Innovation in Emerging and Frontier Markets

Innovation Happens Globally

While many investors consider innovation to be the province of Silicon Valley and other high-tech centers in developed markets around the world, the reality is very different. A look at where intellectual property is being created gives us some indication that we have to broaden our horizons as investors if we want to take full advantage of the potential opportunities.

Innovation occurs in developed markets, in emerging markets, and even in frontier markets. Moreover, innovation isn’t confined to Internet companies and other high-tech enterprises. It’s just as prevalent among health-sciences companies that improve the quality of our lives — and among businesses that bring existing technologies to new applications.

But can investors make money from innovation in emerging markets? The short answer is yes. Emerging-market companies are typically less well-researched and therefore more reasonably priced than their developed-market peers. Once these companies have clearly demonstrated their success, however, they’re likely to be rewarded with considerable public and private valuations. Investors can profit from these valuations, especially as liquidity continues to improve in emerging-market stock transactions.

Schumpeter’s Gale

Innovation is the force that sustains economic growth, according to economist Joseph Schumpeter. In his 1943 book Capitalism, Socialism and Democracy, Schumpeter developed and popularized the concept of “creative destruction,” the process through which existing economic order is disrupted to clear the way for future growth.

“The fundamental impulse that sets and keeps the capitalist engine in motion comes from the new consumers’ goods, the new methods of production or transportation, the new markets, the new forms of industrial organization that capitalist enterprise creates,” Schumpeter wrote. “This process of Creative Destruction is the essential fact about capitalism. It is what capitalism consists in and what every capitalist concern has got to live in.”

Innovation is like a persistent, gale-force wind, according to Schumpeter’s view. Companies will either harness it in a positive way or ultimately be destroyed by it. Innovative companies are important benefactors for society. They provide the foundation for improving our standard of living.

Innovation Is Not Confined to Developed Markets

While Schumpeter hailed innovation as a defining feature of capitalism, innovation has more to do with people’s desire to improve their lives. What may be surprising to some investors is that innovation is prevalent around the world in developed markets, in emerging markets — and even in frontier markets, which are considered the least advanced of all.

Moreover, contrary to the popular belief that innovation is best encouraged by “government just getting out of the way,” governments often play important roles in setting priorities and working in partnership with new entrepreneurs and established players.

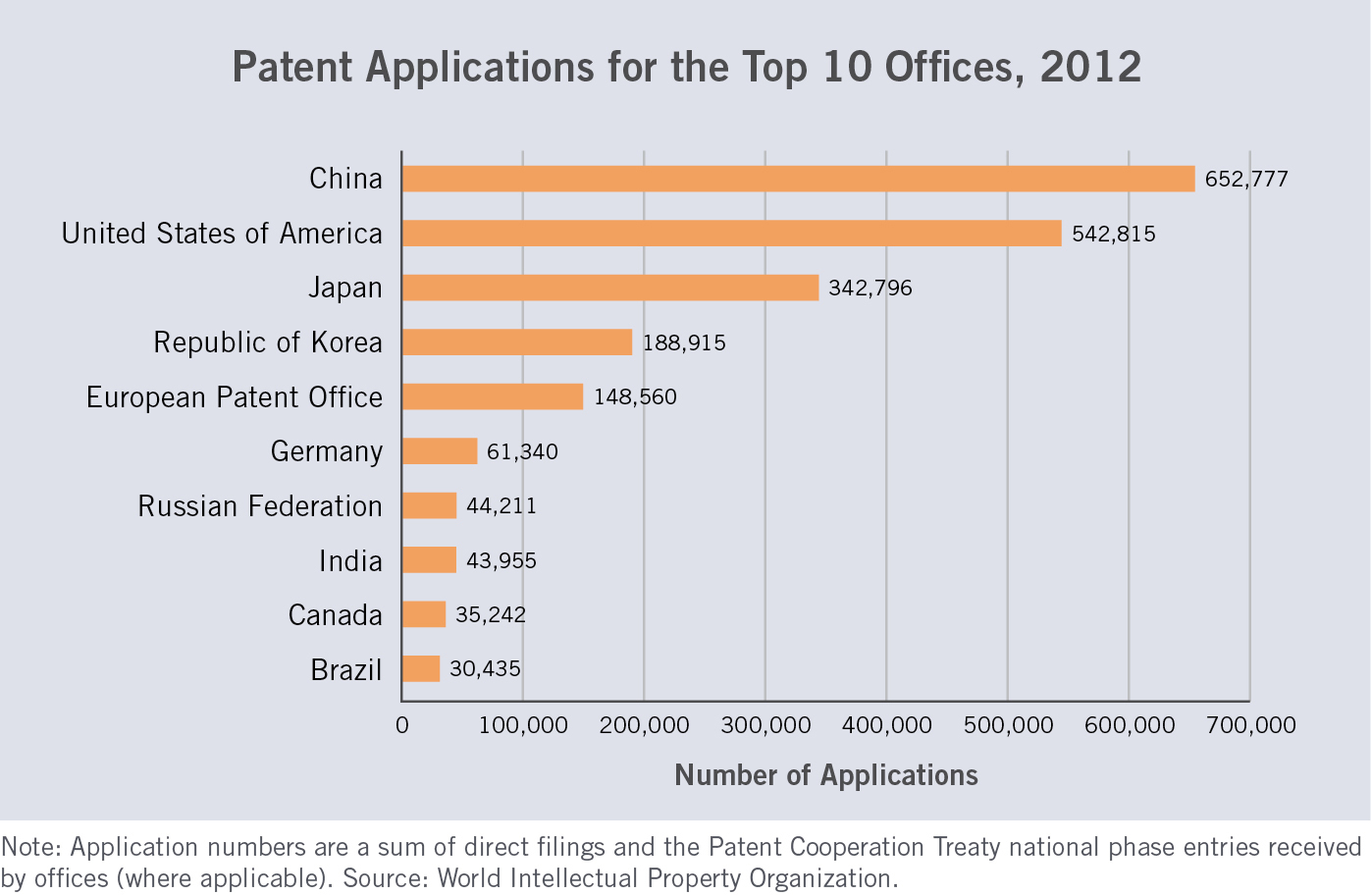

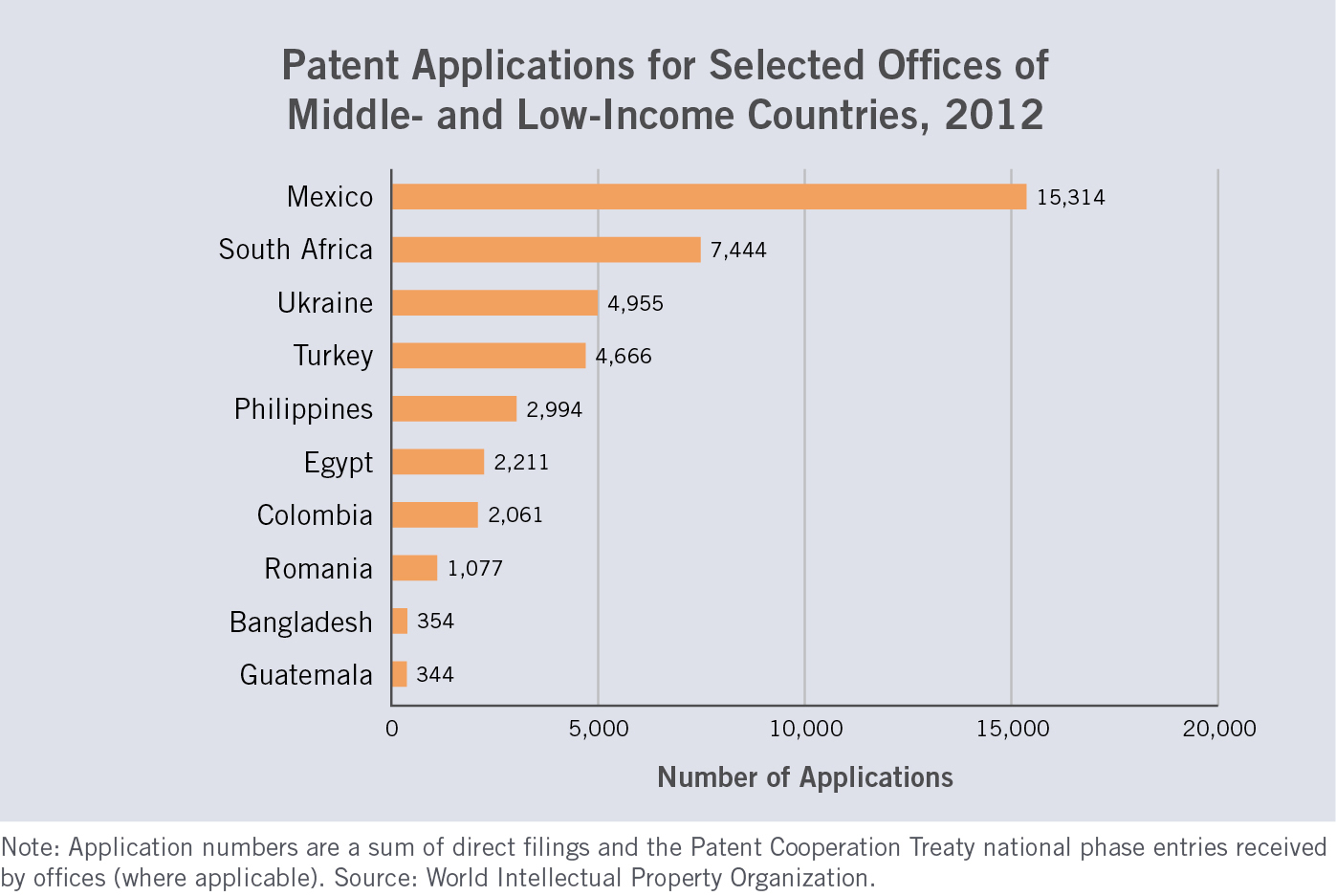

The number of patent applications is one gauge of innovation. By that measure, the charts below indicate where innovation is really occurring. The data may surprise you.

Among the top 10 offices for patent applications, five are in emerging markets. In fact, China is #1, well ahead of the United States and Japan. Perhaps even more surprising are the diversity of countries in which innovators are applying for patents and the total number of patent applications by offices in emerging and frontier markets.

When we think about innovation today, Silicon Valley and the greater San Francisco Bay Area often come to mind. But some of today’s social-media, SaaS (software-as-a-service), cloud-computing and other high-tech companies were actually started as much as half a world away. What’s more, innovation goes well beyond these tech industries.

In addition to Internet-based companies, innovation occurs in services that affect the quality of our lives — in health sciences, for example. Another fertile ground for innovation is in the revolution of a business process, whereby a company uses existing technology in new ways to leapfrog competitors.

Among emerging markets, several countries are especially rich in natural resources. In addition, most emerging and frontier markets have young and growing populations with consumers increasingly moving into the middle class. As a result of these factors, many investors in these markets tend to focus on oil and other commodity exporters, and on makers of basic consumer staples.

But the growing middle classes in emerging and frontier markets are also being served by more-innovative companies. Investors can participate in the growth of these companies, many of which are publicly traded on local stock exchanges — and some of which are even listed on major exchanges around the world.

Internet Innovation: Tencent Holdings Ltd.

Lots of today’s most-innovative companies have taken advantage of the opportunities created by the Internet’s public availability, which started in the early 1990s. Initially viewed as a novelty for rudimentary text-based messages, the Internet — itself highly innovative — has rapidly developed into the essential backbone of our communication, commerce and entertainment. Though many investors consider high technology to be largely the province of developed countries, in fact, three of the top 10 Internet companies world-wide (ranked by annual revenues) are in China.

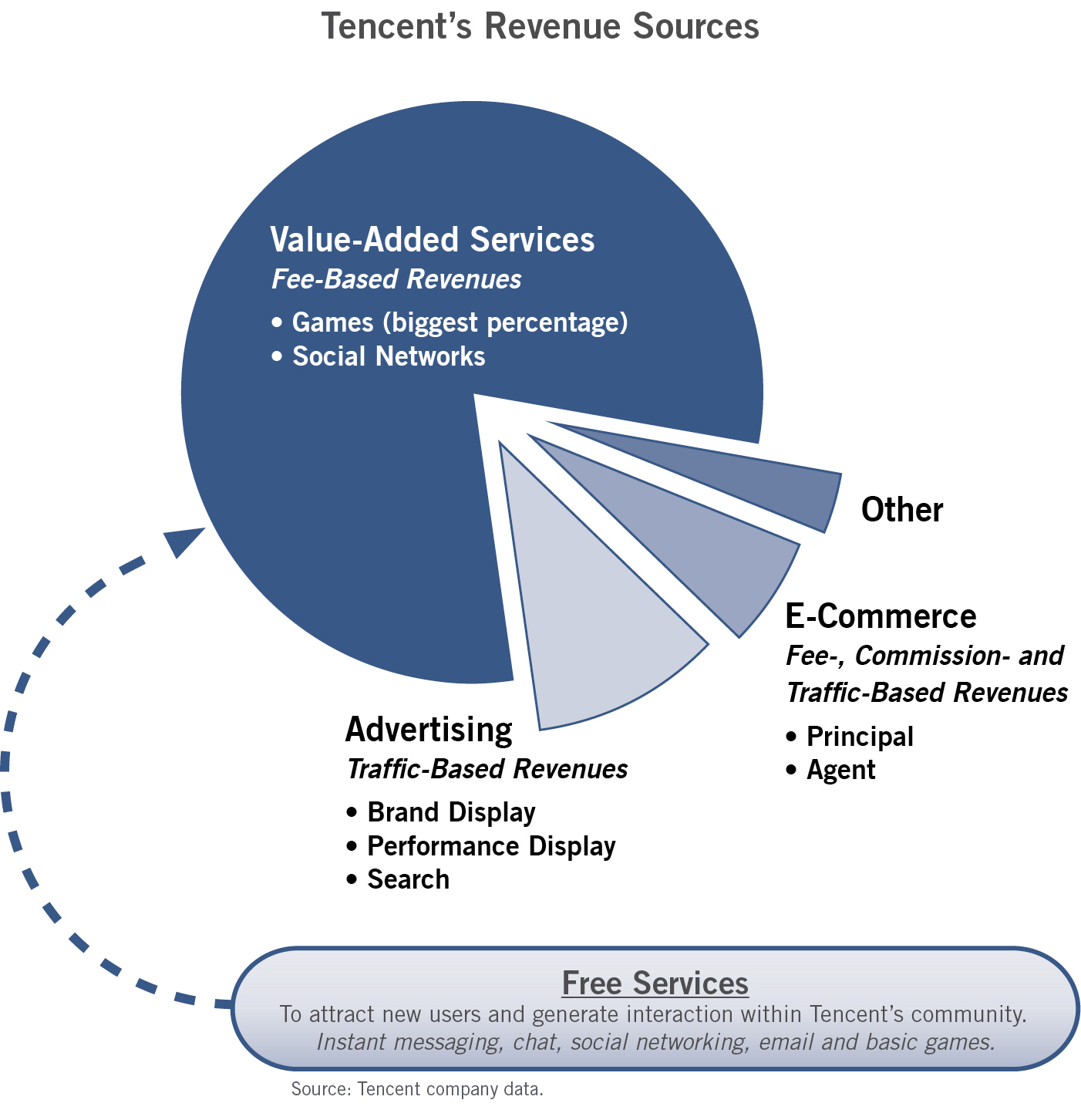

While it’s easy to dismiss many of China’s accomplishments as mere knockoffs of U.S. technology, the social-media, e-commerce and search sites that dominate in China are among the most innovative in the world. One such Chinese Internet company, Tencent Holdings Ltd., was founded in 1998 and was up and running with its QQ instant-messaging service a year later, well ahead of its counterparts elsewhere. The company went public in 2004 and today features a comprehensive range of platforms unmatched by those of its rivals in developed countries. Tencent’s offerings include messaging, chat (WeChat), social media, gaming, retailing, payment services, search, music, video, news and an Uber-style taxi service.

The company has more than 840 million users with active messaging accounts. Its market capitalization on the Hong Kong Stock Exchange is over $180 billion in U.S. dollars. In taking advantage of its understanding of Asian markets and culture, the company has been expanding its reach outside China, to enter Korea, Southeast Asia, Vietnam and India.

No U.S. companies come close to matching the breadth and integration of services that Tencent offers its users. While some observers would argue that Tencent has an inherent advantage over companies like Google and Facebook that have been mostly blocked in mainland China, Tencent can legitimately lay claim to many innovations in the use of mobile technology. Because relatively few Chinese had access to desktop computers, Tencent began creating its applications for mobile devices from day one, long before its chief rivals in developed markets.

China’s languages, culture and political system also played roles in differentiating Tencent’s services from those in the West. Unlike China’s spoken languages, which differ significantly across regions, its written languages are more universally understood. With Tencent’s messaging and chat services, people throughout China could communicate with each other more easily than ever before. The Chinese also value their personal privacy to a great extent, enhancing the appeal of the private messaging and chat systems that Tencent offers. A Facebook-type offering that eschews individual privacy would be deemed far less appealing.

The greater degree of outward privacy that Tencent provides comes at a price, however. Tencent must cooperate with the Chinese government to monitor all communication and information that traverse its network. Companies that refuse to do so, like Google and Facebook, are prohibited from operating in the country.

But even those companies that have agreed to cooperate encounter significant obstacles. LinkedIn and eBay, for example, are two U.S.-based companies that have entered the Chinese market. Though eBay’s technology may well be more sophisticated than that of relative newcomer Alibaba, eBay’s unfamiliarity with Chinese consumers and culture has been a significant impediment to success. The look and feel of eBay’s website are not considered attractive in China, where consumers prefer a more highly styled visual presentation. And as a latecomer to the market, LinkedIn also faces a serious challenge — Tencent’s users are very loyal. Tencent already has hundreds of millions of established social-media users, many of whom have grown up on the site.

Cultivating loyal users is a hallmark of Tencent’s approach. The company has long employed the “freemium” strategy of offering basic services for free and then, over a period of time, creating premium services and features that a user pays for. Tencent’s entry into the online-games business was typical. The gaming market in China had not developed to the same extent as in the U.S., perhaps in large part because gaming consoles like Nintendo’s had been banned by the government. That didn’t prevent the development of games in China, but it made their distribution problematic. Not only was there no means available to effectively promote the games, users lacked the equipment necessary to play them.

Unlike in the United States, where computer and mobile users have app stores for third-party games and other applications, no such single-source outlets existed in China. Tencent took advantage of its large user base to consolidate this deeply fractured market for online games by creating both mobile and web platforms that could be easily accessed by its users.

Developers flocked to the platforms, seeking to take advantage of the distribution opportunities that Tencent created. Users now had ready access to many previously obscure games. Tencent makes the games available via both mobile devices and its websites. Oftentimes, users can play basic versions of a game for free, but must pay a charge to access premium features. In some cases, these charges take the form of a subscription. In other cases, users must pay for certain upgrades — such as buying virtual weapons in an adventure game.

Within the span of just a few years, Tencent has captured 40% of the web-based and mobile games market in China and distributes about 50% of the mobile games consumed in Korea. Mobile gaming is now the top near-term driver of revenue for the company and should continue to grow, given the company’s large and loyal user base.

Similarly, users of Tencent’s messaging, chat and social-media services can avail themselves of basic functionality free of charge. Early in its history, Tencent was intent mainly on building a substantial user base. Later, the company began providing some for-pay options. Users now pay to add music and graphics to enhance their personal pages. About 10% of the company’s users pay for these enhanced features, roughly 10 times the rate achieved by companies offering similar features in developed markets.

The sale of advertising on Tencent’s sites, both web and mobile, is the company’s second-largest source of revenue. With its enormous user base and broad range of services, including online payment, the company has the ability to analyze user activity and purchasing patterns to deliver highly targeted advertising.

Tencent’s close relationships with its users are also enabling the development of a significant “online-to-offline” (O2O) e-commerce revenue stream. O2O initiatives give online users incentives and promotional offers for offline purchases of things such as clothing, restaurant meals, concert tickets, hotel rooms and car services. In the years to come, O2O revenues may rival or even overtake Tencent’s traditional fee-based and advertising (traffic-based) revenues.

Health-Sciences Innovation: Medytox, Inc.

Medytox, Inc. is a South Korean pharmaceutical firm that’s revolutionizing a global product category, which hadn’t changed much in the previous 20 years. That product category is the market for injectable neurotoxins, of which Allergan’s drug Botox is by far the most famous.

Botox is made from botulinum toxin, a lethal toxin that requires highly advanced manufacturing processes. Medytox’s initial strategy was to create Neuronox, a bio-equivalent product to Botox, and thereby gain access to a world-wide market that by 2020 is expected to reach $5.6 billion — roughly double the level from 2013.

Medytox’s bio-equivalent to Botox has grown from an 8% market share in South Korea upon its 2006 launch to 40% in 2014. At the same time that Medytox is taking market share in Korea, the industry itself is growing rapidly for reasons such as an aging Korean population, higher female employment in Korea, and a growing trend of Chinese medical tourism to Korea. These Korea-specific factors, combined with a broad obsession with beauty, make Medytox extremely well-positioned on its home turf.

But the international growth potential is what truly makes Medytox a standout among emerging-market pharmaceutical companies. Currently, Medytox has only a 2.5% share of the category in which Botox dominates on a world-wide basis. That number is set to rise. Medytox has obtained market approval in 27 countries and has registration ongoing in 30 countries. With the firm’s international expansion still in its infancy, Medytox has already risen to become the #1 market-share holder in Japan, Taiwan and Thailand.

Over time, Medytox will continue to launch in additional markets and gain approval for even more medical indications. Those indications aren’t confined to cosmetic purposes, either. In fact, more than half of Botox’s sales are already for therapeutic purposes, such as helping to control migraines, cerebral palsy, overactive bladder, hyperhidrosis and many other conditions. Both the therapeutic and cosmetic segments are set to grow as the neuromodulator category continues to advance.

So far, this discussion has focused on Medytox’s success in duplicating Botox — no small technical feat, in and of itself. But now let’s zero in on innovation, because Medytox is not just a copycat story. Medytox is a prime example of an emerging-market pharmaceutical company that has mastered a process and is applying game-changing innovation. In this industry category, it is Medytox — not Allergan — that is driving the science forward.

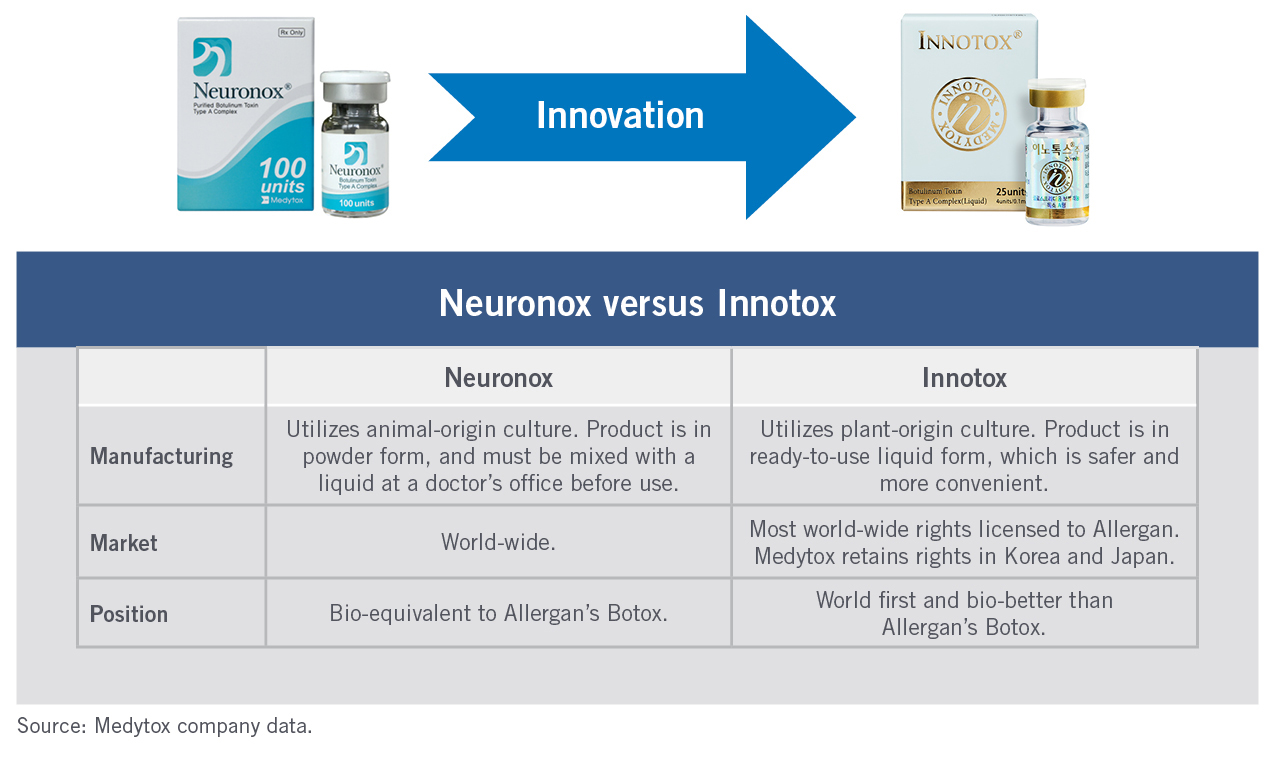

That’s a bold statement, but clearly evidenced by the fact that Allergan has been so impressed with the new technology — still in the approval stages — that Allergan has contracted to license Medytox’s next-generation neurotoxin technology for a substantial fee of $365 million. The “out-licensed” technology includes new manufacturing processes, such as starting from a plant-origin culture rather than the animal-origin culture used for Botox. The license agreement also applies to the manufactured drug itself, which Medytox has named Innotox.

Innotox is “bio-better” than Botox for several reasons, the most important of which is that Innotox is longer-lasting. As a beauty treatment, one of Botox’s advantages is low cost — an average of under $400 per treatment, compared to over $1,800 for fat-transfer surgeries, which are also used to reduce the appearance of wrinkles. But Botox treatments must be renewed every four to six months. Innotox is appealing to patients because it lasts some 20% longer, which reduces the number of doctor visits and procedures that are necessary for the same effect.

The following diagram highlights key differences between Neuronox (which is Medytox’s current bio-equivalent to Botox) and Innotox (which is Medytox’s new bio-better product). For many investors, this degree of innovation in pharmaceuticals — coming from an emerging-market country — is quite a surprise. Medytox serves as a wake-up call emphasizing the many ways that companies domiciled in emerging-market countries are already leading the world.

Medytox is part of a broad, encouraging movement in South Korea, where the government is supporting innovation by entrepreneurial firms. The days in which successful companies had to be part of one of the family-controlled chaebols are over. Medytox and many other innovative Korean health-care companies are located in large, new technology parks. For the most part, these parks were constructed by the Korean government, which has also taken steps to support entrepreneurial firms by arranging venture-capital investments and providing generous research-and-development (R&D) tax incentives.

In the health-care sector, Medytox is one of the most-interesting companies to emerge from this new Korean ecosystem. Medytox has gone far beyond copycatting — which is typical of emerging-market pharmaceutical companies — to become the primary driver of innovation in an established product category. The company’s $365 million licensing deal with Allergan is a cash windfall. But even more importantly, that deal serves to validate the world-class R&D platform Medytox has developed.

Business-Process Innovation: Safaricom Ltd.

Think about mobile-phone usage in the United States and most other developed markets. Sure, the phones work great for communications and social-media applications.

But where on earth is the mobile phone used as the dominant means of making payments and transferring money? Not in most developed markets. However, in Kenya — a country not even rising to the status of an emerging market — an innovative company has leapfrogged the normal evolution of business practices by bringing basic banking services to millions of individuals who’ve never had a traditional bank account.

Kenya is an East African country with a population of about 44 million people. And Safaricom Ltd. is the country’s leading mobile-network/integrated-communications company with over 23 million subscribers. Incidentally, Safaricom is so successful in Kenya that Vodafone Group plc of the United Kingdom maintains an almost 40% stake in the company.

So does Safaricom have some groundbreaking technology that allows it to offer banking services without a bank’s infrastructure? Hardly. If anything, the company offers its services by means of equipment and devices that are often less than state-of-the-art. What Safaricom does have, however, is a dominant customer base of individuals and businesses — which the company has combined with innovative business processes.

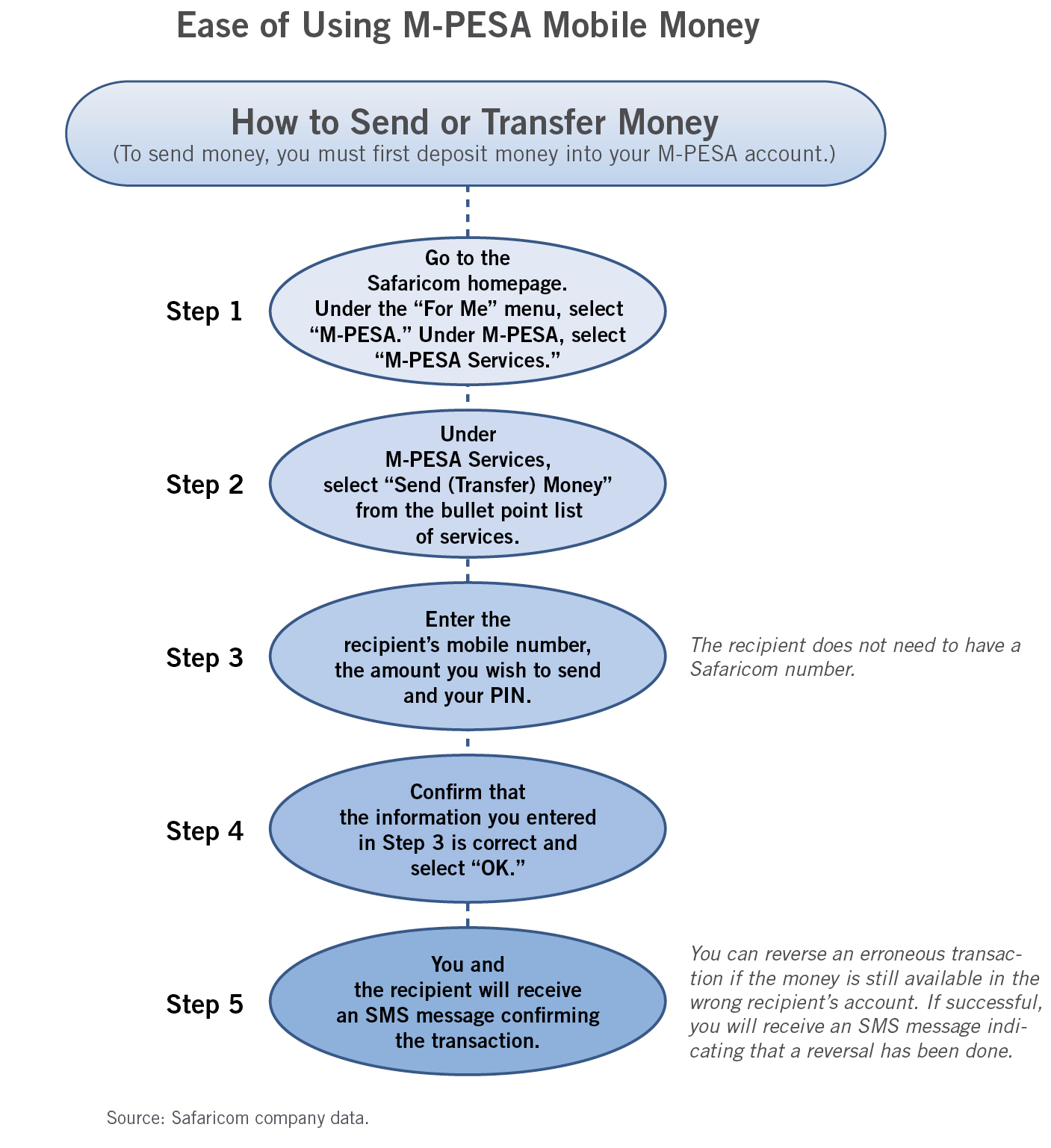

Safaricom’s mobile-money application is called M-PESA, which allows Kenyans to transfer money via short-message service (SMS). With M-PESA, the user can buy electronic cash from any of Safaricom’s 81,000 agents nationwide. This electronic cash can then be sent to another mobile-phone user, which could be an individual or a business. The electronic cash can be kept by the recipient for future transactions, or redeemed at an M-PESA agent for traditional cash denominated in the Kenyan shilling, which is the local currency. The following diagram shows how easy it is to transfer money through M-PESA.

While Safaricom charges a commission for each transaction, the M-PESA commissions are typically much more reasonable than credit-card commissions. This makes M-PESA attractive for businesses selling products and services to customers in person or over the Internet. In fact, M-PESA is an accepted method of payment at over 50,000 stores across the country. Based on this success, Vodafone, which partnered in the development of M-PESA, intends to roll out the mobile-money application internationally as well.

M-PESA started as a person-to-person application, then expanded to person-to-business transactions, and is now accommodating business-to-business relationships. Consider a global consumer-products company selling items in Kenya. Without M-PESA, the delivery person brings the items to the local store, and usually accepts cash as payment. This is cumbersome and prone to theft or graft. With M-PESA, the consumer-products company can keep better track of transactions, and have greater confidence that money is exchanging hands legitimately.

Approximately 90% of all transactions in Kenya are cash-based. Of the rest, figures from the Kenyan central bank indicate that M-PESA accounts for over 70% of non-cash transactions. These figures show that M-PESA has a huge competitive advantage, but also that there’s plenty of headroom for growth. Just think of all the transactions that could be accommodated by M-PESA: payment of salaries, rents, utility bills, tabs at restaurants, and administration of loyalty programs for travel, hotels and ticketing.

While M-PESA’s mobile-money features are mostly used for relatively small transactions, broader banking services — such as savings accounts, mortgages and other large loans — will require relationships with traditional banks. As such, Safaricom has partnered with over 38 banks nationwide. The banks are happy with these partnerships because Safaricom is meeting the needs of previously unbanked people, and is now introducing many of those people to more and more advanced bank-type services. Currently, an M-PESA enabled mobile phone can also function as an electronic wallet to hold up to 100,000 Kenyan shillings — which is functionality supported by Safaricom’s banking partnerships.

Through M-PESA, Safaricom took advantage of the growth opportunity in Kenya’s young, dynamic population that was extremely well-penetrated by mobile phones, but was way underpenetrated by banking relationships. That’s not where Safaricom’s innovation ends, however.

Safaricom’s newest innovation delivers entertainment and Internet access though a device it calls “the BIG box.” In an effort to gain widespread acceptance, Safaricom sells the BIG box without making a profit. Since traditional cable and fiber-optic connectivity are not yet prevalent in Kenya, the BIG box uses 3G/4G connectivity over the airwaves to bring an Internet hotspot (Wi-Fi) into people’s homes. Then, users can access less-data-intensive content right away, including 30 free television channels, YouTube videos and pre-installed games. Alternatively, users can download and record more-data-intensive content (such as full-length movies and music) for viewing and listening at a later date.

Like M-PESA, the BIG box doesn’t require state-of-the-art technology. In fact, the BIG box can be used with old, analog (non-digital/non-USB) televisions, which are almost extinct in the United States. Safaricom’s goal is to get a large customer base hooked on the BIG box as quickly as possible, and then upgrade the service over time with more content and faster connectivity (e.g., fiber-optic installations).

Going forward, the precise development of Safaricom’s business is unclear. But what is clear is that Safaricom considers itself to be something way beyond a telecommunications company. Moreover, with a competitive head start, a large user base, and the “big-data” capabilities to analyze user preferences and buying habits, Safaricom’s potential for growth should be quite significant.

Summary and Conclusions

This discussion has made clear that innovation is occurring in emerging and frontier markets, and that innovation is creating opportunities for investors beyond commodity exporters and basic consumer-goods companies. In addition, emerging- and frontier-market innovation is especially exciting because it’s being applied to growing populations with expanding middle-class segments.

But how can investors take advantage of this innovation? Firsthand, on-the-ground research is important because third-party information is less prevalent and less reliable in these countries. As a result, those willing and able to do the hard work are more likely to find better opportunities. Having said that, once a company has proven its success, public stock-market valuations and private valuations can be quite substantial, as indicated in the table on the previous page.

Moreover, stock-transaction liquidity has been improving in emerging- and frontier-market countries, which should further enhance valuations over time. And many smaller innovative companies in these countries pay attractive dividends, which is less common among small-cap companies in the United States and other developed markets.

About the LEAD Portfolio Managers for Wasatch’s emerging and frontier markets funds

Ajay Krishnan is the Lead Portfolio Manager for the Wasatch Emerging Markets Select and Emerging India Funds. He is also a Portfolio Manager for the Wasatch Global Opportunities Fund. He was a Portfolio Manager for the Ultra Growth Fund from 2000 to 2013. In addition, he was a Portfolio Manager for the World Innovators Fund from 2000 to 2007. He joined Wasatch Advisors as a Research Analyst in 1994. He was a Research Analyst on the Ultra Growth Fund prior to becoming a Portfolio Manager.

Mr. Krishnan earned a Master of Business Administration from Utah State University, where he also worked as a graduate assistant. He completed his undergraduate degree at Bombay University, earning a Bachelor of Science in Physics with a Minor in Mathematics.

Mr. Krishnan is a CFA charterholder and a member of the Salt Lake City Society of Financial Analysts. He specializes in analyzing the investment potential of fast-growing companies.

Ajay is a native of Mumbai, India and speaks Hindi and Malayalam. He enjoys traveling, reading, playing squash and road biking.

Roger Edgley is Director of International Research and the Lead Portfolio Manager for the Wasatch International Growth Fund and the Wasatch Emerging Markets Small Cap Fund. He is also a Portfolio Manager for the Wasatch Emerging Markets Select Fund. In addition, he was the Lead Portfolio Manager for the Wasatch International Opportunities Fund from 2005 to 2015. He joined Wasatch Advisors in 2002 and is a member of the Board of Directors. A native of the United Kingdom, he also holds U.S. citizenship and has many years of international investing experience.

Prior to joining Wasatch Advisors, Mr. Edgley was a principal, director of international research and portfolio manager for Chicago-based Liberty Wanger Asset Management, which managed the Acorn Funds. He was also a co-manager for the Acorn Foreign Forty Fund. Earlier, he worked in Hong Kong as a financial-services analyst for Societe Generale Asia/Crosby Securities and as an analyst for Strategic Asset Management.

Mr. Edgley has a Master of Arts in Philosophy from the University of Sussex and a Master of Science in Social Psychology with Statistics from the London School of Economics, where he was awarded a Social Science Research Scholarship. He earned a Bachelor of Science with honors in Psychology from the University of Hertfordshire. He is also a CFA charterholder.

Laura Geritz is the Lead Portfolio Manager for the Wasatch Frontier Emerging Small Countries Fund and the Wasatch International Opportunities Fund. She was a Portfolio Manager for the Wasatch Emerging Markets Small Cap Fund from 2009 to 2015. She first joined Wasatch Advisors in 2006 as a Senior Equities Analyst on the international research team.

Before joining Wasatch Advisors, Ms. Geritz worked as a senior analyst for Mellon Corporation, where she made investment recommendations for two of the company’s small-cap growth funds. Prior to joining Mellon Corporation, she spent four years analyzing securities for various products at American Century Investments, where her stock selections represented approximately one-third of the assets held in each mid-cap growth portfolio.

Ms. Geritz graduated with honors from the University of Kansas with a Bachelor of Arts in Political Science and History. Later, she earned a Master’s Degree in East Asian Languages and Cultures. Before completing her Master’s Degree, she spent one year in Japan, where she translated and interpreted documents for the Board of Education and wrote and broadcast a weekly radio program in both English and Japanese. She is also a CFA charterholder and a member of the Denver Society of Financial Analysts.

About Wasatch Advisors®

Wasatch Advisors is the investment manager to Wasatch Funds,® a family of no-load mutual funds, as well as to separately managed institutional and individual portfolios. Wasatch Advisors pursues a disciplined approach to investing, focused on bottom-up, fundamental analysis to develop a deep understanding of the investment potential of individual companies. In making investment decisions, the portfolio managers employ a uniquely collaborative process to leverage the knowledge and skill of the entire Wasatch Advisors research team.

Wasatch Advisors is an employee-owned investment advisor founded in 1975 and headquartered in Salt Lake City, Utah. The firm had $17.4 billion in assets under management as of October 31, 2015. Wasatch Advisors, Inc. is registered with the Securities and Exchange Commission under the Investment Advisers Act of 1940.

RISKS

In addition to the risks of investing in foreign securities in general, the risks of investing in the securities of companies domiciled in frontier and emerging markets countries include increased political or social instability, economies based on only a few industries, unstable currencies, runaway inflation, highly volatile securities markets, unpredictable shifts in policies relating to foreign investments, lack of protection for investors against parties that fail to complete transactions, and the potential for government seizure of assets or nationalization of companies.

Investing in small cap funds will be more volatile and loss of principal could be greater than investing in large cap or more diversified funds.

Being non-diversified, the Wasatch Emerging Markets Select Fund can invest a larger portion of its assets in the stocks of a limited number of companies than a diversified fund. Non-diversification increases the risk of loss to the Fund if the values of these securities decline.

An investor should consider investment objectives, risks, charges, and expenses carefully before investing. To obtain a prospectus, containing this and other information, visit www.WasatchFunds.com or call 800.551.1700. Please read it carefully before investing.

Information in this document regarding market or economic trends or the factors influencing historical or future performance reflects the opinions of management as of the date of this document. These statements should not be relied upon for any other purpose. Past performance is no guarantee of future results, and there is no guarantee that the market forecasts discussed will be realized.

The investment objective of the Wasatch Emerging Markets Select, Wasatch Emerging Markets Small Cap, Wasatch Frontier Emerging Small Countries, and Wasatch Emerging India Funds is long-term growth of capital.

As of September 30, 2015, the Wasatch World Innovators Fund had 0.7% of net assets in Alibaba Group Holding Ltd. and 2.1% of net assets in Google, Inc., the Wasatch Emerging Markets Select Fund had 3.5% of net assets in Medytox, Inc., the Wasatch Emerging Markets Small Cap Fund had 1.7% of net assets in Medytox, Inc., the Wasatch Frontier Emerging Small Countries Fund had 1.1% of net assets in Safaricom Ltd., the Wasatch Global Opportunities Fund had 2.4% of net assets in Medytox, Inc., the Wasatch International Growth Fund had 2.0% of net assets in Medytox, Inc. None of the Wasatch Funds were invested in Tencent Holdings Ltd., eBay, Inc., Facebook, Inc., LinkedIn Corp., Nintendo Co. Ltd., Allergan, Inc. or Vodafone Group plc as of September 30, 2015. Portfolio holdings are subject to change at any time. References to individual companies should not be construed as recommendations by the Funds or the Advisor. Current and future holdings are subject to risk.

CFA® is a trademark owned by CFA Institute.

ALPS Distributors, Inc. is not affiliated with Wasatch Advisors.

DEFINITIONS

The word “chaebol” means “business family” or “monopoly” in Korean. The chaebol structure can encompass a single large company or several groups of companies. Each chaebol is owned, controlled or managed by the same family dynasty, generally that of the group’s founder.

The “cloud” is the Internet. Cloud-computing is a model for delivering information-technology services in which resources are retrieved from the Internet through web-based tools and applications, rather than from a direct connection to a server.

The Hong Kong Stock Exchange, one of the world’s largest securities markets by market capitalization, traces its origins to the founding of China’s first formal securities market, the Association of Stockbrokers in Hong Kong, in 1891. A second market opened in 1921, and in 1947 the two merged to form the Hong Kong Stock Exchange.

Valuation is the process of determining the current worth of an asset or company.

© 2015 Wasatch Funds. All rights reserved. Wasatch Funds are distributed by ALPS Distributors, Inc. WAS003943 1/30/2017