US Equity and Economic Review; Good Economic But Weaker Technical Environment, Edition

US economic news was strong. The Fed raised rates (see the bond market review for detailed analysis), indicating their confidence in the economic environment. Both LEIs and CEIs increased; the former rose smartly, while the later are a bit weak thanks to the shallow industrial recession. Housing starts and permits also rebounded. The markets, however, are weakening. The SPYs are fluctuating around the 200 day EMA; the IYTs are flirting with 1-year lows and the IWMs are 2.5% below their 200 day EMA. The QQQs are the only average in relatively strong technical shape. But the breadth of overall weakness indicates their most likely move is slightly lower.

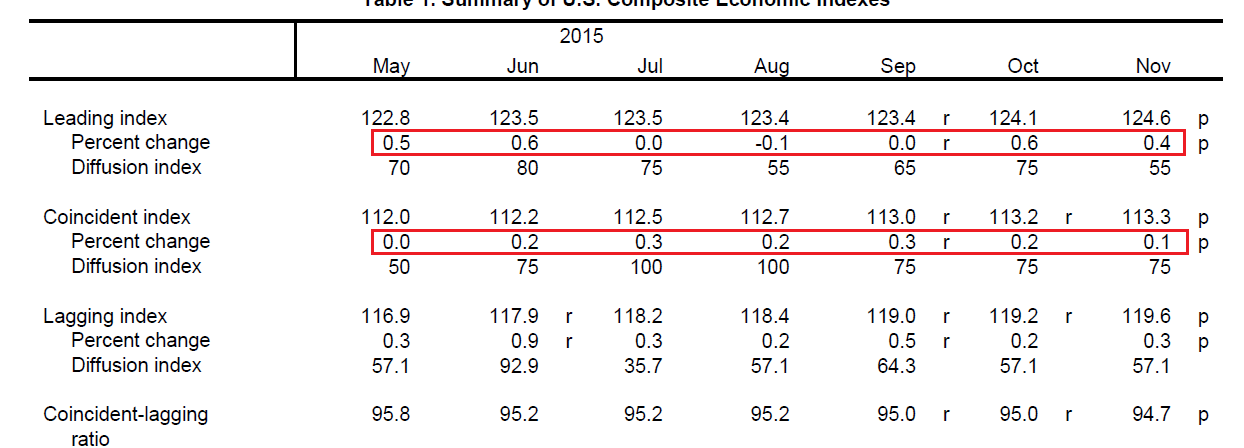

LEIs increased .4%. They have increased strongly in 4 of the last 6 months. CEIs, while increasing, are rising at a slower pace:

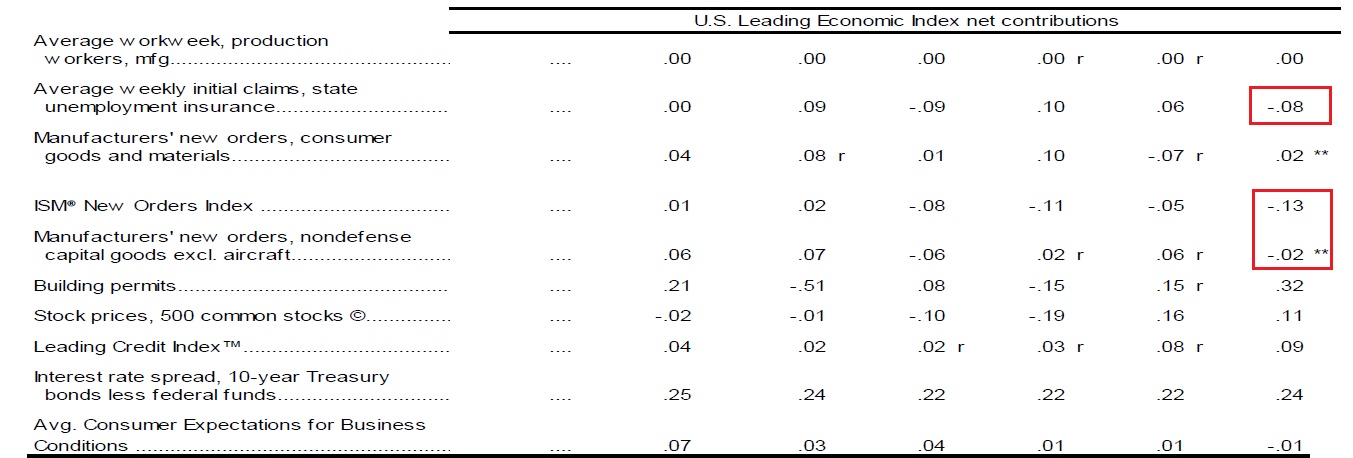

While new industrial orders continue their weakness, new building permits and interest rates remain strong contributors to the LEIs:

Industrial production is clearly the primary reason for weaker CEI readings; it has only been a strong contributor in 1 of the last 6 months:

The LEIs and CEIs remain useful statistics for two reason: they combine a large amount of important information into a single useable number and they have a history of being right. The latest reading points to continued weaker growth thanks to industrial weakness.

