To no one’s surprise, the Fed raised rates 25 basis points this week, offering the following assessment of the economy:

Information received since the Federal Open Market Committee met in October suggests that economic activity has been expanding at a moderate pace. Household spending and business fixed investment have been increasing at solid rates in recent months, and the housing sector has improved further; however, net exports have been soft. A range of recent labor market indicators, including ongoing job gains and declining unemployment, shows further improvement and confirms that underutilization of labor resources has diminished appreciably since early this year. Inflation has continued to run below the Committee's 2 percent longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation remain low; some survey-based measures of longer-term inflation expectations have edged down.

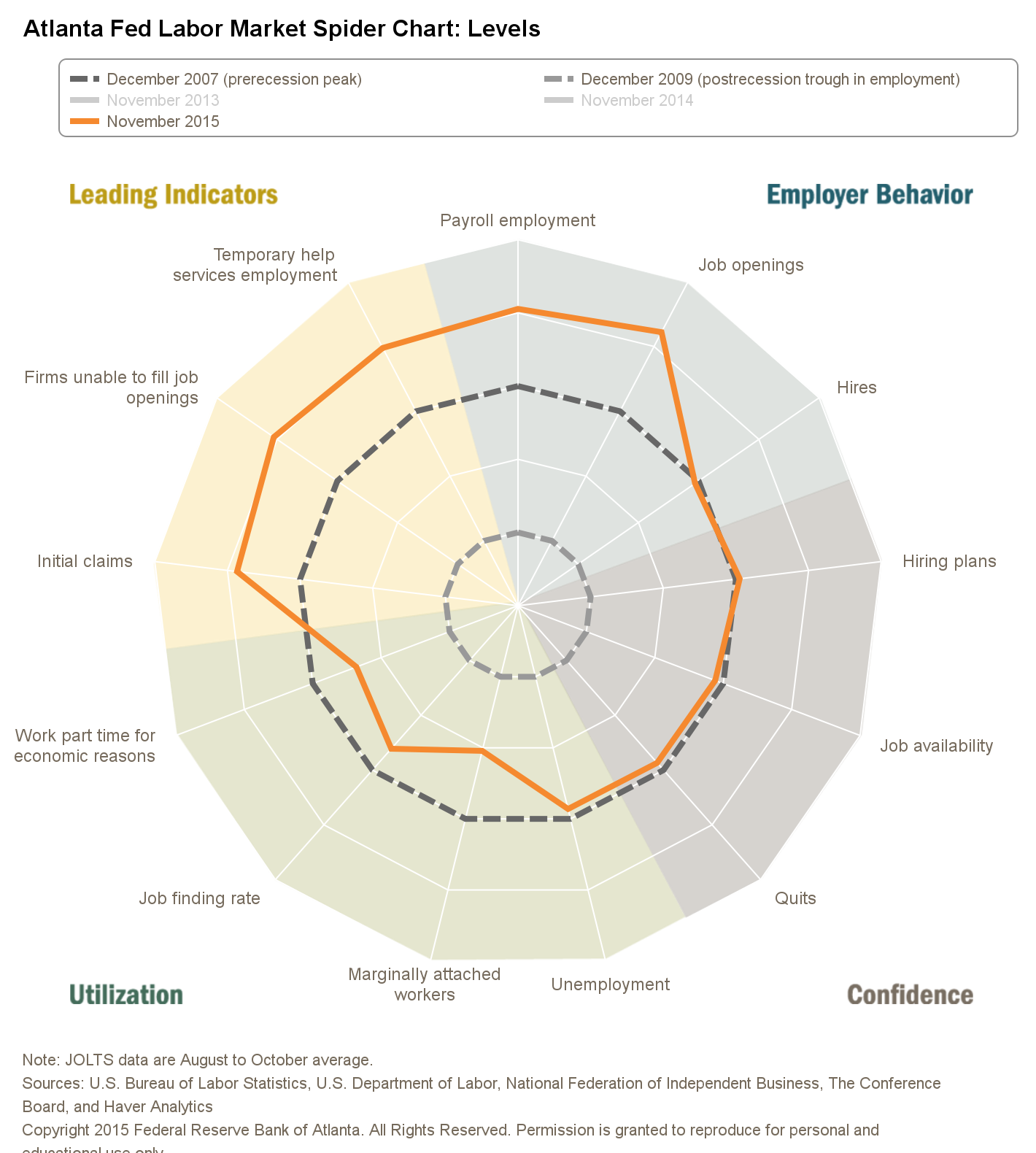

There is little debate about domestic demand (household spending, investment and housing); it remains strong. But there are moderately strong counter-arguments to several Fed assertions, beginning with employment. While under-employment has improved, utilization remains below its pre-recession peak:

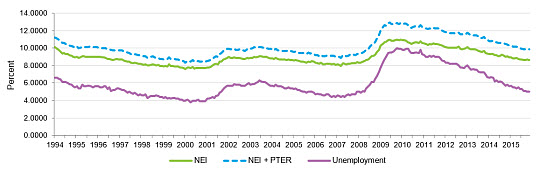

And the Hornstein-Kudlyak-Lange Non-Employment Index (NEI), provided by the Richmond Fed, is slightly over 8%, indicating a fairly high amount of labor slack:

Both measures are improving. But the higher level of under-utilization raises questions about the Fed’s timing. (But, see this from the KC Fed, indicating employees are more confident in their job hunting prospects).

The low level of inflation presents a second problem. The majority of the Fed Presidents argue that oil prices are the primary reason for weak prices. However, Fed President Evans and Brainard recently proposed an alternate, far more nuanced, thesis:

But inflation has been stubbornly low, even excluding energy prices. Over the 12 months ending in August, core PCE prices, which exclude the often volatile categories of food and energy, increased 1.3 percent, and the 12-month change in core prices has been around 1-1/4 to 1-1/2 percent since the beginning of 2013.

The persistence of the weakness in core price inflation deserves attention. For the post-recession period as a whole, low levels of resource utilization surely accounted for a substantial part of the weakness. But resource utilization has increased dramatically since 2009, and core price inflation has remained quite low.

A sizable decline in import prices over the past year has also contributed. As a result of the sharp increase in the dollar over the past year or so, prices for non-oil imports fell at an annual rate of a little over 4 percent in the first half of the year and look to decline a further 2 percent at an annual rate over the second half. Estimates suggest the dollar's rise will hold down core inflation between 1/4 and 1/2 percentage point this year, restraint that would wane if the dollar stabilized going forward.

However, recent weakness is not completely explained by import prices. Services prices excluding energy, which are generally relatively little affected by changes in the dollar, have also shown no sign of acceleration in recent years. Instead, inflation in this category has moved lower over the past year. In August, the 12-month change in non-energy services prices was 2 percent, 1/4 percentage point lower than the pace of increase from 2012 through the middle of 2014.

Brainard presents a complex inflation picture, attributing low inflation rates to a combination of resource underutilization, the strong dollar and broadly weaker commodity prices. Unlike the predominant Fed narrative, Brainard presents a far more nuanced picture. In addition, the Fed continues to state that prices will return to their preferred level of 2% within the next 24-36 months. But as Tim Duy points out, the Fed has a lousy track record on inflation forecasts (also see here).

The Fed is not the only central bank to miss inflation targets; the ECB and BOJ continue to struggle in their respective inflation predictions. But the fact that predictions have continually undershot actual inflation levels raises concerns that the Fed does not understand the current inflationary environment and is therefore far more prone to continue in their underestimation.

Additionally, some industrial sector participants are describing their macro environment as recessionary:

At WW Grainger, an Illinois-based industrial supply company which sells everything from lightbulbs to electric motors and safety gear, sales in the US are down 5 per cent on last year with government purchases the only segment offering any growth. The company has been warning investors for months that it is facing a “tough industrial economy” which may last into 2016.

At Fastenal, which similarly relies on supplying the industrial sector, management has gone a step further. “The industrial environment is in a recession,” Fastenal’s chief financial officer told analysts on an October conference call.

A rate increase will increase the dollar’s value, exacerbating the downturn.

The combination of weak labor utilization, weak inflation and an already challenging environment for the industrial sector (that will be made worse by the resulting stronger dollar) provide a strong counter-argument to timing of this rate increase.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis