International Economic Week in Review: A Year End Look At China, Japan and Australia, Edition

Last week, we looked at the EU, UK and Canada. This week we’ll turn to the pacific for a look at Japan, China and Australia.

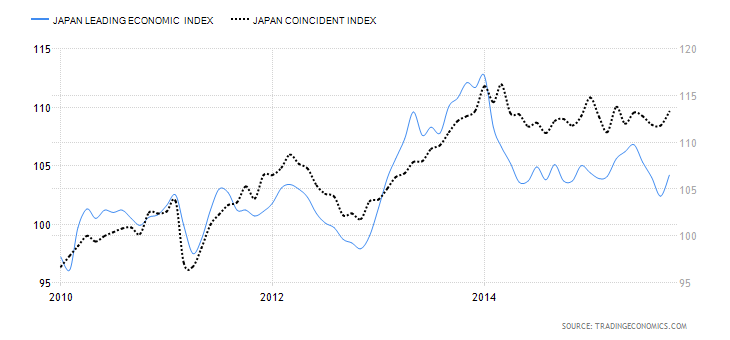

There are several statistics that perfectly explain the Japanese economy. The first two are the leading and coincident indicators published by the The Cabinet Office:

Both have moved sideways for the last year and a half. These sum-up the zero sum game that is Japanese economic growth:

The economy contracted in five of the last twelve quarters. This is very much a, “two steps forward, one step back,” scenario. Also consider these two coincident indicators:

Industrial production has also been moving sideways for the last two years

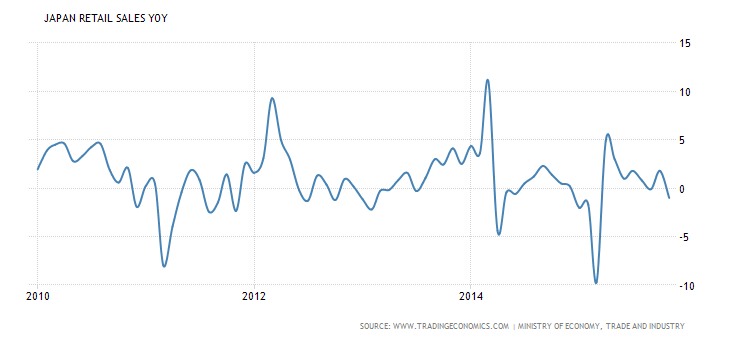

And the Y/Y percentage change in retail sales is slowly approaching 0%. More importantly, this coincidental indicator of consumer activity has vacillated between extreme readings for the last several years, indicating the Japanese consumer is not healthy. Despite numerous efforts, the Japanese economy simply can’t seem to make any meaningful forward progress without some type of major retrenchment.

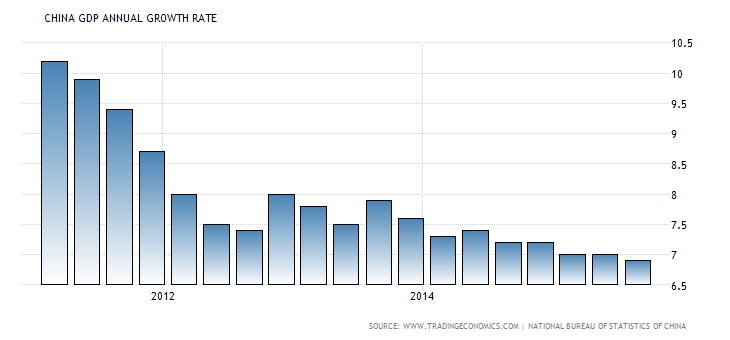

The Chinese slowdown continues. Overall Y/Y GDP growth declined from ~10% 2012 to its current level of 6.9%:

The decline in manufacturing is the primary reason for the drop; the Markit manufacturing PMI has printed below 50 in 11 of the last 12 months, indicating a near year-long contraction:

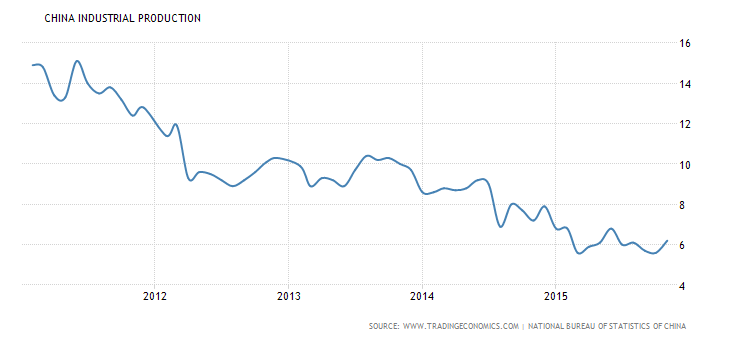

And industrial production has consistently moved lower since 2014:

According to the privately compiled Chinese Beige Book, the slowdown is widespread:

China’s economic conditions deteriorated across the board in the fourth quarter, according to a private survey from a New York-based research group that contrasted with recent official indicators that signaled some stabilization in the country’s slowdown.

National sales revenue, volumes, output, prices, profits, hiring, borrowing, and capital expenditure were all weaker than the prior three months, according to the fourth-quarter China Beige Book, published by CBB International. The indicator is modeled on the survey compiled by the Federal Reserve on the U.S. economy, and was first published in 2012

And this is before we consider the negative readings in producer prices or the record levels of debt in the economy. China is certainly not in a recession, nor is it approaching one. But the days when it would drive the world economy are over.

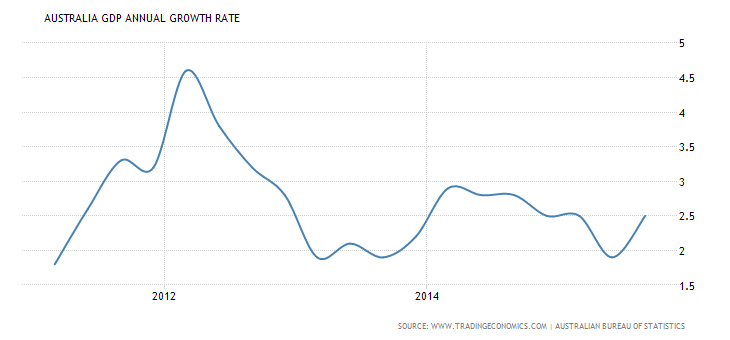

Australia is a mixed bag. While it’s not growing at a gangbusters rate, the Australian economy printed growth in the 2%-3% range for the last few years:

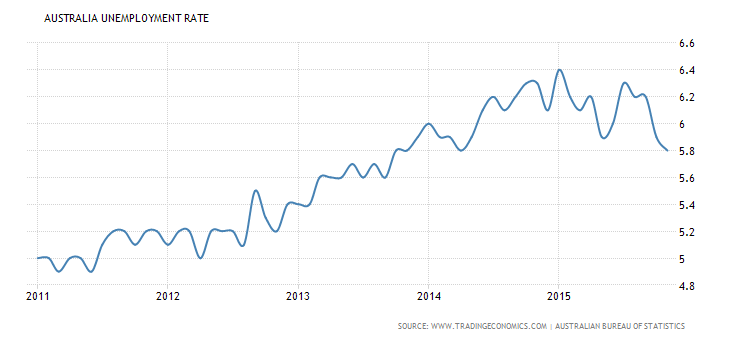

The unemployment rate is moving lower:

Sector growth, however, is mixed. Manufacturing is strongest; its index printed over 50 for the last five months. 6/7 sub-indexes increased and 5/8 sectors expanded. Services are weaker; they only expanded in 6/11 of the past months. All 5 sub-indexes contracted in the latest reading. And while construction continues expanding, apartment growth is the primary reason; CRE, residential and engineering work are all contracting. And while positive, retail sales growth is moving lower.

The Pacific Rim is suffering from the Chinese slowdown. China’s decreased appetite for raw materials is negatively impacting the giant Australian raw material build-out of the last 10 years. Japan’s intra-regional trade is slowing as well. There are no signs of a recession on the horizon. But it is obviously one step closer in the current environment.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis