International Retrospective and Outlook

In an effort to move beyond standard communications that focus on the drivers of quarterly and annual performance, we’d like to offer a longer-term retrospective on international markets and our outlook for the secular changes that we expect to evolve over time. In particular, we’d like to highlight the opportunities and challenges in emerging markets.

The Role of Portfolio Management

Before we dive into specifics, it’s important to provide some context through a description of the way we view portfolio management. In portfolio management, our job is to look at current stock valuations relative to expected future valuations based on our growth, profitability and cash-flow projections. An investment is deemed to be attractive when the expected difference between the two valuations is sufficiently large, considering the likely time period and risk level. As such, the portfolio-management process is very subjective.

In other fields, a study of historical phenomena and established relationships may be helpful in coming up with solutions to current problems. But in portfolio management, a study of the recent past may lead you astray — unless at the very least you also consider longer horizons and the valuation levels from where you begin your investments. Additionally, even if you come equipped with a full understanding of past and current valuation levels, future returns are highly uncertain due to considerations such as geopolitical issues and investor risk preferences.

As indications of the dangers involved in using the recent past to predict the future, consider the following examples from the last two decades: During the dot-com bubble that peaked in 2000, many investors assumed stocks would keep rising without regard to revenues and profits. In the years leading up to the Global Financial Crisis, Wall Street firms, rating agencies and government officials all acted as if housing prices would never go down. Just as remarkably, sophisticated hedge-fund managers have periodically damaged their track records by erroneously concluding that historical relationships among securities prices would persist in the future.

On the other hand, when most market participants assume that fear and pessimism will endure, attractive investments are often available at reasonable prices — including high-quality Internet companies after the tech washout in 2002, European stocks subsequent to the Greek debt crisis in 2010, and Japanese equities starting in 2012 once monetary and fiscal stimulus began to reverse years of stagnation.

With this context in mind, we can address what we consider to be some of the main issues confronting international investors today.

Emerging Markets in General

More than a decade ago, Jim O’Neill at Goldman Sachs coined the term “BRICs” to refer to the higher-profile emerging markets of Brazil, Russia, India and China. In 2006, Goldman Sachs Asset Management launched its BRIC Fund. However, in September 2015, Goldman announced that it would close the Fund due to poor performance and a dearth of assets. In addition, over the last five years, almost all of the MSCI emerging-market indices have lost ground.

So why would anyone want to invest in emerging markets now? The answer has to do with the reasons described above: The recent past does not necessarily predict the future. And valuations matter. This isn’t to say that all emerging markets are created equal and would provide the same opportunities going forward. But negative or relatively flat returns should at least pique our interest that some emerging-market stocks may be on sale at attractive prices.

At Wasatch Advisors, many of our investment styles are growth-oriented. We don’t want to overpay for growth, however. And in emerging markets, generally speaking, valuation measures are now less expensive than those in developed markets. These valuation measures include ratios such as price to earnings (P/Es), cyclically adjusted P/Es, price to cash flow, price to book value, price to sales, and enterprise value to earnings before interest, taxes, depreciation and amortization. Moreover, today’s dividend yields tend to be higher in emerging markets.

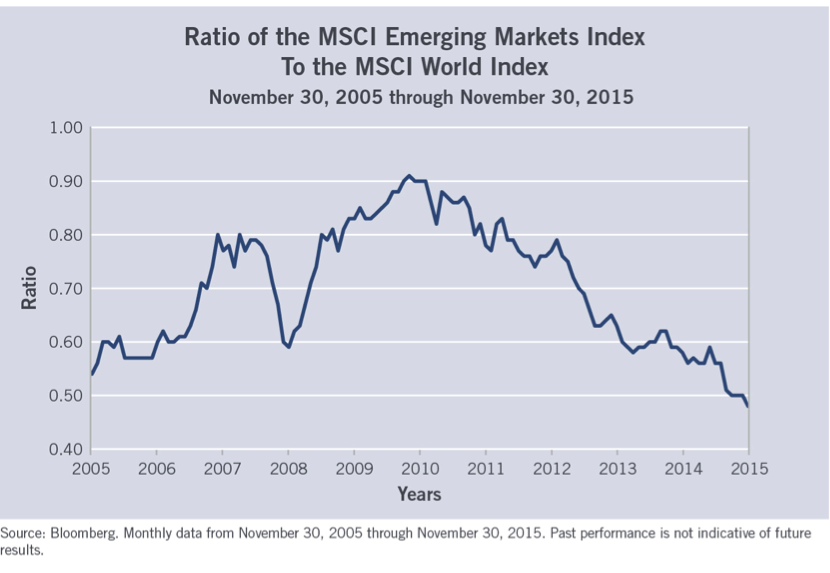

The chart below is another indication of the potential attractiveness of emerging markets relative to developed markets. The chart shows the ratio of the MSCI Emerging Markets Index divided by the MSCI World Index (an index of developed markets). The ratio is at its lowest level in 10 years, and developed markets have dramatically outperformed since 2010. If we believe most trends eventually reverse course, we may be close to a period of outperformance for emerging markets. Looking at how the ratio has fluctuated over time, we can see that such a period of outperformance began in 2008 at a level not far from today’s level.

Lower overall valuations do not mean that we never “pay up” for growth. In fact, if we believe growth prospects are outstanding, we’re often willing to accept a high P/E or price-to-cash-flow ratio in emerging markets. For example, an emerging-market financial-services company might have tremendous prospects because the population is in the early stages of using bank accounts, consumer credit and mobile money. Also, consider an emerging-market pharmaceuticals company that has significant headroom for growth because health care is rapidly improving in the company’s home country, and because its drugs can be exported around the world.

In the short to medium term, which unfortunately can last several years, stock prices can be quite unpredictable. However, looking at the long term, we feel comfortable with the investments we’ve made in emerging markets — not only because these investments have been extensively researched, but also because overall valuations (as described above) are lower than in developed countries. And when we do decide to pay up for growth, we generally feel more confident because we believe emerging/frontier markets have significant untapped potential, as they account for approximately 80% of the world’s population and about 50% of global gross domestic product (GDP).

Where to Be Cautious on Emerging Markets

The section above describes general conditions. But like all generalizations, we have to be careful with the generalizations applied to emerging markets. Just consider the differences among the BRICs. Brazil and Russia are major commodity exporters with poor political situations. India, on the other hand, is a large importer of energy resources, has an encouraging political environment, and has a long history of well-regulated securities markets. As for China, the country is still a significant — albeit slowing — buyer of commodities. China also has widespread corporate-governance problems, despite its hard-earned status as the world’s second-largest economy.

Earlier in 2015, equity markets around the world were mostly down as reports surfaced of lower economic growth in China. Moreover, many Chinese companies failed to meet revenue and earnings expectations. The Chinese government initially responded with direct intervention in an effort to prop up stock prices, and with a coordinated devaluation of the Chinese yuan against other major currencies — probably intended to support exports. At the time, we said that we thought such intervention was bad policy.

Normally, a coordinated currency devaluation is done in an effort to strengthen an economy by making exported goods cheaper to foreign buyers. But we don’t believe the yuan devaluation so far has been significant enough to materially improve the Chinese economy. As a result, we think it’s likely that China’s government will continue to devalue the yuan — which, relative to the last several years, is still strong versus many other currencies.

China fears that if it can’t maintain its growth rate, the country’s debt as a percentage of GDP will continue to rise. This percentage is already above 240%, up from about 160% in 2007. The problem is that a lower currency value makes China even more dependent on exports for economic growth. What’s really needed is a balanced economy with a greater percentage of growth coming from spending by Chinese consumers.

Because China’s industrial base is vulnerable to lower demand from around the world, and because domestic Chinese consumption of goods and services is not yet picking up the slack in the economy, deflation is a significant threat. In fact, through November 2015, China’s producer-price index declined for the 45th consecutive month. In a deflationary environment, consumers are even more reluctant to spend and businesses are less inclined to make capital investments. Such an environment can create a situation in which additional loans are not used to grow the economy in a meaningful way, but instead are used to keep alive “zombie” corporations that lack innovation and are already overly indebted.

A deflationary spiral gripped Japan for much of the past 25 years. Even now, Japan’s Nikkei 225 Index is only about half the level it was in 1989. While we don’t believe China’s deflationary risk is anywhere near the same magnitude, Japan provides a cautionary tale of how excessive speculation can lead to excessive pessimism — and why we need to be cautious regarding Chinese stocks today. Moreover, Japan’s woes illustrate the dangers of assuming that future returns can be predicted by the recent past without also considering valuation levels. One of the most-often quoted statistics from Japan’s bubble era was that the property encompassing the Tokyo Imperial Palace and surrounding gardens was valued more highly than all the real estate in California.

Underweight China, Commodity Exporters and Centers of Political Instability

So where does this leave us as investors — particularly as emerging-market investors? Let’s start with how we were positioned even before the equity-market declines earlier in 2015. We were underweighted in China and Hong Kong for quite some time because we had trouble finding companies that met our criteria for long-duration growth and reasonable valuations. Competition is especially intense in China, and companies often sacrifice profitability in order to gain market share. In addition, we still haven’t seen enough emphasis on fair disclosure of information and on ethical trading practices at the mainland stock exchanges.

Beyond our underweighting in China and Hong Kong, we were also underweighted in companies and countries that are heavily dependent on commodity exports to the rest of the world. These factors helped enhance our performance relative to our benchmarks as the Chinese markets fell significantly below their highs. And we don’t currently have plans to materially increase our exposure to Chinese or commodity-oriented names, as we believe there could be more pain to come in these areas.

As we’ve said in previous commentaries, we’ve never invested in Chinese A-shares — which are traded on China’s mainland exchanges — due to our concerns regarding growth, valuations and transparency. When we do decide to pursue additional opportunities in China, it’s likely that our investments will be through the H-shares traded in Hong Kong, where corporate governance is better and speculation is less extreme. In addition, we expect to place more emphasis on dividends — which have tended to be reliable indicators of quality and stability — and we expect to monitor our holdings even more closely for signs of improvement or deterioration.

Going forward, we anticipate that commodity-related issues and/or political instability will continue to create challenges in countries such as Brazil, Chile, Indonesia, Malaysia, Peru, Russia, South Africa and Turkey. While we’re currently underweighted in these countries as a group, our underweighting may become even more pronounced over time.

Overweight Oil Importers and Countries Growing Their Domestic Economies

On the other hand, our outlook is much more positive for India, Mexico and the Philippines. As big buyers of foreign energy resources, India and the Philippines have been huge beneficiaries of lower oil prices. In addition, we see all three countries as having favorable demographics and plenty of potential for growth in domestic (home-country) consumer demand. Moreover, we believe India and Mexico offer good investment opportunities in certain types of exports (e.g., pharmaceuticals and information-technology services from India, and durable manufactured goods from Mexico). Due to a relatively healthy U.S. economy, Mexico’s manufacturing exporters are particularly well-situated, as the two countries are strong trading partners.

Among emerging markets, we expect India to remain the largest country weighting in our portfolios. From a macro perspective, we like the fact that India is governed by elected officials. As a result, we’ve found that market forces are increasingly having positive effects on national and state policies and on infrastructure development. We’ve also found that — relative to most other emerging markets — financial controls, management expertise, corporate governance and transparency are remarkably good in India. The reasons for these positive conditions include a strong regulatory environment maintained by the Reserve Bank of India and a long history of multinational corporations. In fact, many multinationals have had operations in India for more than 75 years, which has created a strong business culture despite periodic political and economic challenges.

Our outlook is also positive for North Asia, namely Korea and Taiwan. Historically, Korea had been a less-dynamic market dominated by the large, monopolistic “chaebols.” Now, however, we’re witnessing a generational shift of entrepreneurship in knowledge-based areas like health care, e-commerce and technology. When a shift like this occurs in the equity markets, it usually begins among small caps, which is what we’re seeing for Korea. Taiwan is another market where we’re finding many small-cap companies that we consider to be high quality. In addition, Taiwan has a strong macro environment with a current-account surplus and stable economic growth.

Opportunities in Developed Markets

The main focus of this discussion is on emerging markets. But we’d also like to touch on opportunities in developed markets.

