As we near year-end, it seems appropriate to take a macro look at the US economy. This week, I’ll look at the US consumer while next I’ll take a look at business.

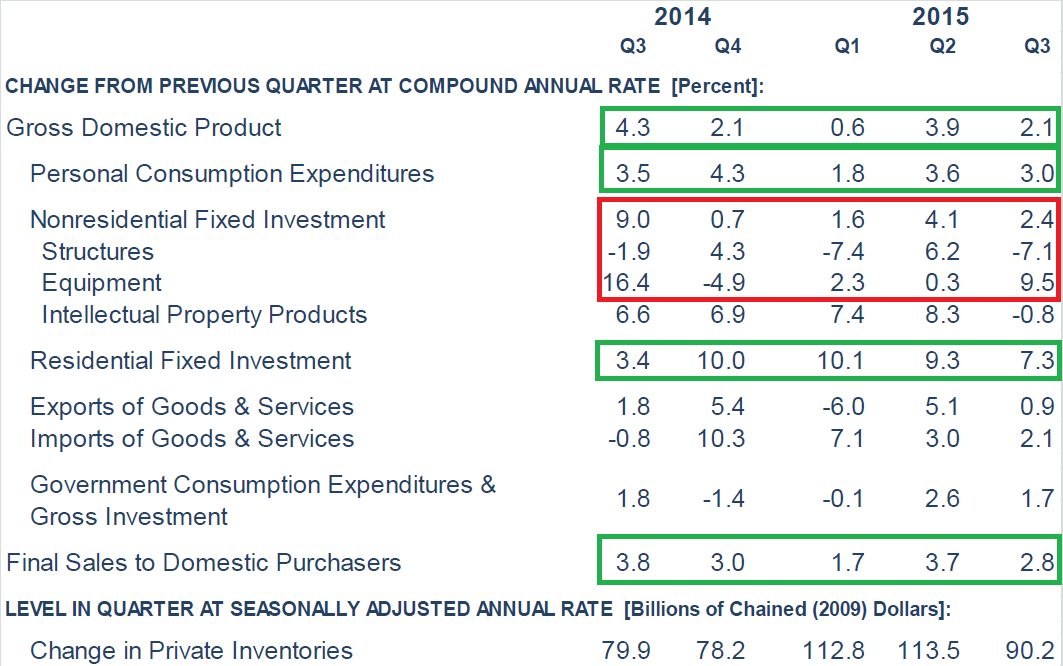

Let’s start with a table from the Richmond Fed’s monthly chart pack:

The US consumer and domestic demand continues to power the economy. Personal consumption expenditures (PCEs) increased over 3% in 4 of the last 5 quarters. Domestic demand, rose over 3% in 3 of the last 5 quarters, and grew 2.8% last quarter. Overall, these are important numbers, indicating consumer spending is solid.

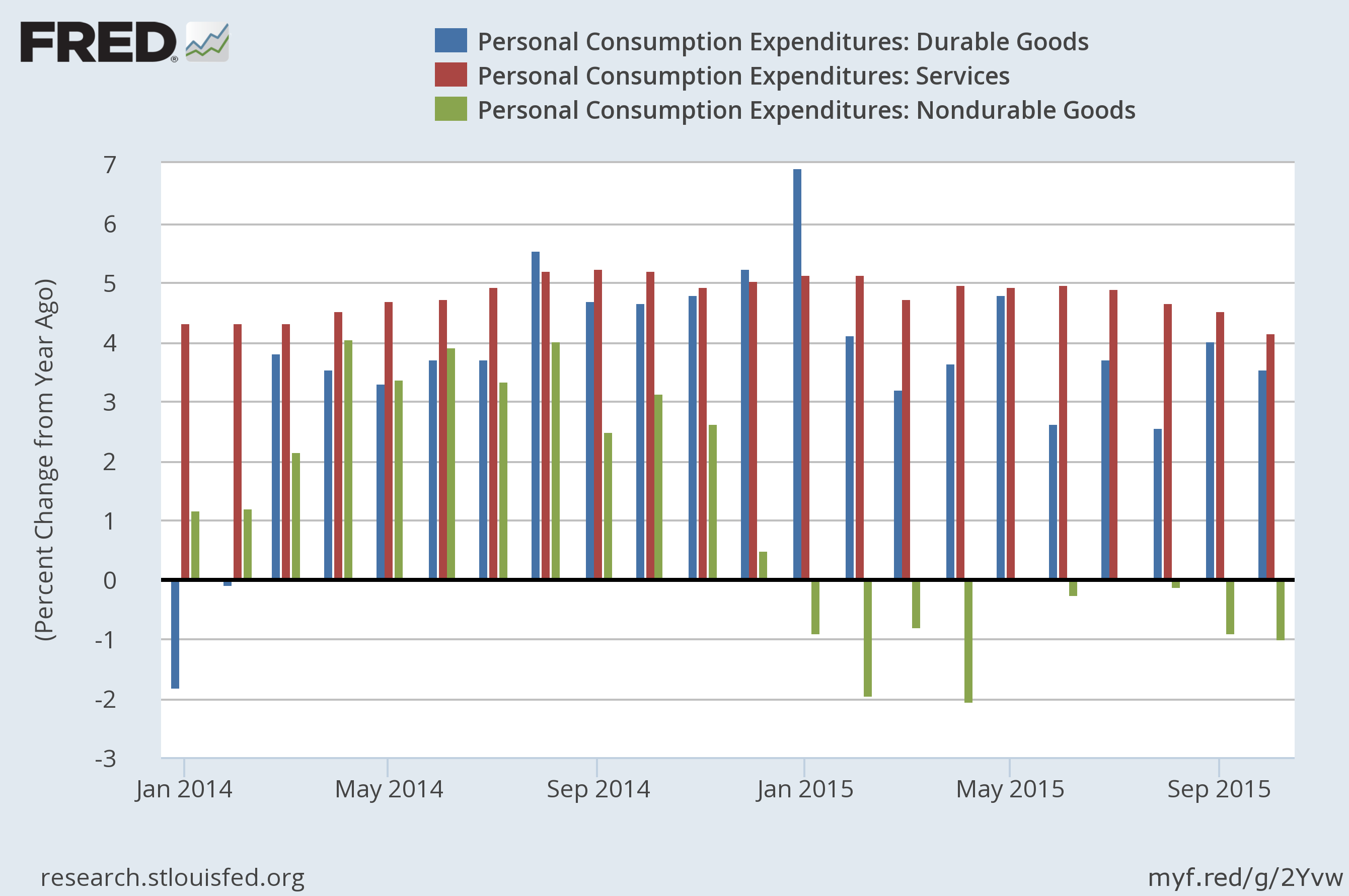

Let’s take a deeper look and spending:

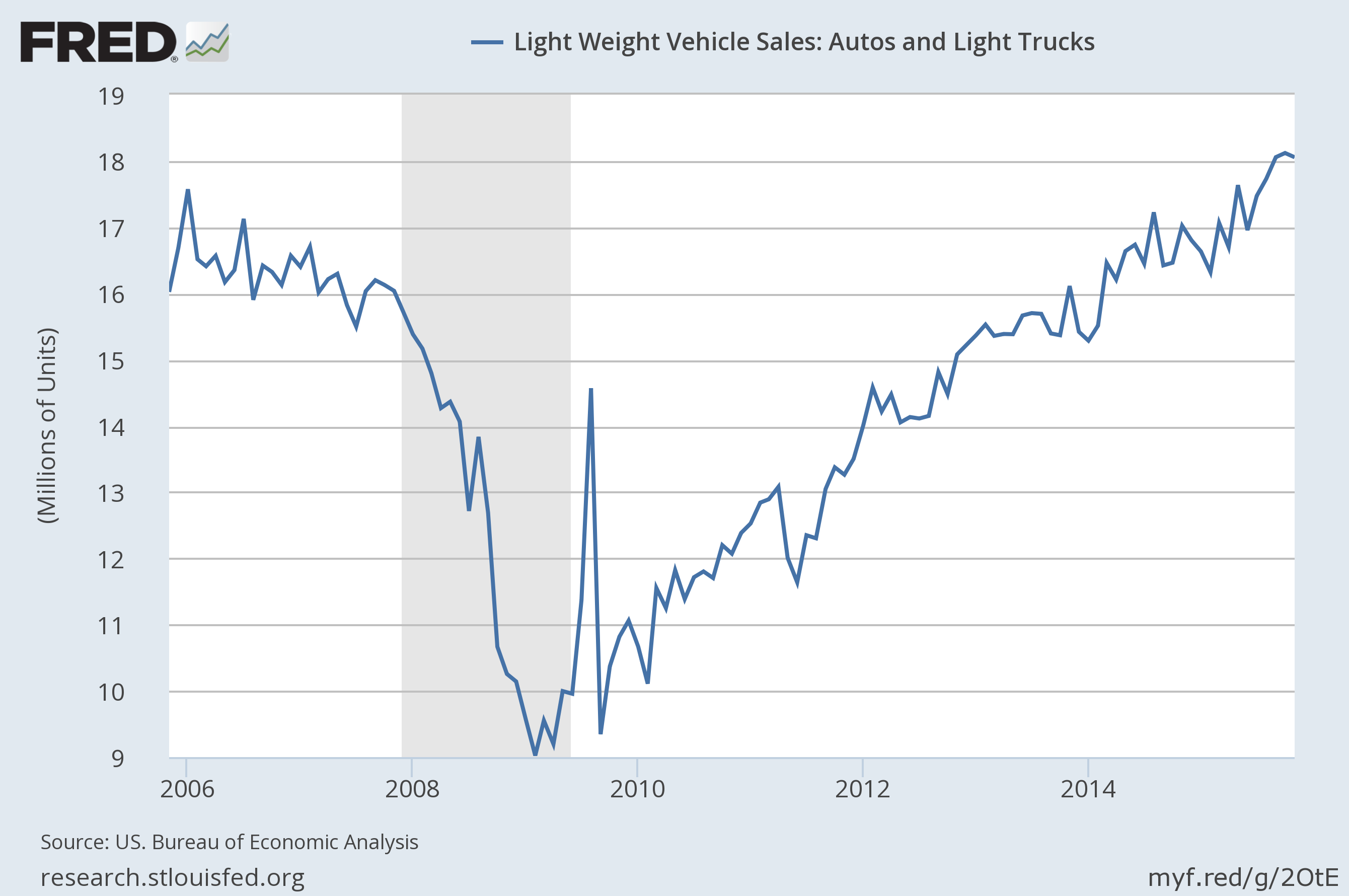

The graph above is from the St. Louis FRED system, and it shows monthly Y/Y percentage change in sub-categories of PCEs – durable goods (blue), non-durable goods (green) and services (red). Service spending is solid, increasing consistently from 4%-5% Y/Y for the last year. Durables goods are also strong; they’re up between 2.5% and 5% on a monthly basis for the last year. However, non-durable spending is weak; it’s contracted in 8 of the last 12 months. Two charts add additional definition to this data, starting with auto and light truck sales:

Car sales have risen consistently since just after the end of the recession. They are now near record levels.

But real retail sales are weakening a bit, falling to 1% Y/Y in their latest reading.

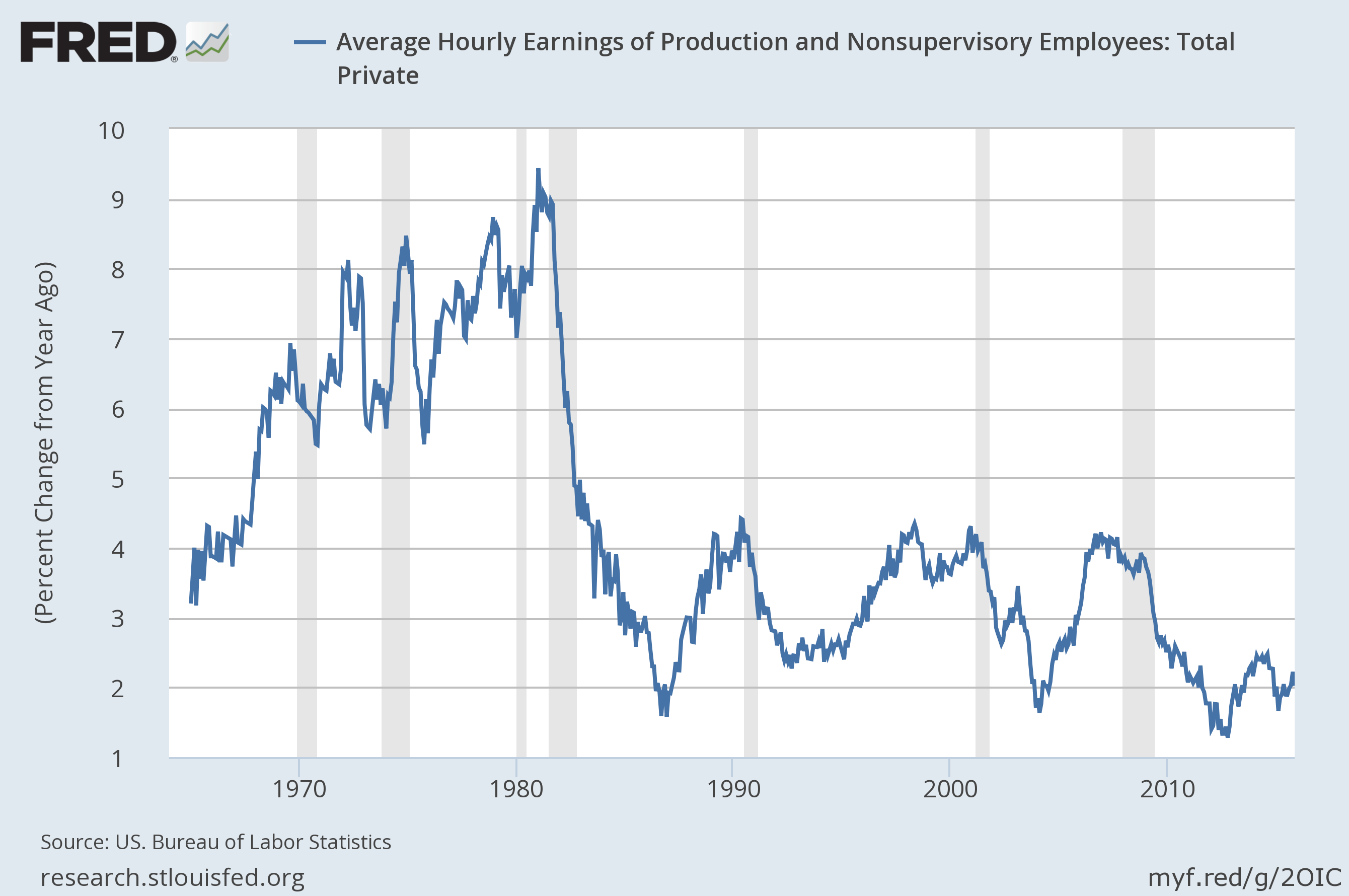

As for the source of spending, there are three important charts:

Real wage growth is still very weak, not only historically, but for where we are in the expansion. However,

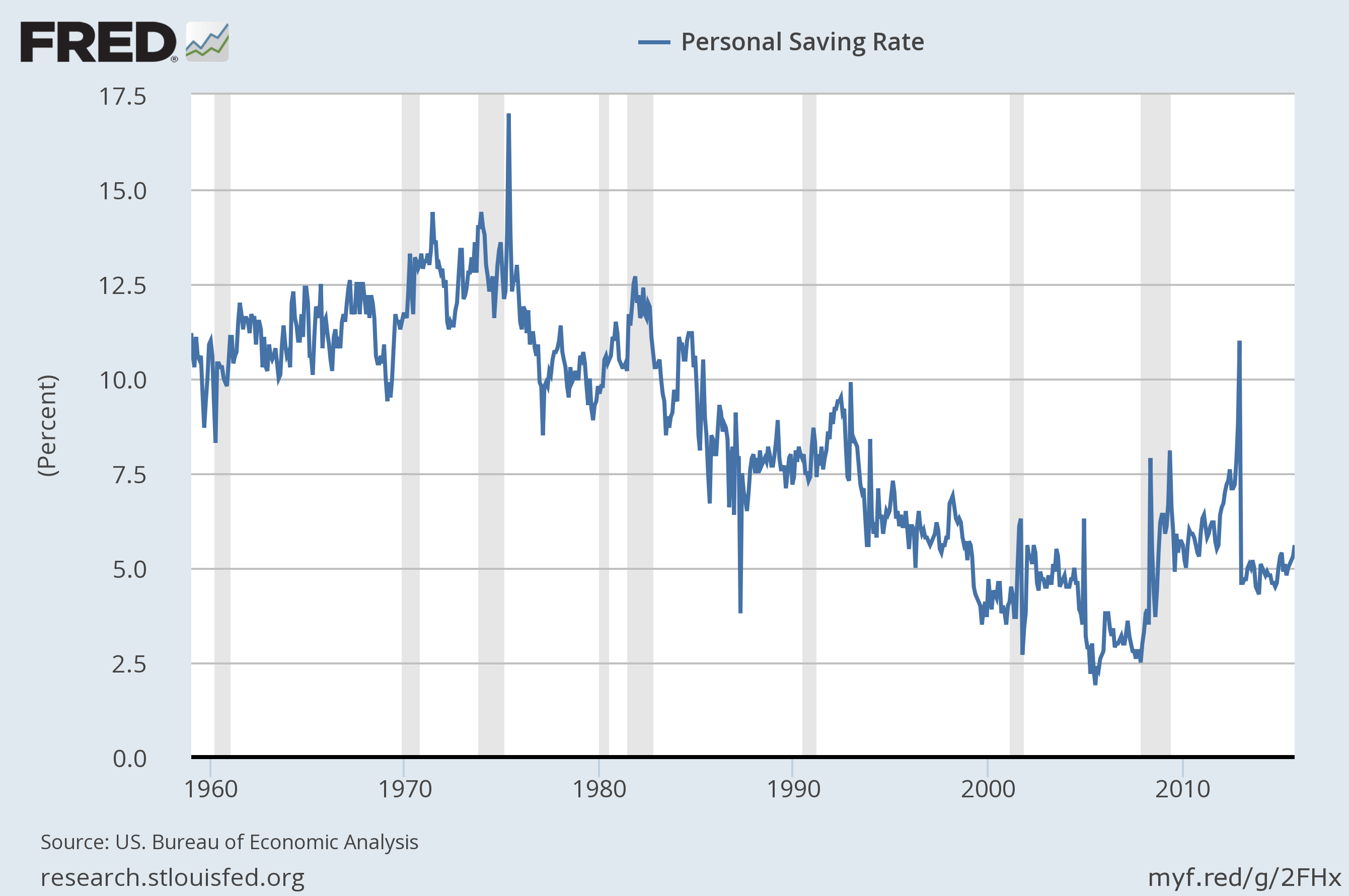

The personal savings rate is ~5%, and has been since the end of the recession. And perhaps best of all:

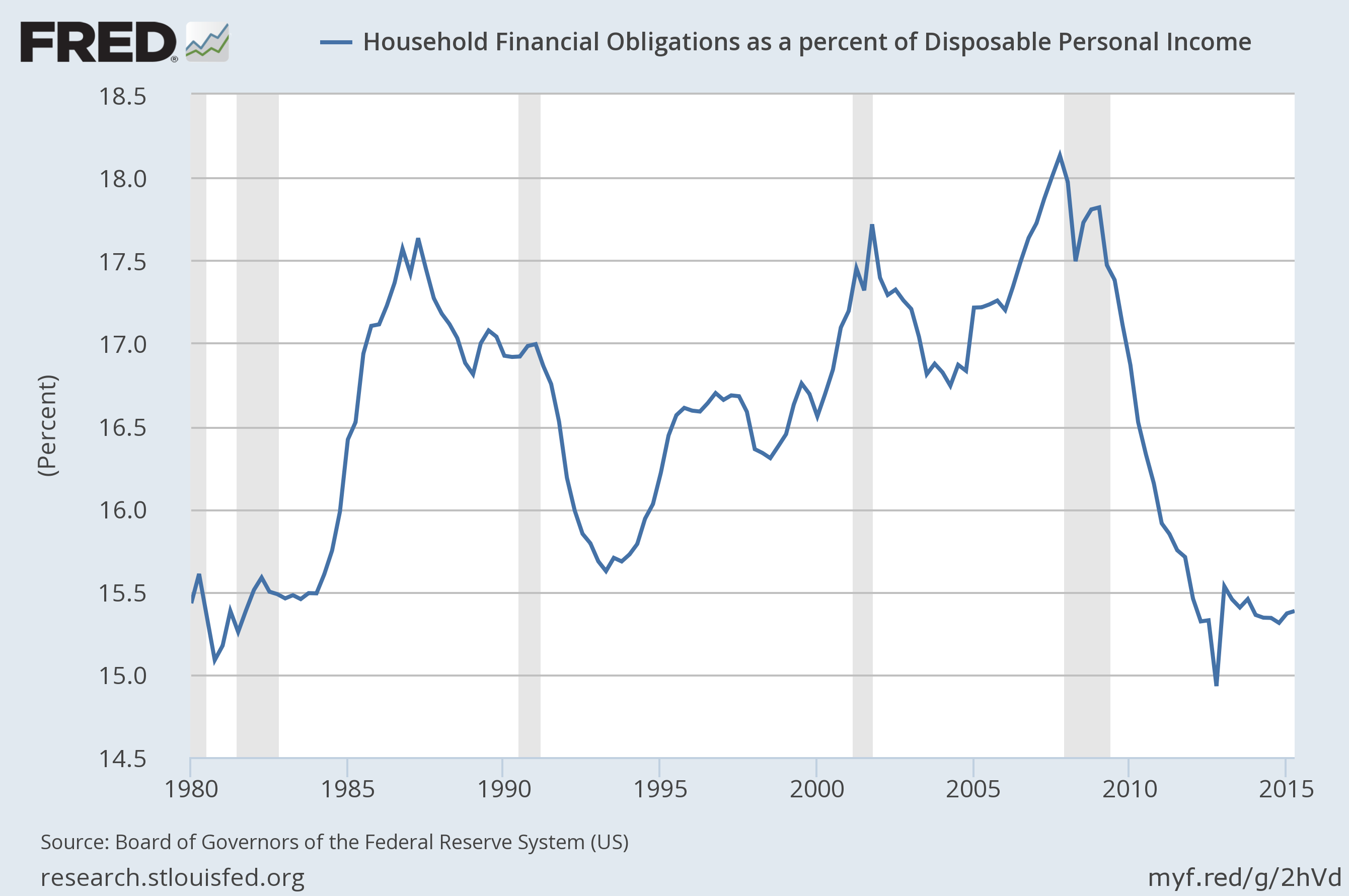

US households have cleaned up their balance sheets.

Let’s sum up: the US consumer is spending at a solid pace. Perhaps most importantly, he’s buying cars in record numbers, indicating a fairly high amount of confidence in the next 2-3 years. While wage growth is very weak, there is a higher savings cushion that could continue to provide funding. And, household balance sheets are in their best shape in over 30 years. In short, there’s a great deal of bullishness provided by the above data.

Market

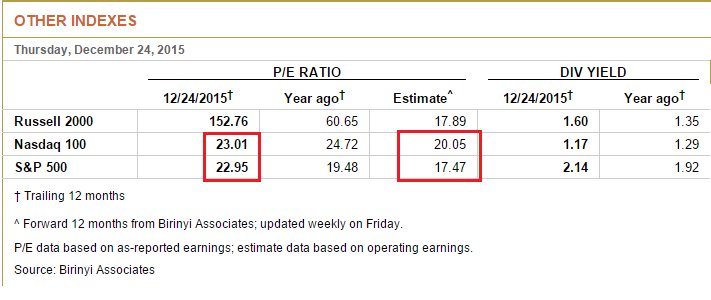

The markets remain expensive:

The markets need revenue and meaningful earnings growth to move higher. Unfortunately, they’re not going to get it. In this interview, Zacks’ lead analyst uses the phrase, “earnings recession.” And Factset is predicting a fourth straight quarter of revenue declines:

The estimated revenue decline for Q4 2015 is -3.2%. If this is the final revenue decline for the quarter, it will mark the first time the index has seen four consecutive quarters of year-over-year revenue declines since Q4 2008 through Q3 2009. Six sectors are expected to report year-over-year growth in revenues, led by the Telecom Services and Health Care sectors. Four sectors are expected to report a year-over year decline in revenues, led by the Energy and Materials sectors.

Essentially, there is nothing good in the fourth quarter predictions.

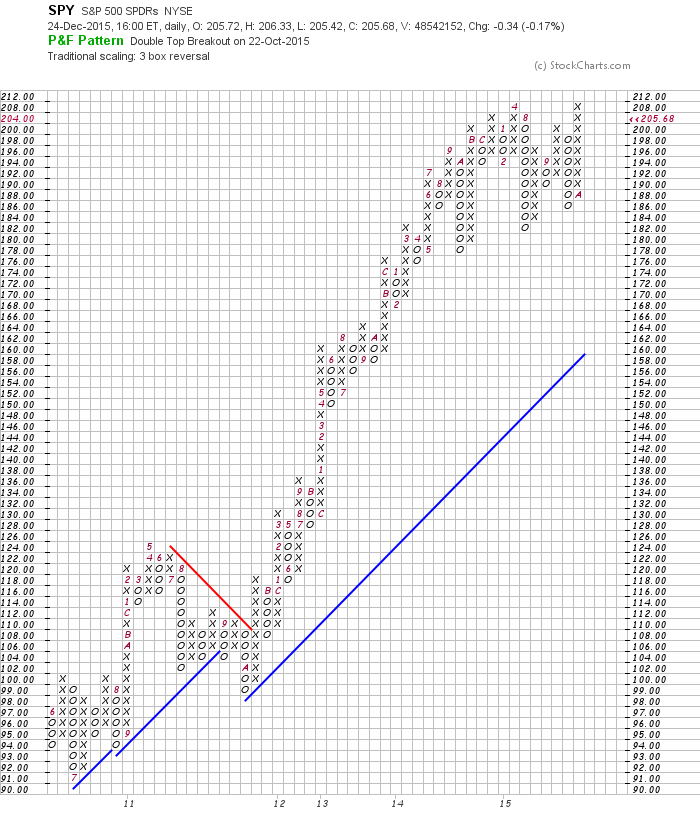

Over the last quarter, I’ve noted the stalled nature of the SPYs rally. This P&F chart really highlights that issue:

The market topped in April and hasn’t moved meaningfully higher since. It’s also we could be seeing a long-term double top. And that possibility, combined with weaker revenue growth, is a big reason I’m slightly bearish going forward.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis