Weighing the Week Ahead: A Parade of Pontificating Pundits!

Last week’s stock market had a Jekyll and Hyde feeling, setting the background for the two weeks ahead. We will have lighter volume and plenty of people taking vacation during the holiday-shortened weeks. With plenty of explaining to do and a new year ahead, we can expect:

A Parade of Pontificating Pundits!

Prior Theme Recap

In my last WTWA I predicted that the market stories for the week would consider the possibility of a Santa Claus rally. That was the right question, since it got plenty of buzz from the media, but my suggested answer – “Yes” – looked good for only part of the week. While it is still technically possible to see Santa (last five trading days and first two of the New Year is the “official” definition) it is not looking good. For the full story, let us look at Doug Short’s weekly chart. Doug’s full post quashes the Santa Rally idea and shows the various relevant moving averages in another very negative week for stocks. (With the ever-increasing effects from foreign markets, you should also add Doug’s World Markets Weekend Update to your reading list).

Doug’s update also provides multi-year context. See his full post for more excellent charts and analysis.

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

This Week’s Theme

The long-awaited change in Fed policy had a dramatic effect on Wednesday—all good. Everything – stocks, the dollar, interest rates, commodities – all changed course on Thursday. This provides plenty of grist for pundits to explain the Jekyll and Hyde market mentality of the week just passed. Since it is also time for end-of-year explanations and predictions, we can expect —

A Parade of Pontificating Pundits!

There will be a wide range of viewpoints projecting a few days of trading into the year ahead:

- The U.S. is on the cusp of a recession, dragged down by the rest of the world. (This is drawing a lot of supporters already).

- This is the start of the reaction to over-valuation and declining profit margins.

- The Fed emphasis has now shifted to the pace of increases.

- Last week was more of what we have recently seen – reaction to energy trading – but exaggerated by options expiration.

- More tax loss selling. Time for a rally.

As always, I have my own opinion in the conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

Despite the negative result for stocks, there was plenty of good news last week.

- The Omnibus Spending Bill easily passed through the House and Senate this week. It will rule out any fears of a government shutdown until September. It’s a refreshing change to see bipartisan compromise in Washington, and should help to stimulate the economy well into next year.

- L.A. Port Traffic is strong, with a November gain of 6.6% year-over-year. Calculated Risk (great comprehensive coverage this week) has the story, analysis, and charts.

- Leading economic indicators from the Conference Board solidly beat expectations, 0.4% versus 0.1%.

- Bullish sentiment at a three-year low. Bespoke via Brian Gilmartin.

- Housing news was strong. Building permits and housing starts both beat expectations. Calculated Risk notes the relatively warm November weather, but also highlights the strong (double digit increase) comparisons with this time in 2014. It has been a good year for housing. (See also New Deal Democrat’s analysis).

- Initial jobless claims edged lower to 271K, beating expectations by more than 10K.

- Mortgage equity withdrawal was the best since 2008. Calculated Risk has the full story, explaining how rising home prices have helped spendable income, even though debt has declined.

The Bad

Some of the economic data was disappointing.

- FedSpeak (post Yellen press conference) was negative. The Friday comments from Richmond Fed President Jeff Lacker – four increases is what the Fed means by gradual – was inconsistent with market expectations of two or maybe three rate hikes. There is still a significant disparity between Fed and market perceptions about the overall strength of the economy as well as the probably pace of rate hikes.

- Industrial production was weak, declining by 0.6%.

- Rail data weakened again. Steven Hansen at GEI has the story.

The Ugly

The checkered past of Martin Shkreli, the wildly unpopular person who bought a company so that he could jack up the price of one of its life-saving drugs. He was arrested this week on the unrelated case of Ponzi-type securities fraud. Matt Levine at Bloomberg View (Martin Shkreli Accused of Being Surprisingly Good at Fraud) has a good description of his past misdeeds and some interesting questions, e.g., What if he shorted biotech stocks before going public with the 5000% price increase story? Andy Borowitz has a more humorous take.

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. No award this week, but nominations are always welcome.

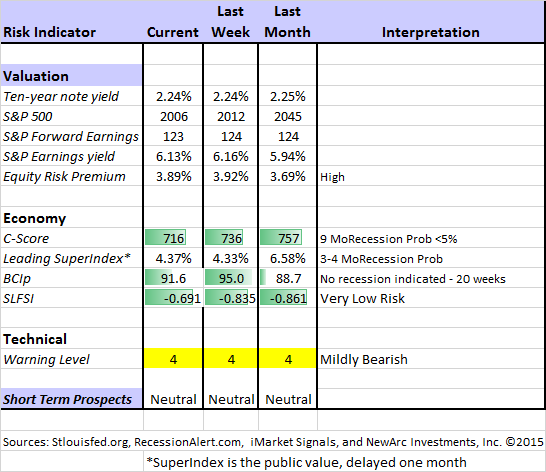

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. Beginning last week I made some changes in our regular table, separating three different ways of considering risk. For valuation I report the equity risk premium. This is the difference between what we expect stocks to earn in the next twelve months and the return from the ten-year Treasury note. I have found this approach to be an effective method for measuring market perception of stock risk. This is now easier to monitor because of the excellent work of Brian Gilmartin, whose analysis of the Thomson-Reuters data is our principal source for forward earnings.

Our economic risk indicators have not changed.

In our monitoring of market technical risk, I am using our “new” Oscar model. I put “new” in quotes because Oscar is in the same tradition as Felix and the product of extensive testing. We have found that the overall market indication is more helpful for those investing or trading individual stocks. The score ranges from 1 to 5, with 5 representing a high warning level. The 2-4 range is acceptable for stock trading, with various levels of caution.

Oscar improves trading results by taking some profits during good times and getting out of the market when technical risk is high. This is not market timing as we normally think of it, since it is not an effort to pick tops and bottoms and it does not go short. Instead, Oscar identifies and limits risk. (More to come about Oscar).

I considered continuing to report the Felix updates, but I already have a distinction between long and short-term methods. I want to minimize confusion. Those who want this information can subscribe to our weekly Felix updates.

In my continuing effort to provide an effective investor summary of the most important economic data I have added Georg Vrba’s Business Cycle Index, which we have frequently cited in this space. In contrast to the ECRI “black box” approach, Georg provides a full description of the model and the components.

For more information on each source, check here.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

Georg Vrba: provides an array of interesting systems. Check out his site for the full story. We especially like his unemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result with the twenty-week forward look from the Business Cycle Indicator, updated weekly and now part of our featured indicators.

Doug Short: Provides an array of important economic updates including the best charts around. One of these is monitoring the ECRI’s business cycle analysis, as his associate Jill Mislinski does in this week’s update. His Big Four update is the single best visual update of the indicators used in official recession dating. You can see each element and the aggregate, along with a table of the data. The full article is loaded with charts and analysis.

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting systems. These include approaches helpful in both economic and market timing. He has been very accurate in helping people to stay on the right side of the market.

The Week Ahead

This is a relatively light week for economic data. While I highlight the most important items, you can get an excellent comprehensive listing at Investing.com. You can filter for country, type of report, and other factors.

The “A List” includes the following:

- New Home Sales (W). An important proxy for growth in construction.

- Personal Income and Spending (W). Both are important for consumption as an economic driver. Recent gains suggest robust holiday spending.

- Michigan Sentiment (W). A good concurrent indicator of job growth and spending.

- Initial claims (Th). Fastest and most accurate update on job losses.

The “B List” includes the following:

- Existing Home Sales (T). Not as important as new home sales, but shows the state of the market.

- Durable Goods (W). Volatile but interesting.

- PCE prices (W). The favorite Fed indicator, edging above the 2% target.

- GDP – Third Estimate (T). Backward looking, revised slightly lower?

- Crude oil inventories (W). Continued focus on oil prices keeps this report in the spotlight.

It will be a quiet week for official speechifying.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Oscar continues Felix’s neutral market forecast, but we have a bearish lean. He started selling on Tuesday and is now about 20% invested. There are often plenty of good investments, even in an expected flat market. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix and Oscar’s weekly ratings updates via email to etf at newarc dot com. They appear almost every day at Scutify.

How to learn by analyzing your best trades (SMB). A refreshing change from analyzing just your mistakes!

Look over Brett Steenbarger’s shoulder via his trading log for last week’s exciting action.

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page (just updated!) summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking. Pick a topic and give it a try.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important source, it would be the CNBC interview with Leon Cooperman. He has an excellent take on the current economy (solid), the long-term implications of low energy prices (positive), the trailing performance of value stocks (temporary and short-term), and the likely winners for next year. Take some time and watch as much of this as you can.

Stock and Fund Ideas

Eddy Elfenbein has announced his buy list for 2016. He has a great record with these picks, even though he sticks with them throughout the year. This is always a source for great ideas.

ADP? Or cloud competitors? Blue Harbinger does a careful fundamental analysis and provides specific advice.

Apple – Have iPhone sales peaked? (Felix Richter via GEI). 2016 is projected in this chart. Hmm…

Investment Time Horizon

Cullen Roche explains the futility of tracking the annual forecasts: You need to think in a longer term.

Cliff Asness (via Alpha Architect) explains that active investing is “easy, but not simple.” In particular, it requires a lot of patience. He shares this chart showing the timing of the launch of his own fund.

And the things that did NOT happen last year, but might have taken your eye off of the ball. (Barry Ritholtz)

Economic Reactions

Suppose you could have your own “Beige Book”. The FOMC likes to have a report from each District providing some anecdotal evidence to supplement the data. Avondale Asset management does something similar by tracking the news and corporate conference calls. This week it emphasizes CEO’s and the Fed.

Watch out for….

Junk bonds. It is often better reward versus risk to buy the underlying stocks – greater upside, same downside. Matthew C. Klein (FT Alphaville) has a good post on this topic.

Private lending stocks. FT Alphaville has an update with analysis of specific names.

High dividend stocks. Perhaps riskier than you think! (Larry Swedroe).

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for over ten years. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. There are several great links, but I especially liked Vanguard’s advice to young investors. My favorite Millennial explained that the author took some liberties with YOCO, a take on YOLO. Glad to know that!

Final Thoughts

- Last week. I have frequently noted that I do not believe in delayed reactions to events, particularly when the events are widely followed and anticipated. The Fed decision was well-received and well-communicated. On Thursday the correlation with oil prices resumed. Big moves are often exaggerated during options expiration week. Options thought to be dead come back to life, stimulating last-minute covering, hedging, and profit-taking.

- Expertise is specialized. Being a bond king or billionaire is certainly evidence that you have done something really well. It does not make you an expert on everything. You would not go to one of these people for brain surgery. What makes you think they know more about recession forecasting? Each may have some interesting information and be helpful on a piece of the economic puzzle. None of them have impressive track records. (See Barry Ritholtz for more on this theme; and, Ben Carlson adds an interesting list of widely-held beliefs from not that long ago).

-

The fixation on oil prices continues. This is not a solid economic indicator since it reflects both demand (which has been solid) and supply (which has been excessive). The energy sector continues to lead the entire market, including many stocks that are obviously not related. This disparity represents a big opportunity for long-term value investors. The chart below illustrates two points:

- Oil prices reflect over-supply, not lagging growth in demand

- The current “glut” would be absorbed with a consumption increase of 1 – 2%, probably not what is suggested by the term.

Here is the current chart of supply and demand

Personal Note

Some readers have suggested that I am also a pundit. Indeed! I try to take the role of a friend attempting to help readers navigate a confusing mass of information. If I get on a soap box, I try to confine it to the final section of each WTWA. In short, I show many viewpoints as well as offering my own opinion. I especially aim to highlight some of the best things from my own research.

I am delighted that so many people have commented or written to say that they find WTWA to be useful. I wish all of my readers a Merry Christmas, Happy Holidays, and success in the Year Ahead. I will probably not write next weekend while I spend some time with family and work on my annual preview article. In the meantime, we will have some of our year-end awards.