Weighing the Week Ahead: Will There Be a January Effect?

After two weeks of slow, holiday-shortened trading, the A-Teams will (gradually) get back to work. Despite the importance of the data on this week’s schedule, I expect a different sort of fixation on the calendar. We can expect widespread discussion of the question:

Will we see a January effect?

Prior Theme Recap

In my last WTWA I predicted that the slow news and trading environment would lead to a pundit parade, with plenty of forecasts for the new year. This was pretty accurate, including some carry over from our prior week’s question about Santa. Things were looking up until the last two days of the year disappointed. You can see this clearly from Doug Short’s weekly chart. His full post also includes analysis for the full year. (With the ever-increasing effects from foreign markets, you should also add Doug’s World Markets Weekend Update to your reading list).

Doug’s update also provides multi-year context. See his full post for more excellent charts and analysis.

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

This Week’s Theme

There are plenty of important data releases this week, including the most important. At most other times this would stimulate spirited discussion about the economy. At the start of the year there is a very different dynamic. Perhaps because it is simpler to think about, everyone loves the focus on the start of the new year. I expect most observers to be asking –

Will we see a January effect?

I did not say “the” January effect, since the calendar-based prognoses have broadened to include the following:

- The original January effect saw losers sold near the end of the year to harvest the tax losses. After 30 days, many repurchase, causing a January rebound.

- Some investors wait until January to sell winners, delaying the tax effect. Reportedly (Art Cashin) others sell winning names short during the last two days of the trading year, anticipating the tax trade.

- Many believe that as goes January, so goes the year.

- Some believe that as goes the first trading day, so goes January and the year.

- Some will focus on the Presidential election year.

- And a few will stick to the data.

As always, I have my own opinion in the conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

Despite the negative result for stocks, there was some good news last week.

- Hotel occupancy is the best on record. Calculated Risk reports it as 65.9%.

- Modest overall economic improvement in five key indicators monitored by New Deal Democrat. They are all good, but many might be surprised by this chart:

- Consumer confidence from the Conference Board registered 96.5, beating expectations by a few points. Doug Short has the story, including data showing the historical significance of the indicator.

The Bad

Some of the economic data was disappointing.

- Initial jobless claims increased to 287K. See Calculated Risk for analysis and a helpful chart.

- Rail traffic weakness continues. Steven Hansen of GEI says it is “sliding into recession.”

- The Chicago PMI was only 42.9, missing expectations by seven points and signaling continuing contraction in Midwest manufacturing. Detailed analysis from Steven Hansen of GEI (who was definitely working last week!)

- Pending home sales declined by 0.9%. Too little inventory once again gets the blame. Hmm.

The Ugly

My intention was to skip this topic over the holidays, despite the many candidates. Then I saw a famous bear’s list of “possible” predictions for 2016. The list was heavy on terrorism ideas and even included a possible injury to Warren Buffett. To me, this went beyond the bounds of good fun. It also serves to keep investors scared witless (TM OldProf Euphemism). The question of how terrorism affects investing is difficult, and not a subject for light-hearted speculation – especially when it includes specific ideas of what attacks might be the worst.

Mrs. OldProf advises me that I should not name and link to this source – who is notoriously thin-skinned. You can find it easily if you really want, but I am not recommending it. The post just hit me the wrong way. I suppose that others might like it.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. This week’s award goes to Matt Busigin, who explains that US Recession Callers Are Embarrassing Themselves. Here is his lead paragraph, worth keeping in mind on Monday when the ISM data come out:

Through a combination of quackery, charlatanism, and inadequate utilisation of mathematics, callers for US recession in 2016 are embarrassing themselves. Again.

The most prominent reason for recession calling may well be the Institute of Supply Management’s Manufacturing Purchasing Manager Index. The problem with this recession forecasting methodology is that it doesn’t work.

Please also see our review of last year’s winners. You will find the summary fun to read, featuring advice which remains timely.

A Well-Deserved Remembrance

If we had been doing the Silver Bullet in those days, we certainly would have recognized “Tanta” who wrote anonymously for Calculated Risk before her death in 2008. Joe Weisenthal and Tracy Alloway have a nice interview on the subject with Bill McBride.

Noteworthy

How would you do as Fed Chair? Could you get reappointed after four years? Give it a try with this enjoyable game.

