Last week, I looked at the US consumer. This week, I’ll focus on US businesses, which is the tale of two sectors:

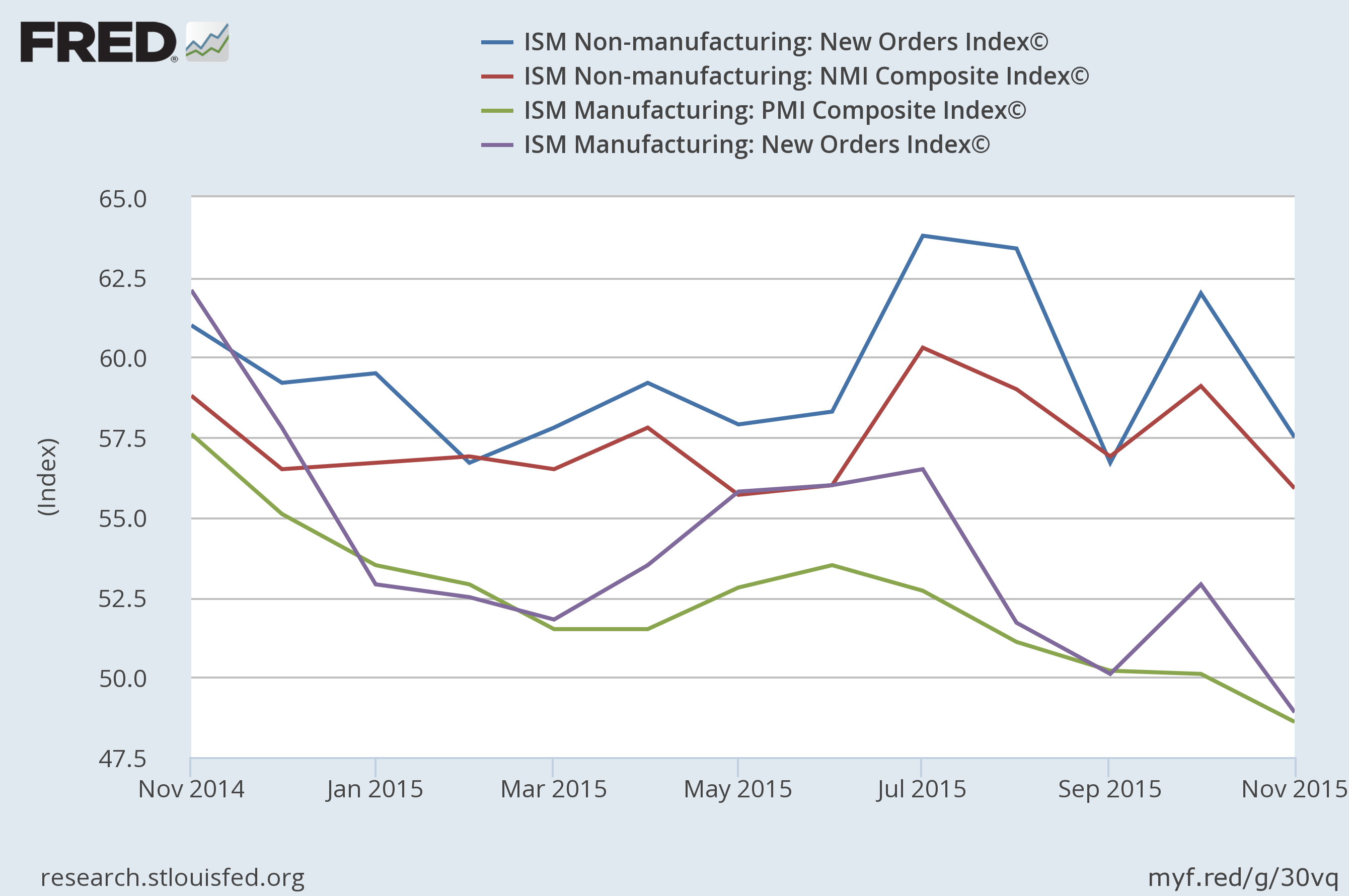

The service sector (the top two lines) continues to grow strongly, while the manufacturing sector (the bottom two lines) is now in a mild recession. The most recent ISM manufacturing report’s anecdotal comments contains the reason for the industrial slowdown:

- "The oil and gas industry is realizing that [the] ‘low’ oil prices are now the new reality with expectations to continue at this level for some time." (Petroleum & Coal Products)

- "Still seeing deflation in raw materials." (Chemical Products)

- "Bookings and new orders are lower than expected." (Computer & Electronic Products)

- "Automotive remains strong." (Fabricated Metal Products)

- "Business is still good." (Transportation Equipment)

- "Downturn in China and European markets are negatively affecting our business." (Machinery)

- "Strong dollar is slowing our sales to China as they can buy in Europe." (Primary Metals)

- "Medical device continues to be strong." (Miscellaneous Manufacturing)

- "Incoming orders have leveled off from the summer." (Furniture & Related Products)

- "Month-over-month conditions are stable." (Food, Beverage & Tobacco Products)

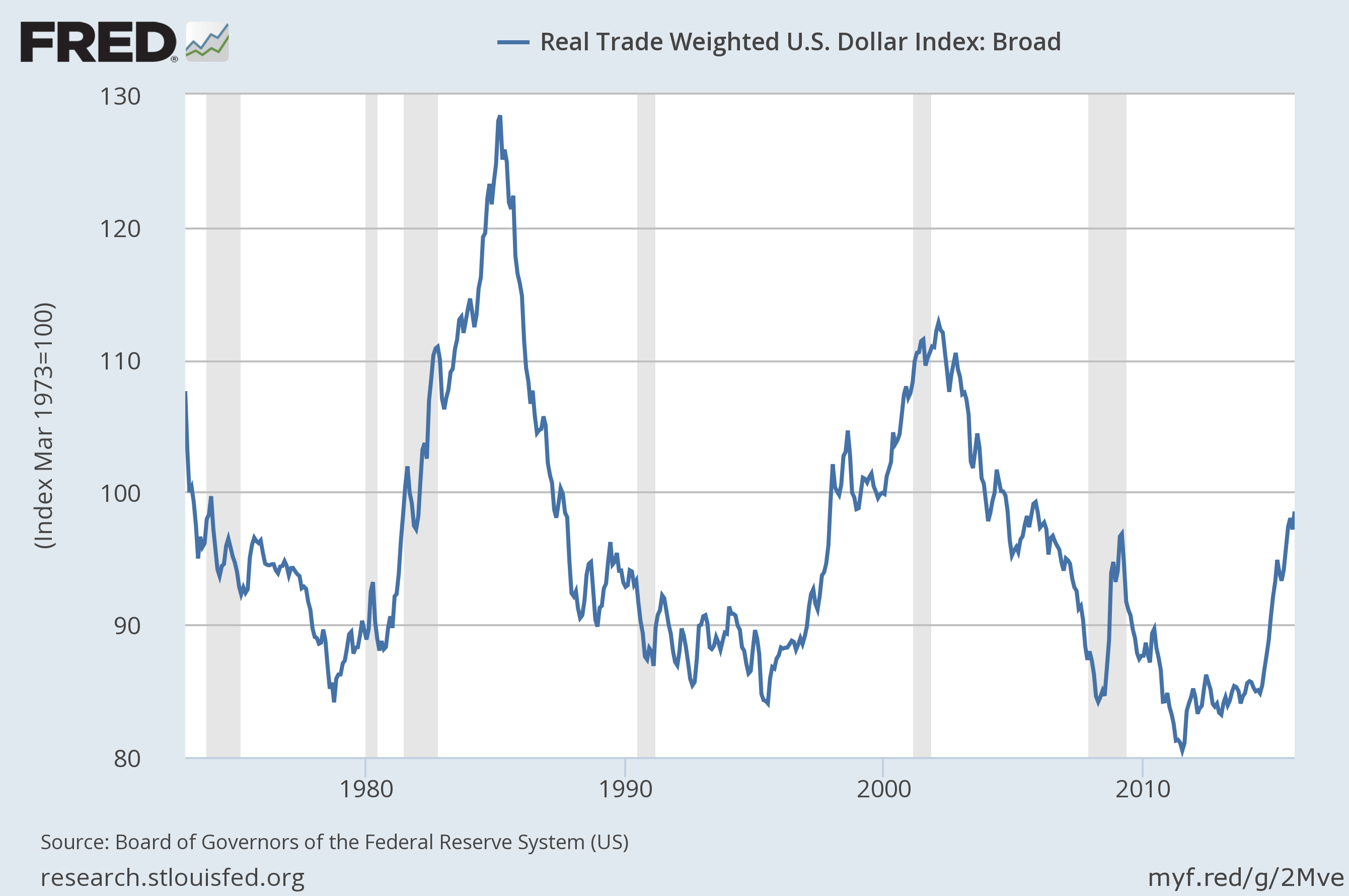

Oil continues to move lower. And with record high supplies combined with Iran wanting to join the market, there is little reason to expect a major rally. And adding to oil’s weakness is the dollar’s strength:

The trade-weighted dollar is near post-recession highs. Not only does this compress commodity prices, it also makes US exports more expensive. Not only is the dollar strong, but emerging economies are weak:

The outlook for the EMEs is a key source of global uncertainty at present, given their large contribution to global trade and GDP growth. In China, ensuring a smooth rebalancing of the economy, whilst avoiding a sharp reduction in GDP growth and containing financial stability risks, presents challenges. A more significant slowdown in Chinese domestic demand could hit financial market confidence and the growth prospects of many economies, including the advanced economies. For EMEs more broadly, challenges have increased, reflecting weaker commodity prices, tighter credit conditions and lower potential output growth, with the risk that capital outflows and sharp currency depreciations may expose financial vulnerabilities.

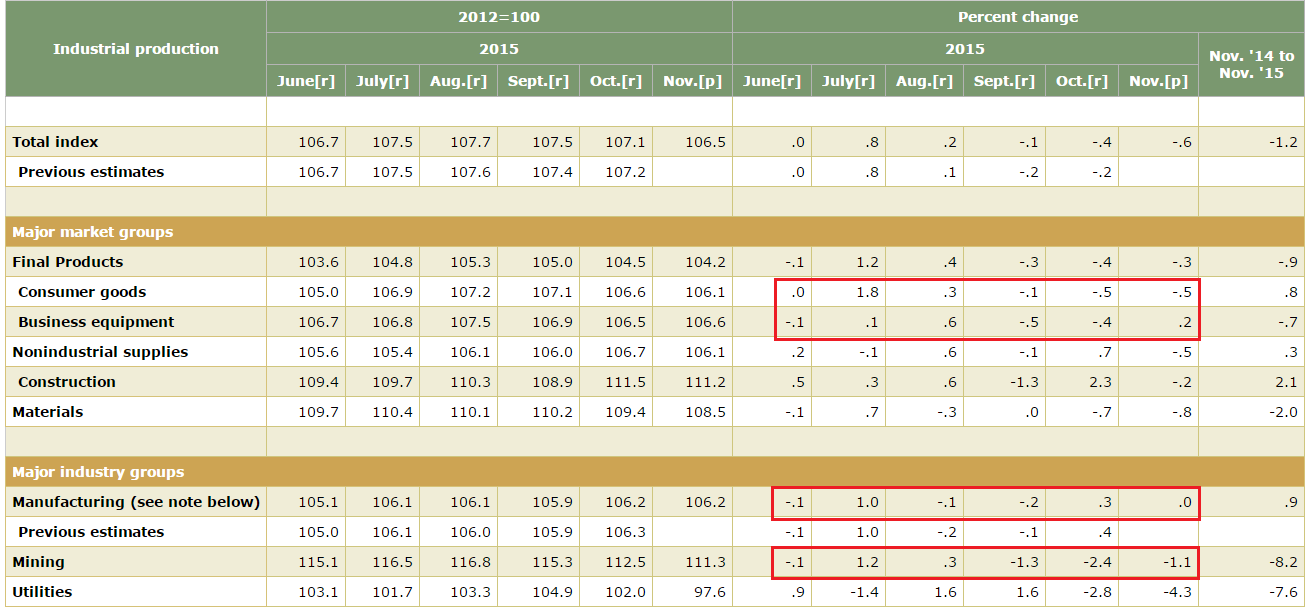

The weak readings across the entire industrial production data set highlights manufacturing and industrial weakness:

Consumer product and business equipment manufacturing contracted in three of the last six months. Of the major industry groups, manufacturing contracted in three of the last six months, while mining (think oil extraction) declined in 4 of the last 6 months. No matter which metric is used to describe the manufacturing sector, you find abundant weakness.

Conclusion: the industrial sector is weak. And the combination of low oil prices, a strong dollar and weak emerging economies will keep the sector weak for some time.

Market: the market is expensive. The current and forward PEs of the SPYs and QQQs is 22.95/23.25 and 17.44/20.04, respectively. The earnings outlook continues to disappoint:

Total S&P 500 earnings are expected to be down -7.3% from the same period last year on -3.3% lower revenues in Q4, with 12 of the 16 Zacks sectors expected to see earnings decline from the year-earlier period. Earnings growth for the index would still be in the negative even if exclude the Energy sector drag from the aggregate picture.