Given the relatively full equity valuations and slow economic progress we’ve seen in developed markets around the world, we believe companies with the best prospects for top-line and bottom-line growth are the most likely to be rewarded in the stock market. As such, we’ve been trimming positions that we believe have lower growth potential, and we’ve been adding positions that we feel have higher potential.

We also believe that for quite some time to come developed markets will be in a low-growth, low-interest-rate environment in which excess capital is chasing fewer attractive investment opportunities. While there’s some debate regarding the complicated implications of low interest rates, we think that higher valuations have become the norm — and that well-chosen small-cap companies will have some of the best long-duration growth prospects, which may be necessary to justify the loftier valuations.

Based on the assessment of our U.S. team at Wasatch Advisors, we believe economic conditions and company-specific fundamentals are relatively strong in the United States. But stock prices are generally high compared to the underlying business prospects.

Among the developed markets that our international team members focus on, our largest weightings are in Japan, the United Kingdom and Germany. Economic improvement had been slow in coming to these countries, but we’ve seen better signs during the last two years — despite periodic hiccups along the way. These countries are creating increasingly positive environments for small-cap companies, and the stocks are generally less well-researched — and have better valuations — than those in the U.S. Regarding the peripheral European countries, we already have some investments in Italy. And we continue to look for signs that other peripheral countries are becoming successful in fostering the growth of their small-cap companies.

Japan Has Moved Beyond Its Decades-Long Stagnation

We’ve been steadily adding to our holdings in Japanese companies. While the economic policies of Prime Minister Shinzo Abe have received mixed reviews, company fundamentals in Japan are better than we’ve seen in decades. Japanese companies are increasingly committed to improving returns on equity and creating shareholder value, which we think have the potential to be rewarded in the stock market. There’s also been a cultural shift in Japan to embrace entrepreneurship. And the effects of these changes are being seen in a more-vibrant employment picture with incomes on the rise.

In terms of our favorite types of Japanese companies, we like consumer-oriented businesses that are meeting needs locally and in the broader Asian region. We also like businesses that are serving their customers through the Internet — which is an avenue where Japanese companies have underutilized the available technology, but where they are now catching up to their global competitors. Another attractive feature of Internet businesses is that they focus on efficiency, which should be a high priority regardless of overall economic conditions.

Currency Hedging Generally Not Worth the Cost — Or the Risk

In addition to our views on company fundamentals, and on economic and political conditions around the world, a topic we’re frequently asked about is the viability of currency hedging. Broadly speaking, if we choose individual companies and countries correctly, we also believe we can mitigate some of the effects of potentially volatile international currencies. We think this is a better approach than trying to hedge our currency exposure, as currency hedging is expensive and very difficult to perform effectively — even for traders who specialize in the activity.

It’s easy to point to a specific company investment — in Brazil, for example, where the Brazilian real has declined over 30% versus the U.S. dollar so far in 2015 — and say we should have hedged the currency. That statement may be true with 20/20 hindsight, but it ignores several questions: What would have been the cost of the hedge? Could the currency depreciation have been foreseen? When should the hedge have been implemented? When should the hedge be closed? Does the company have revenues in U.S. dollars and expenses in Brazilian reais that may change the analysis? Has the currency depreciation made the company’s products more attractively priced to buyers of Brazilian exports?

Our conclusion is that even if hedging sometimes works on a one-off basis, the practice is not a sound strategy for most managers of diversified portfolios. In the short term, one successful hedge is just as likely to be offset by another, unsuccessful hedge — producing no net gain. In the long term, hedging is probably unnecessary because global companies have revenues and expenses in multiple currencies. Moreover, any portfolio that we manage with international currency exposure is likely to be part of a larger client asset base in which our portfolio provides additional diversification, including currency diversification.

Reasons for Optimism

While we have ongoing concerns regarding lower growth in China, currency devaluations, falling commodity prices, high debt levels and the ripple effects of all these, there are reasons for optimism. Among emerging markets — even before the declines earlier in 2015 — we had been finding many of the most-attractive stock valuations in the world. Therefore, we believe emerging-market valuations are that much better today, which means we see good buying opportunities.

Another important point is that the recent trends in currency exchange rates and commodity prices will not continue indefinitely. When those trends change, new opportunities will be created and we stand ready to adjust our portfolios as necessary.

About the Portfolio Managers

Roger Edgley is Director of International Research and the Lead Portfolio Manager for the Wasatch International Growth Fund and the Wasatch Emerging Markets Small Cap Fund. He is also a Portfolio Manager for the Wasatch Emerging Markets Select Fund. In addition, he was the Lead Portfolio Manager for the Wasatch International Opportunities Fund from 2005 to 2015. He joined Wasatch Advisors in 2002 and is a member of the Board of Directors. A native of the United Kingdom, he also holds U.S. citizenship and has many years of international investing experience.

Prior to joining Wasatch Advisors, Mr. Edgley was a principal, director of international research and portfolio manager for Chicago-based Liberty Wanger Asset Management, which managed the Acorn Funds. He was also a co-manager for the Acorn Foreign Forty Fund. Earlier, he worked in Hong Kong as a financial-services analyst for Societe Generale Asia/Crosby Securities and as an analyst for Strategic Asset Management.

Mr. Edgley has a Master of Arts in Philosophy from the University of Sussex and a Master of Science in Social Psychology with Statistics from the London School of Economics, where he was awarded a Social Science Research Scholarship. He earned a Bachelor of Science with honors in Psychology from the University of Hertfordshire. He is also a CFA charterholder.

Ajay Krishnan is the Lead Portfolio Manager for the Wasatch Emerging Markets Select and Emerging India Funds. He is also a Portfolio Manager for the Wasatch Global Opportunities Fund. He was a Portfolio Manager for the Ultra Growth Fund from 2000 to 2013. In addition, he was a Portfolio Manager for the World Innovators Fund from 2000 to 2007. He joined Wasatch Advisors as a Research Analyst in 1994. He was a Research Analyst on the Ultra Growth Fund prior to becoming a Portfolio Manager.

Mr. Krishnan earned a Master of Business Administration from Utah State University, where he also worked as a graduate assistant. He completed his undergraduate degree at Bombay University, earning a Bachelor of Science in Physics with a Minor in Mathematics.

Mr. Krishnan is a CFA charterholder and a member of the Salt Lake City Society of Financial Analysts. He specializes in analyzing the investment potential of fast-growing companies.

Ajay is a native of Mumbai, India and speaks Hindi and Malayalam. He enjoys traveling, reading, playing squash and road biking.

Andrey Kutuzov has been an Associate Portfolio Manager for the Wasatch Emerging Markets Small Cap Fund since 2014. He joined Wasatch Advisors in 2008 as a Senior Equities Analyst on the international research team. He also interned at Wasatch in 2007, while studying at the University of Wisconsin-Madison.

Prior to joining Wasatch Advisors, Mr. Kutuzov earned a Master of Business Administration from the University of Wisconsin’s Applied Security Analysis Program. While earning his degree, he was on a team that managed a student-run long/short equity portfolio. Prior to graduate school, he was a senior auditor at Deloitte, where his work included designing, performing, and supervising financial and internal control audits of commercial banks and investment companies under the U.S. GAAP as well as various international accounting standards.

Mr. Kutuzov also obtained a Bachelor’s and a Master’s of Accounting Degree at the University of Wisconsin-Madison. While pursuing his Master’s Degree, he taught an undergraduate course in Managerial Accounting. He is a Certified Public Accountant. He is also a CFA charterholder.

Andrey is a native Russian speaker. He enjoys traveling, sports and reading.

Scott Thomas has been an Associate Portfolio Manager for the Wasatch Emerging Markets Small Cap Fund since 2015. He joined Wasatch Advisors in 2012 as a Senior Equities Analyst on the international research team.

Prior to joining Wasatch Advisors, Mr. Thomas was a vice president at Morgan Stanley & Co. in New York City and worked in equity research for six years. He also worked in the M&A consulting group at KPMG LLP in San Francisco and New York.

In addition to the CFA and CPA certifications, Mr. Thomas holds a Bachelor of Science in Accounting from Brigham Young University.

Prior to returning to Utah, Scott lived in Madagascar and La Reunion, France. He speaks fluent French and has conversational knowledge of Malagasy and Reunion Creole.

About Wasatch Advisors®

Wasatch Advisors is the investment manager to Wasatch Funds,® a family of no-load mutual funds, as well as to separately managed institutional and individual portfolios. Wasatch Advisors pursues a disciplined approach to investing, focused on bottom-up, fundamental analysis to develop a deep understanding of the investment potential of individual companies. In making investment decisions, the portfolio managers employ a uniquely collaborative process to leverage the knowledge and skill of the entire Wasatch Advisors research team.

Wasatch Advisors is an employee-owned investment advisor founded in 1975 and headquartered in Salt Lake City, Utah. The firm had $17.4 billion in assets under management as of November 30, 2015. Wasatch Advisors, Inc. is registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940.

Risks AND DISCLOSURES

In addition to the risks of investing in foreign securities in general, the risks of investing in the securities of companies domiciled in frontier and emerging-market countries include increased political or social instability, economies based on only a few industries, unstable currencies, runaway inflation, highly volatile securities markets, unpredictable shifts in policies relating to foreign investments, lack of protection for investors against parties that fail to complete transactions, and the potential for government seizure of assets or nationalization of companies.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

Being non-diversified, the Wasatch Emerging Markets Select Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund. Non-diversification increases the risk of loss to the Fund if the values of these securities decline.

An investor should consider investment objectives, risks, charges, and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit www.WasatchFunds.com or call 800.551.1700. Please read it carefully before investing.

Information in this document regarding market or economic trends or the factors influencing historical or future performance reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

The investment objective of the Wasatch Emerging India, Wasatch Emerging Markets Select, Wasatch Emerging Markets Small Cap, Wasatch Global Opportunities, Wasatch International Growth, Wasatch International Opportunities and Wasatch World Innovators Funds is long-term growth of capital. The Wasatch Ultra Growth Fund’s primary investment objective is long-term growth of capital. Income is a secondary objective, but only when consistent with long-term growth of capital.

CFA® is a trademark owned by CFA Institute.

ALPS Distributors, Inc. is not affiliated with Wasatch Advisors.

DEFINITIONS

Chaebol means “business family” or “monopoly” in Korean. The chaebol structure can encompass a single large company or several groups of companies. Each chaebol is owned, controlled or managed by the same family dynasty, generally that of the group’s founder.

Devaluation is the planned or market-forced reduction in the value of a currency’s exchange value. Devaluation may improve a country’s balance-of-payments situation by boosting exports and reducing imports.

Dividend yield is a company’s annual dividend payments divided by its market capitalization, or the dividend per share divided by the price per share. For example, a company whose stock sells for $30 per share that pays an annual dividend of $3 per share has a dividend yield of 10%.

The financial crisis of 2007 — 2008, also known as the Global Financial Crisis and 2008 financial crisis, is considered by many economists to have been the worst financial crisis since the Great Depression of the 1930s.

Gross domestic product (GDP) is a basic measure of a country’s economic performance and is the market value of all final goods and services made within the borders of a country in a year.

The MSCI Emerging Markets Index is a free float-adjusted market capitalization index designed to measure the equity market performance of emerging markets. You cannot invest in this or any index.

The MSCI World Index captures large and mid-cap representation across 23 developed market countries.

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties or originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

The Nikkei 225 Stock Index is a price-weighted index of the 225 top Japanese companies (called the First Section) that are listed on the Tokyo Stock Exchange (TSE).

The price-to-book ratio is used to compare a company’s book value to its current market price. Book value is the value of a security or asset entered in a company’s books.

The price-to-earnings (P/E) ratio is the price of a stock divided by its earnings per share.

The price-to-sales ratio is a stock’s capitalization divided by the company’s sales over the trailing 12 months. The value is the same whether the calculation is done for the whole company or on a per-share basis.

The Producer Price Index (PPI) measures the change in the price of goods sold by manufacturers. It is a leading indicator of consumer price inflation, which accounts for the majority of overall inflation.

Return on equity (ROE) measures a company’s efficiency at generating profits from shareholders’ equity.

Valuation is the process of determining the current worth of an asset or company.

© 2015 Wasatch Funds. All rights reserved. Wasatch Funds are distributed by ALPS Distributors, Inc.

WAS003969 1/30/2017