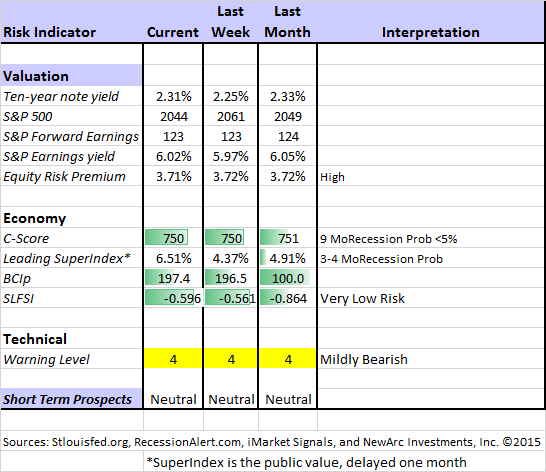

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. Beginning last week I made some changes in our regular table, separating three different ways of considering risk. For valuation I report the equity risk premium. This is the difference between what we expect stocks to earn in the next twelve months and the return from the ten-year Treasury note. I have found this approach to be an effective method for measuring market perception of stock risk. This is now easier to monitor because of the excellent work of Brian Gilmartin, whose analysis of the Thomson-Reuters data is our principal source for forward earnings.

Our economic risk indicators have not changed.

In our monitoring of market technical risk, I am using our “new” Oscar model. I put “new” in quotes because Oscar is in the same tradition as Felix and the product of extensive testing. We have found that the overall market indication is more helpful for those investing or trading individual stocks. The score ranges from 1 to 5, with 5 representing a high warning level. The 2-4 range is acceptable for stock trading, with various levels of caution.

Oscar improves trading results by taking some profits during good times and getting out of the market when technical risk is high. This is not market timing as we normally think of it, since it is not an effort to pick tops and bottoms and it does not go short. Instead, Oscar identifies and limits risk. (More to come about Oscar).

I considered continuing to report the Felix updates, but I already have a distinction between long and short-term methods. I want to minimize confusion. Those who want this information can subscribe to our weekly Felix updates.

In my continuing effort to provide an effective investor summary of the most important economic data I have added Georg Vrba’s Business Cycle Index, which we have frequently cited in this space. In contrast to the ECRI “black box” approach, Georg provides a full description of the model and the components.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

Doug Short: Provides an array of important economic updates including the best charts around. One of these is monitoring the ECRI’s business cycle analysis, as his associate Jill Mislinski does in this week’s update. His Big Four update is the single best visual update of the indicators used in official recession dating. You can see each element and the aggregate, along with a table of the data. The full article is loaded with charts and analysis.

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting systems. These include approaches helpful in both economic and market timing. He has been very accurate in helping people to stay on the right side of the market.

Georg Vrba: provides an array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result with the twenty-week forward look from the Business Cycle Indicator, updated weekly and now part of our featured indicators.

Check out Georg’s new mutual fund analysis tool. You can easily see how your fund has done on this fee-adjusted ratings scale.

Monitoring earnings trends is a crucial step in making sound investment decisions. Brian Gilmartin has an excellent review of the last several years, as well as a look at the year ahead.

The Week Ahead

This is a big week for economic data, including several of the most important reports, as well as some catching up from the holidays. While I highlight the most important items, you can get an excellent comprehensive listing at Investing.com. You can filter for country, type of report, and other factors.

The “A List” includes the following:

- Employment report (F). Still viewed as the single most important data point.

- ADP private employment (W). A strong alternative to the official report, using a different method.

- ISM Index (M). Of special interest given the recent softness in manufacturing and the Chicago PMI.

- Auto sales (T). Continuing strength in this important non-government read?

- Initial claims (Th). Fastest and most accurate update on job losses.

- FOMC minutes (W). Even with a unanimous vote and a press conference, we can expect careful scrutiny in the search for added information.

The “B List” includes the following:

- ISM services index (W). Less widely followed than manufacturing because it is newer – actually covers more of the economy.

- Construction spending (M). November data, but still interesting.

- Factory orders (W). Also November data, with weaker results expected.

- Trade balance (W). November data with significance for Q4 GDP.

- Wholesale inventories (F). Also November data with implications for GDP.

- Crude oil inventories (W). Continued focus on oil prices keeps this report in the spotlight.

It will be a light week for speechifying, but there will be some action at the American Economic Association’s annual meeting, held in SF this year. Regional Fed President John Williams will be on a panel.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Oscar continues both the neutral market forecast, and the bearish lean. We are about 35% invested in this program. There are often plenty of good investments, even in an expected flat market. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix and Oscar’s weekly ratings updates via email to etf at newarc dot com. They appear almost every day at Scutify.

Dr. Brett Steenbarger has two great pieces this week.

- Why you do better if working in a team

- The root causes of traders’ emotional problems

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page (just updated!) summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking. Pick a topic and give it a try.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important source, it would be it would be the annual economic summary from Calculated Risk. Most investors find it challenging to link news about the economy to their own portfolios. Chuck Carnevale has provided great evidence that “earnings determine market price.” I have repeatedly shown that economic growth is strongly linked to earnings, with recessions the biggest risk. Bill McBride tells you what to watch for in 2016 – a very helpful list. A recent interview with Peter Lynch underscores this point. His advice has been widely summarized as investing in what you know. He notes that this is not enough.

What’s wrong with the popular-wisdom version of his ideology, which is usually cited as “invest in what you know”? It leaves out the role of serious fundamental stock research. “People buy a stock and they know nothing about it,” he says. “That’s gambling and it’s not good.”

Stock and Fund Ideas

Chuck Carnevale has ten undervalued dividend champions, with complete analysis and explanations. Here is one that we like, enhancing the nice yield with the sale of short-term calls.

Value investors should note that even Mr. Buffett had a tough year, the worst since 2009. Great methods do not always work within a twelve-month period.

A guide to contrarian investing in 2016. (Luke Kawa/Bloomberg)

Lessons from 2015

You can get in short form – pithy and witty entries — with Josh Brown’s annual list. He asks many contributors to comment on what they learned. I always give some thought to this question, but it is difficult. I thought I had a good entry, but it didn’t beat this response:

Scott Redler (T3 Live): Uber, the world’s largest taxi company, owns no vehicles. Facebook, the world’s most popular media owner, creates no content. Alibaba, the most valuable retailer, has no inventory. And Airbnb, the world’s largest accommodation provider, owns no real estate

Michael Johnston has a categorized list of 50 favorite posts from a variety of authors. You can use the descriptions to find the most interesting for your own needs.

Watch out for….

Market Forecasts. It is pretty easy to find a long list of failures in the forecasting business, especially if there is no attention to error bands or the general volatility of the series in question. But what should you do? Even a buy-and-hold investor is making an implicit assumption about the general market trend. Cullen Roche has, as we would expect, a very pragmatic viewpoint on the subject. You will find it helpful in navigating the noise.

And also …. Market history in headlines for the last decade. This is a great illustration of the difficulty in calling the twists and turns of events. (Morgan Housel)

Hotel stocks. Does Airbnb represent a real threat?

Oil price forecasts. A history to consider. Check out some of the big-time calls versus this chart:

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. There are several great links, but I especially liked Monevator’s advice on How to Lose Money in 2016. There are seven great points, but the first will give you the idea:

1. Sign up to some bearish investing websites

Good investing starts with a long-term businesslike mindset, so to really invest badly, it’s vital you start rotting your thinking without delay.

Where better to begin than by overdosing on some of the doom and gloom newsletters that have been predicting Financial Armageddon since, well, the start of the last bull market?

They’ll have you swapping your carefully chosen funds and shares for baked beans and survival kits in no time.

Ideally find one that offers occasional tips on Russian gold miners, Panamanian oil explorers and the like.

That way you’ll get twice the bang for your buck.

Final Thoughts

If we are to believe in a calendar effect, we need to see two things:

- Some logical reason behind the action. Deadlines for tax effects qualify, so it is something to think about.

- A reason that the effect has not been fully anticipated – already “discounted” by the market. In general, this sort of regular opportunity lasts only until it is widely known.

Count me in with the final group, de-emphasizing January and following the data. The calendar data are weak, and do not cover enough history.

This illustrates our most persistent theme from last year:

If you want to be a trader, you need to outguess what everyone else is thinking about. We do some of that.

If you are an investor you can rely upon your own assessment, taking what the market is giving you.

Eventually stock prices depend upon earnings which depend upon economic growth. Leading economist Brad DeLong illustrates why growth continues, but has been sluggish.

[long EMR versus short calls]