We’ve seen daily references to what has worked — or hasn’t worked — when interest rates have risen in the past. Strategists, asset managers and pundits have dusted off numerous “tried-and-true” historical playbooks for investing in a rising-rate environment. But here’s the problem with applying those lessons to today’s markets: We’ve never been in this exact economic environment before, so relying too heavily on what’s worked in the past may not be particularly helpful.

What makes today’s environment unique?

In my view, the current torrent of rising-rate analyses should be taken with healthy dose of skepticism. Why? Here are three reasons.

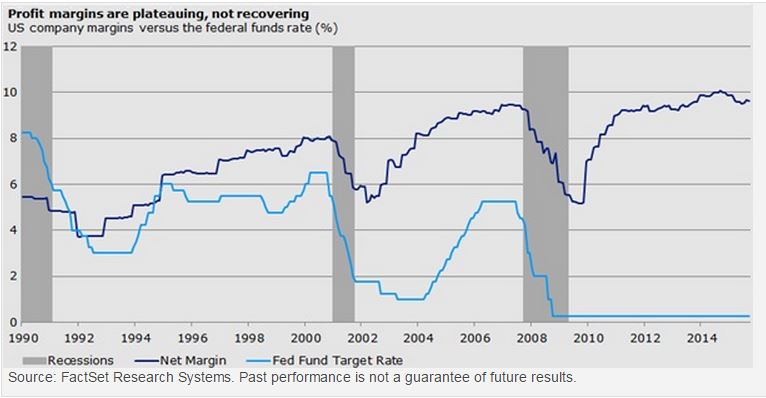

1. First, the “typical” conditions that have accompanied tightening cycles during the past 35 years include rebounding margins and improving credit conditions and sales growth. But these conditions have mostly run their course in the present bull market cycle, which began in March 2009. Today, margins are plateauing (Figure 1), credit conditions are worsening (Figure 2), and sales revisions are showing declines in growth.

Figure 1

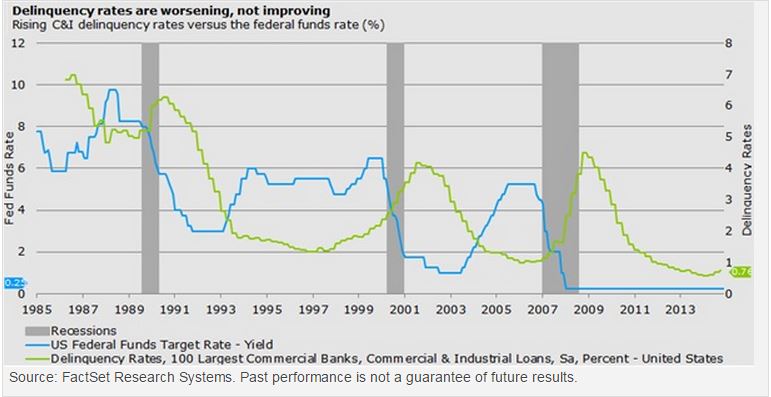

What happens when monetary policy tightens in the midst of these conditions? We don’t know because we’ve never seen it happen. It’s unusual for the Federal Reserve (Fed) to begin monetary tightening so late in the profit cycle. The Fed has rarely, if ever, started to raise rates when sales growth is disappointing, delinquency rates for commercial and industrial (C&I) loans are worsening (Figure 2), corporate margins are narrowing, and other major central banks are loosening monetary policy.

Figure 2

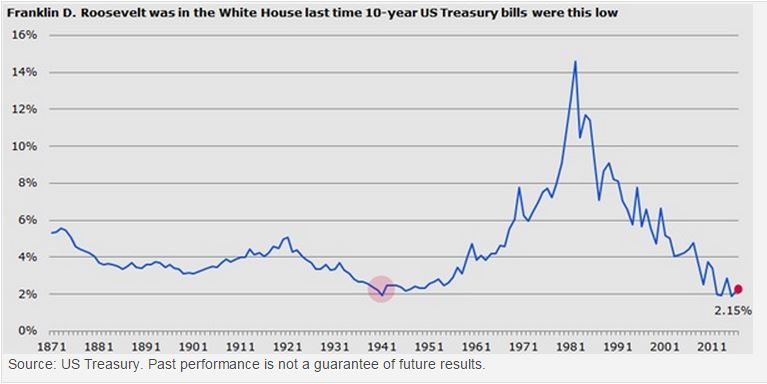

2. Second, the federal funds target rate, recently between zero and 0.25%,1 hasn’t seen these levels since the 1940s (Figure 3). The 10-year US Treasury bill, at 2.32% for the week ending Nov. 13, hasn’t been this low in 60 years.1 We have simply not seen a tightening cycle from these levels in modern times.

Figure 3

3. Third, many asset classifications in use today — for example, value stocks, growth stocks, core plus bond strategies, emerging market debt, master limited partnerships (MLP), floating rate securities and convertibles — either didn’t exist or didn’t have widely available proxies in the 1920s and 1930s. As a result, no one has been able to write a playbook that goes back far enough in history to be applicable to today’s environment. Even if we could, the economy is so different today that the interpretation may be misused.

Where do we go from here?

Unprecedented conditions call for active management. Why? Rules-based approaches that rely heavily on historical playbooks often break down at inflection points. This is particularly important today as I believe we face the most expected tightening cycle in history.

Active management uses sound fundamental research to anticipate potential changes in conditions to position client assets accordingly. Our Invesco Dividend Value team has often remarked that results for our clients are made or broken at inflection points. It’s important to exercise a healthy degree of skepticism and a willingness to go against consensus when supported by bottom-up analysis. This is particularly important today as everyone seems to be using the same rising-rate playbook.

Our team has successfully navigated numerous economic environments by maintaining a full market cycle perspective. We believe this experience becomes even more important as investors, who are less focused on the signs of a mature profit cycle, seek a revised rising-rate playbook for today’s environment.

Learn more about Invesco Diversified Dividend Fund and Invesco Dividend Income Fund.

1 Source: US Federal Reserve System, Nov. 16, 2015

Important information

Profit margin measures the profitability of a company by dividing net income by revenues.

A master limited partnership (MLP) is a publicly traded limited partnership in which the limited partner provides capital and receives periodic income distributions from the MLP’s cash flow and the general partner manages the MLP’s affairs and receives compensation linked to its performance.

Floating rates are interest rates that are allowed to move up and down with the rest of the market or with an index.

The federal funds target rate is the interest rate at which banks and other depository institutions lend money to each other, usually on an overnight basis.

An inflection point is an event that results in a significant positive or negative change in the progress of a company, industry, sector, economy or geopolitical situation.

Credit conditions denote the availability of loans, or credit.

A value style of investing is subject to the risk that the valuations never improve or that the returns will trail other styles of investing or the overall stock markets.

The Fund is subject to certain other risks. Please see the current prospectus for more information regarding the risks associated with an investment in the Fund.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Before investing, investors should carefully read the prospectus and/or summary prospectus and carefully consider the investment objectives, risks, charges and expenses. For this and more complete information about the fund(s), investors should ask their advisors for a prospectus/summary prospectus or visit invesco.com/fundprospectus.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.

Time to throw out the rising-rate playbook? by Invesco Blog