Janet Yellen will step to the rostrum to face the media for an hour. Candidly, she hasn’t looked at all comfortable in these settings since assuming the chair’s role at the beginning of the year. She’s sometimes been tentative and technical and has yet to learn the skill of answering the question she wants to answer as opposed to the one posed. But if she is able to deliver a clear message about the Fed’s intentions, she’ll get the markets working with her.

We’ll provide analysis of the outcome on Wednesday afternoon. Hopefully, the markets will react so well that I’ll have the resources and the time to get caught up on my seasonal responsibilities.