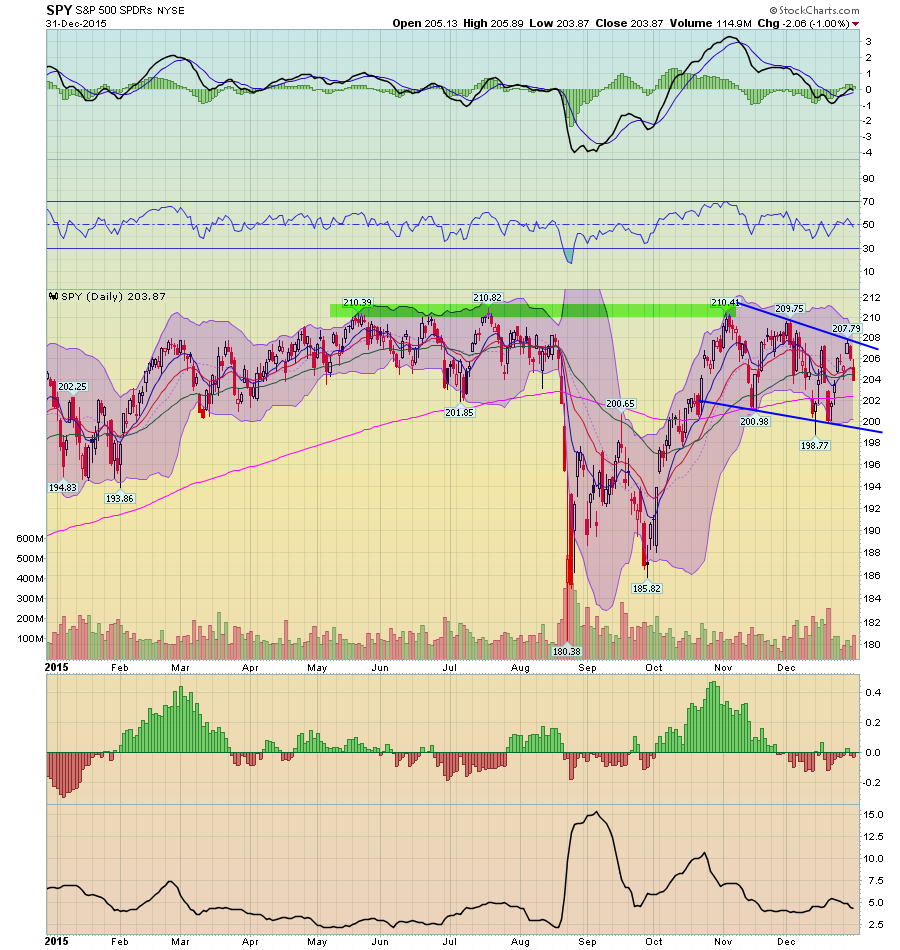

As for the market, it’s been moving slightly lower for the last two months:

Prices hit 210.41 at the beginning of November but have moved slightly lower since. Momentum declined over the same period. And the internals have become more defensive:

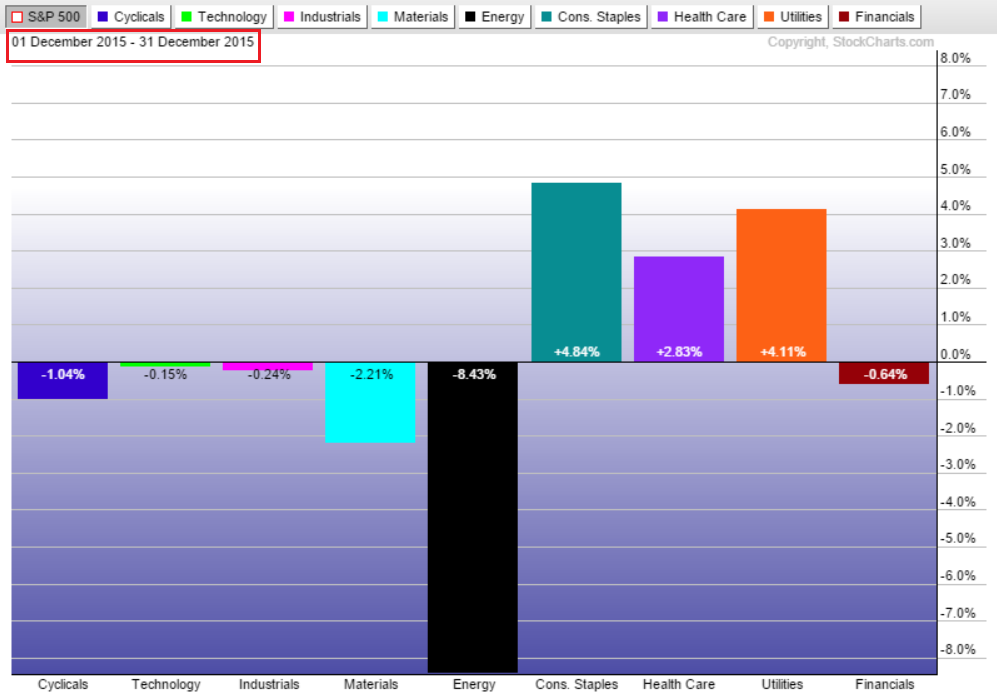

In the last month, stapled increased ~5%, health care rose 3% and utilities were up 4%. Everything else was down, especially basic materials and energy.

So, the industrial sector starts the year in a mild recession while the market is becoming defensive in its sector rotation.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis