In the December 29, 2014, Market View, we surveyed the investing landscape for the year ahead and examined the possibilities for key asset classes. Among our observations for 2015:

-

Against the backdrop of a slowly improving U.S. economy, growth stocks were expected to outperform value, while the broader U.S. equity market seemed poised to continue its ascent, although with less vigor, and a correction seemed likely along the way. Valuations appeared reasonable, if not overly attractive. Corporate earnings were expected to continue to grow at a decent pace.

-

On the bond side, shorter duration, less interest-rate sensitive, and lower-quality fixed-income assets, including high-yield bonds, were expected to hold up fairly well if the U.S. Federal Reserve (Fed) hiked interest rates in 2015, as was anticipated by midyear. Demand for municipal bonds was expected to be strong, given muni’s attractive taxable-equivalent yields, even as new issue supply remained relatively high.

-

International stocks, we believed, would continue to struggle with weak economic growth prospects at home and a stiff headwind from a strong U.S. dollar, but with accommodative central bank policies in the eurozone, Japan, and China, we also saw the potential for better returns. A cautionary flag was raised for emerging markets, particularly currencies, as a slowdown in China and rising commodity prices threatened some, if not all, of the developing nations’ prospects for growth.

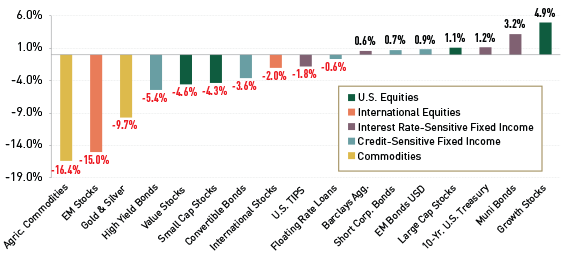

Looking back at 2015 from the last week of December, how did it all play out? (Chart 1 displays the performance of a range of asset classes.)

Chart 1: 2015 Was a Year of Clearly Defined Winners and Losers

Total returns (%) for selected asset classes, December 31, 2014-December 23, 2015

Source: Morningstar. Data as of December 23, 2015.

The investment categories listed in this chart are represented by the following indexes: Emerging Market Stocks, MSCI Emerging Market USD Index; Agricultural Commodities, S&P GSCI Agricultural Index; Gold & Silver, S&P GSCI Precious Metals Index; Small Cap Stocks, Russell 2000 Index; High-Yield Bonds, BofA Merrill Lynch U.S. High Yield Master II Constrained Index; Value Stocks, Russell 3000 Value Index; Convertible Bonds, BofA Merrill Lynch All Convertibles, All Qualities Index; International Stocks, MSCI EAFE Index; U.S. TIPS (Treasury Inflation Protected Securities), Barclays Capital U.S. Treasury TIPS Index; Large Cap Stocks, S&P 500 Index; Floating Rate Loans, Credit Suisse Leveraged Loan Index; Short-Term Corporate Bonds, BofA Merrill Lynch 1-3 year ‘BBB’ U.S. Corporate Index; EM Bonds (Emerging Market Corporate Bonds), JPMorgan CEMBI Broad Diversified Index; Barclays Agg. (Core Bonds), Barclays Capital U.S. Aggregate Bond Index; 10-Year Treasuries, BofA Merrill Lynch U.S Treasury Current 10-Year Index; Municipal Bonds, Barclays Capital Municipal Index; Growth Stocks, Russell 3000 Growth Index.

Past performance is not a reliable indicator or a guarantee of future results.

The historical data are for illustrative purposes only, do not represent the performance of any specific portfolio managed by Lord Abbett or any particular investment, and are not intended to predict or depict future results.

Indexes are unmanaged, do not reflect deduction of fees and expenses and are not available for direct investment.

Some developments were just about as expected. The U.S. economy continued to post stronger growth than the rest of the world. U.S. growth stocks were the star performers of the year. U.S. large-cap stocks (as represented by the S&P 500® Index) also held their own, although performance of the index as a whole was hurt by losses in commodity-related industries, particularly the energy sector.

Weak economic growth in the eurozone continued to weigh on equities in the region. The slowing pace of growth in China also affected economies in the emerging markets, as expected, and weakened their currencies.

Municipal bonds were the strong performers in the bond market in 2015, with the notable exception of Puerto Rican bonds, which suffered for most of the year from fears of default. Emerging market corporate bonds, a largely investment-grade sector, also turned in a respectable performance, as did U.S. short-duration corporate bonds, although, after accounting for inflation, the single bond sector left standing in positive territory was municipal bonds.

The Market View script for 2015 did take some unexpected turns, however, particularly in terms of the intensity of a key trend already in play. The sharp decline in oil prices, with the benchmark West Texas Intermediate dropping to a multiyear low of less than $36 per barrel at one point in December, surprised many. Commodity prices, in general, had been falling throughout 2014, but few anticipated the extent of the continuing decline throughout 2015 or the resulting profit recession (defined as two or more successive quarters of decline) in energy-related sectors. Poor performance in the energy sector negatively affected the high-yield bond market, which also succumbed late in 2015 in reaction to news that a Third Avenue Management high-yield fund heavily weighted in distressed debt (‘CCC’ rated or lower) had ceased redemptions.

Expectations for a rate hike were also disappointed over and over again in 2015 until December 16, when a unanimous Federal Open Market Committee, the policy-making arm of the U.S. Federal Reserve Board (Fed), finally voted to raise its targeted fed funds range to 0.25–0.50%, after seven years of near-zero rates.

Regular readers of Market View will already have noted our published insights into the markets for 2016, including our outlook for equities and fixed income. Of course, we cannot guarantee that our expectations for the new year will play out exactly as we have outlined them in these columns. But as active managers, Lord Abbett will continue to look for select investment opportunities no matter the general direction of the markets, and with a long-term perspective in mind.

A Note about Risk: The value of investments in fixed-income securities will change as interest rates fluctuate and in response to market movements. As interest rates fall, the prices of debt securities tend to rise, and as interest rates rise, the prices of debt securities tend to fall. Investments in high-yield securities (sometimes called junk bonds) carry increased risks of price volatility, illiquidity, and the possibility of default in the timely payment of interest and principal. Bonds may also be subject to other types of risk, such as call, credit, liquidity, interest-rate, and general market risks. Longer term debt securities are usually more sensitive to interest-rate changes. The longer the maturity date of a security, the greater the effect a change in interest rates is likely to have on its price. Moreover, the specific collateral used to secure a loan may decline in value or become illiquid, which would adversely affect the loan's value. Convertible securities have both equity and fixed-income risk characteristics. Like all fixed-income securities, the value of convertible securities is susceptible to the risk of market losses attributable to changes in interest rates. Generally, the market value of convertible securities tends to decline as interest rates increase and, conversely, to increase as interest rates decline. The value of investments in equity securities will fluctuate in response to general economic conditions and to changes in the prospects of particular companies and/or sectors in the economy. Investing in international securities generally poses greater risk than investing in domestic securities, including greater price fluctuations and higher transaction costs. Special risks are inherent to international investing, including those related to currency fluctuations and foreign, political, and economic events. Foreign investments generally pose greater risks than domestic investments, including greater price fluctuations and higher transaction costs. Investments in Puerto Rico and other U.S. territories, commonwealths, and possessions may be affected by local, state, and regional factors. These may include, for example, economic or political developments, erosion of the tax base, and the possibility of credit problems. No investing strategy can overcome all market volatility or guarantee future results.

Market forecasts and projections are based on current market conditions and are subject to change without notice.

The BofA Merrill Lynch All Convertibles, All Qualities Index contains issues that have a greater than $50 million aggregate market value. The issues are U.S. dollar-denominated, sold into the U.S. market and publicly traded in the United States.

The BofA Merrill Lynch High Yield Master II Constrained Index is a market value-weighted index of all domestic and Yankee high-yield bonds, including deferred interest bonds and payment-in-kind securities. Issues included in the index have maturities of one year or more and have a credit rating lower than BB-/Baa3, but are not in default. The BofA Merrill Lynch U.S. High Yield Master II Constrained Index limits any individual issuer to a maximum of 2% benchmark exposure.

The BofA Merrill Lynch 1-3 year ‘BBB’ U.S. Corporate Index is an unmanaged index comprised of U.S. dollar- denominated, investment-grade corporate debt securities publicly issued in the U.S. domestic market, with between one and three years remaining to final maturity.

The BofA Merrill Lynch 10-Year Current U.S. Treasury Yield Index is an unmanaged index tracking the 10-year component of US Treasury securities.

The Barclays Capital Municipal Index is a broad measure of the municipal bond market with maturities of at least one year. To be included in this index, bonds must have a minimum credit rating of at least Baa, an outstanding par value of at least $3 million, and be issued as part of a transaction of at least $50 million. Includes both zero coupon bonds and bonds subject to the Alternative Minimum Tax.

The Barclays Capital U.S. Aggregate Bond Index is an unmanaged index composed of securities from the Barclays Government/Corporate Bond Index, Mortgage-Backed Securities Index and the Asset-Backed Securities Index. Total return comprises price appreciation/depreciation and income as a percentage of the original investment. Indexes are rebalanced monthly by market capitalization.

The Barclays U.S. Treasury TIPS Index is an unmanaged index comprised of U.S. Treasury Inflation Protected Securities with at least $1 billion in outstanding face value.

The Credit Suisse Leveraged Loan Index is designed to mirror the investable universe of the U.S. dollar-denominated leveraged loan market. The CS Leveraged Loan Index is an unmanaged, trader-priced index that tracks leveraged loans. The CS Leveraged Loan Index, which includes reinvested dividends, has been taken from published sources.

J.P. Morgan Corporate Emerging Markets Bond Index Broad Diversified (CEMBI BD): The CEMBI is a market capitalization-weighted index that tracks total returns of US dollar-denominated debt instruments issued by corporate entities in emerging-market countries. The index limits the current face amount allocations of the bonds in the CEMBI Broad by constraining the total face amount outstanding for countries with larger debt stocks.

The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the U.S. & Canada. The MSCI EAFE Index consists of the following 21 developed market country indices: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, and the United Kingdom.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity-market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 23 emerging-market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Peru, Philippines, Poland, Russia, Qatar, South Africa, Taiwan, Thailand, Turkey, and UAE.

The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represents approximately 10% of the total market capitalization of the Russell 3000 Index.

The Russell 3000® Growth Index measures the performance of those Russell 3000 Index companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 3000® Value Index measures the performance of those Russell 3000 Index companies with lower price-to-book ratios and lower forecasted growth values.

The S&P 500® Index is widely regarded as the standard for measuring large cap U.S. stock market performance and includes a representative sample of leading companies in leading industries.

The S&P GSCI® Agricultural Index is a subset of the S&P GSCI®, a leading measure of general price movements and inflation in the world economy. The index is weighted by production and includes the most liquid commodity futures.

The S&P GSCI® Precious Metals Index is a subset of the S&P GSCI®, a leading measure of general price movements and inflation in the world economy. The index is weighted by production and includes the most liquid commodity futures.

Treasury Inflation Protected Securities (TIPS) are treasury securities that are indexed to inflation in order to protect investors from the negative effects of inflation. TIPS are considered an extremely low-risk investment since they are backed by the U.S. government and since their par value rises with inflation, as measured by the Consumer Price Index, while their interest rate remains fixed.

Treasuries are debt securities issued by the U.S. government and secured by its full faith and credit. Income from Treasury securities is exempt from state and local taxes. Although U.S. government securities are guaranteed as to payments of interest and principal, their market prices are not guaranteed and will fluctuate in response to market movements.