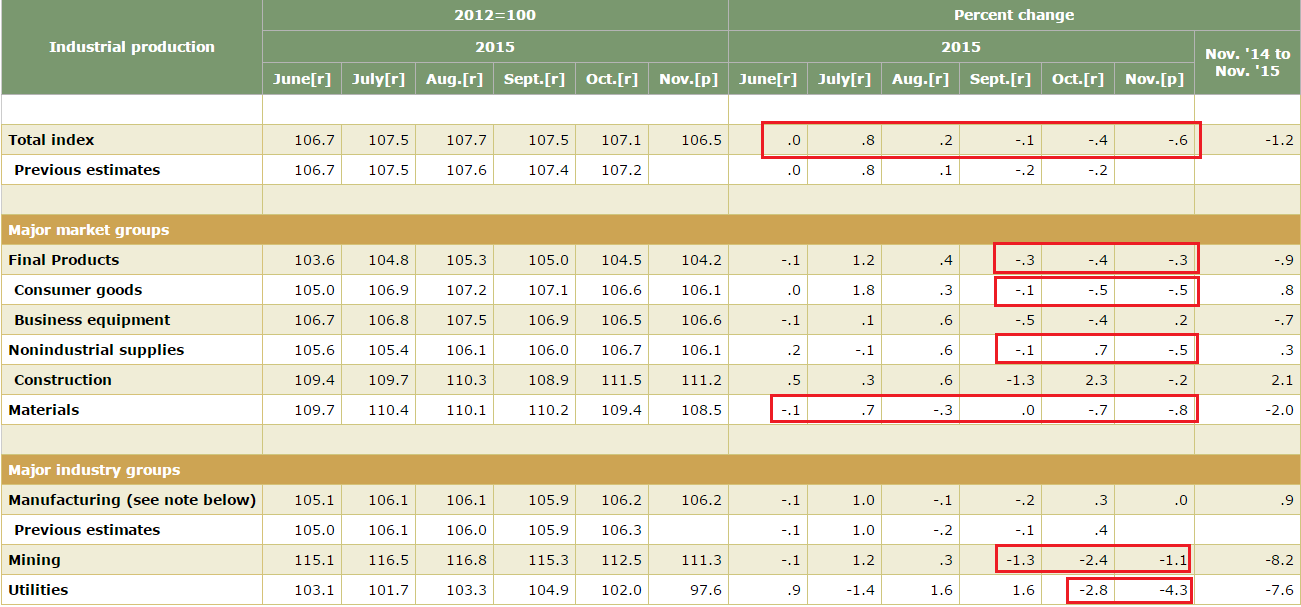

Industrial production decreased .6%. Three events are contributing to the weakness:

Manufacturing is “the weakest sector of the economy right now -- it’s getting hit by the strong dollar, lower energy prices, and now by the weather,” said Aneta Markowska, chief U.S. economist at Societe Generale in New York. Factory output “ultimately is 12 percent of GDP, so the question is what will happen to the other 88 percent. There, the news is still pretty good.”

The following table from the Fed report shows the breadth of the problem:

Final products, non-industrial supplies and materials were all anemic. Mining and now utilities are also fragile. Some market participants are describing the situation as an industrial recession:

From manufacturing behemoths like Caterpillar and Deere & Co to companies supplying the industrial sector the common theme in recent months has been that, thanks to a strong dollar and a collapse in commodity prices, tough times are back. Some are going so far as to declare the arrival of an industrial recession.

.....

At WW Grainger, an Illinois-based industrial supply company which sells everything from lightbulbs to electric motors and safety gear, sales in the US are down 5 per cent on last year with government purchases the only segment offering any growth. The company has been warning investors for months that it is facing a “tough industrial economy” which may last into 2016.

At Fastenal, which similarly relies on supplying the industrial sector, management has gone a step further. “The industrial environment is in a recession,” Fastenal’s chief financial officer told analysts on an October conference call.

.....

“It is a really tough time here now,” Tom Linebarger, Cummins’ CEO, said in a recent interview. “In many of our markets we are back to 2009 levels again, which is a story you are not really reading about.”

Housing continues growing. From the Census:

Privately-owned housing units authorized by building permits in November were at a seasonally adjusted annual rate of 1,289,000. This is 11.0 percent (±1.6%) above the revised October rate of 1,161,000 and is 19.5 percent (±2.0%) above the November 2014 estimate of 1,079,000.

.....

Privately-owned housing starts in November were at a seasonally adjusted annual rate of 1,173,000. This is 10.5 percent (±8.6%) above the revised October estimate of 1,062,000 and is 16.5 percent (±10.3%) above the November 2014 rate of 1,007,000.

It is difficult to see a protracted and deep recession so long as housing remains strong. It is possible the shallow industrial recession will continue to be a drag on growth.

The Atlanta Fed, Cleveland Fed and Moody’s high-frequency GDP model remain very close in their 4Q GDP predictions. The first two currently forecast growth of 1.9% while the last predicts growth of 1.8%. These readings are in line with the current slow growing CEI numbers cited above. The Atlanta Fed’s recession predictor shows a recession probability of 13.3%.

Economic Conclusion: this week’s numbers were positive. The LEIs point to continued growth. The CEIs confirm this trend, but also highlight the weakness caused by the industrial recession, which is confirmed by the weaker 4Q GDP predictions from the two Fed banks and Moody's. Best of all, housing sector news was positive.

The markets: the markets are expensive. The current and forward PE of the SPYs and QQQs are 22.65/22.75 and 17.19/19.54, respectively. 4th quarter revenue and earnings projections are not encouraging:

The estimated revenue decline for Q4 2015 is -3.1%. If this is the final revenue decline for the quarter, it will mark the first time the index has seen four consecutive quarters of year-over-year revenue declines since Q4 2008 through Q3 2009. Six sectors are expected to report year-over-year growth in revenues, led by the Telecom Services and Health Care sectors. Four sectors are expected to report a year-over year decline in revenues, led by the Energy and Materials sectors.

……

The estimated earnings decline for Q4 2015 is -4.5%. If this is the final earnings decline for the quarter, it will mark the first time the index has seen three consecutive quarters of year-over-year declines in earnings since Q1 2009 through Q3 2009. It will also mark the largest year-over-year decline in earnings since Q3 2009 (-15.5%). Four sectors are projected to report year-over-year growth in earnings, led by the Telecom Services and Financials sectors. Six sectors are projected to report a year-over-year decline in earnings, led by the Energy and Materials sectors.

As I noted last week, the weekly charts are slightly bearish. The daily charts are no better, starting with the SPYs:

The S&P 500 (SPYs) prices are below the 200 day EMA. Momentum and price strength are declining. And, the 212-214 area has provided solid resistance for the entire year.

The transports (IYT) are near a yearly low. The 200 day EMA has provided solid resistance since early August. Momentum is negative and declining and price strength is very weak.

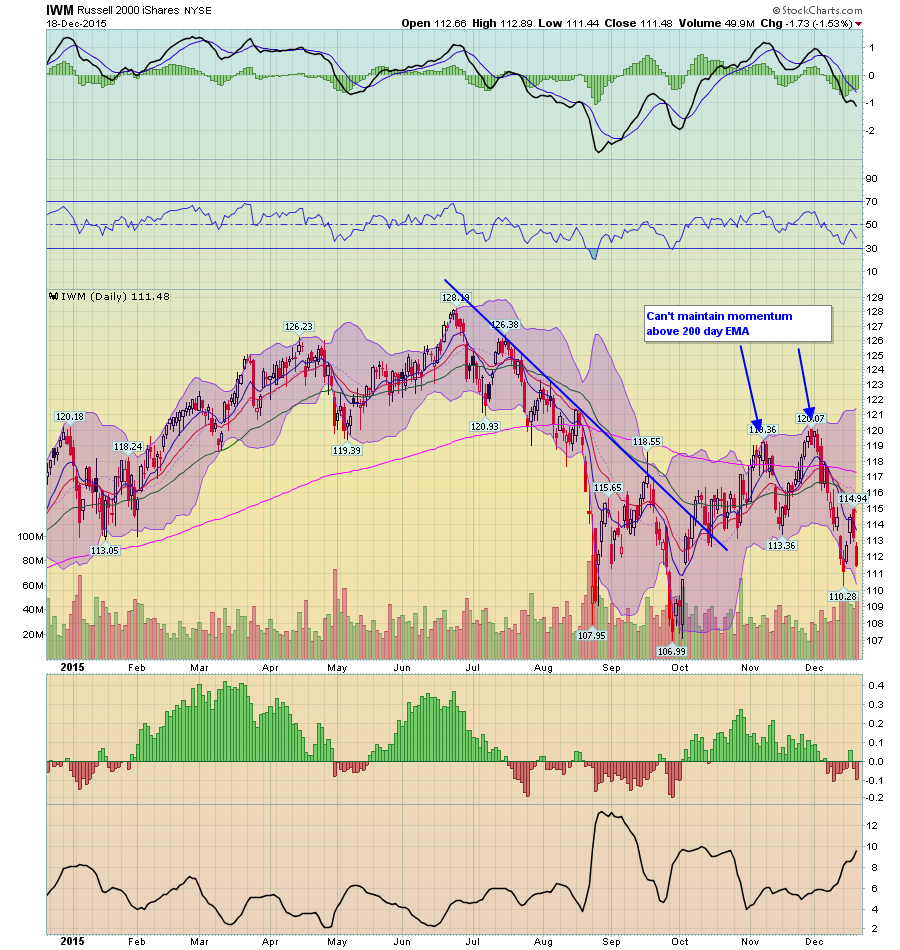

The Russell 2000 (IWMs) is below its 200 day EMA with declining momentum and price strength as well.

This only index with a positive technical outlook are the QQQs. But with the other three big average this technically weak, there is little hope for a sustained rally through previous highs for the QQQs, save any of the other indexes.

As we near year-end, we have more of the same: a market in desperate need of revenue growth isn’t getting any. Therefore, prices are weaker.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis