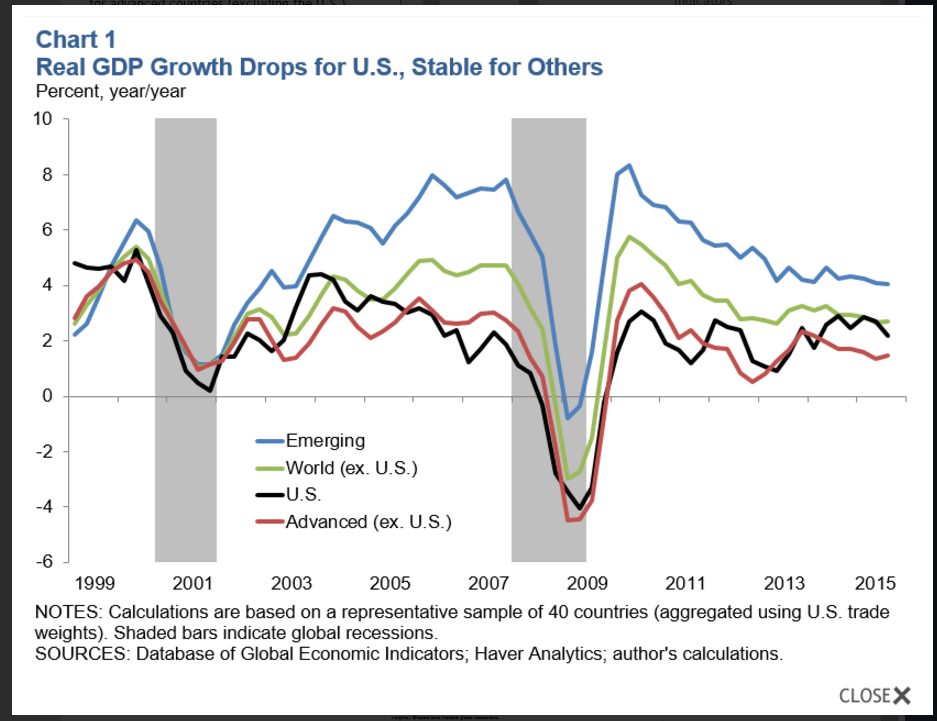

The Dallas Fed published its international economic review this week, which contained the following graph of global economic growth:

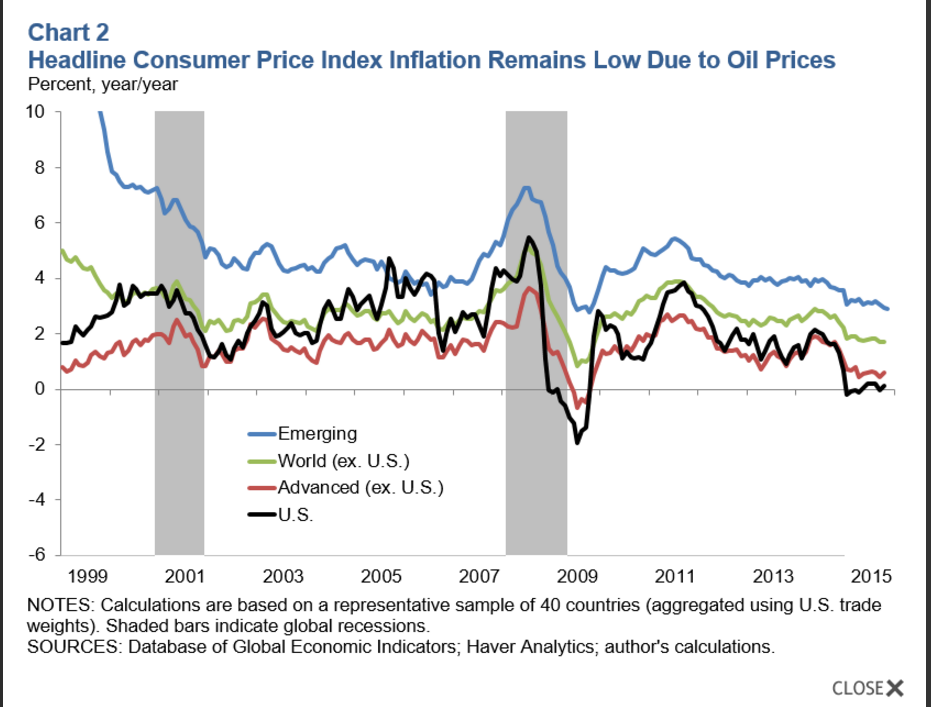

Since 2013, emerging, world and advanced economies’ GDP growth continued to move slightly lower. The only economy to gain GDP traction was the US. The report also contained a graph of global inflation:

Here, all major regions are experiencing a downturn in prices, but this time since 2011. There is little new in this information; we’ve known for some time that overall, the global economy is somewhat weaker over the last 12-24 months. But as we near year end, these two charts provide and important reminder that the global situation is delicate.

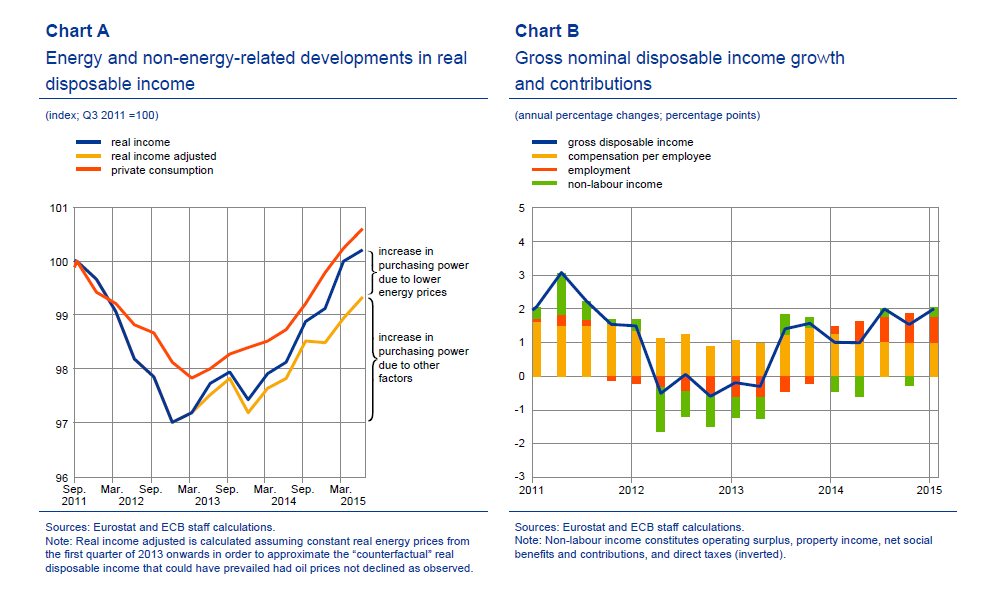

EU news continues to show a growing region. The latest ECB report explained that wages were increasing due to lower fuel prices and improving employment:

The left graph shows that lower energy prices are responsible for ~1/3 of the improved consumer buying power. The right graph shows that employment growth and compensation are about equally responsible for the remaining increase. The recently reported employment increase should add to wage gains:

The number of persons employed increased by 0.3% in the euro area (EA19) and by 0.4% in the EU28 in the third quarter of 2015 compared with the previous quarter, according to national accounts estimates published by Eurostat, the statistical office of the European Union. In the second quarter of 2015, employment increased by 0.4% in the euro area and by 0.3% in the EU28. These figures are seasonally adjusted.

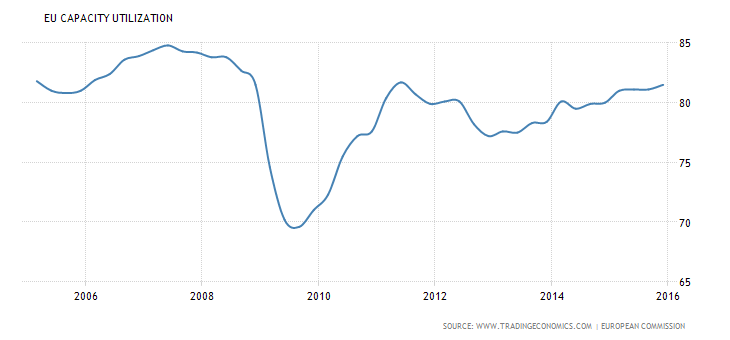

The industrial sector remains strong: industrial production increased 1.9% Y/Y while Markit reported the highest flash manufacturing number (54.4) in 20 months. Services were also healthy with a 53.9 reading. There are still problems, however. Total inflation increased a mere .2% Y/Y. The core rate was somewhat better at .9%, but that figure is still low. And in a speech earlier this week, ECB head Draghi highlighted the EU region’s anemic investment growth:

In determining potential growth, the role of investment is crucial. It increases at once today's demand and tomorrow's supply. In the euro area, however, the recovery has thus far mainly concerned consumption and only to a lesser degree involved investment, which is still 15% lower than its pre-crisis levels. This weakness is, moreover, common to other advanced economies as well.

In the euro area, investment is being held back primarily by three factors: weak demand, the debt overhang, which was building up already in the period preceding the crisis, and the private sector's shaky confidence in the growth prospects of our economies.

Although loans are rising, capacity utilization remains weak, which will drag investment down in the short term:

But despite investment and capacity weakness, the overall tenor of EU news remains positive.

Japanese news continues to be mixed. Markit reported a flash headline number of 52.5 The report contained the following observation:

“Operating conditions at Japanese manufacturers continued to improve at a solid rate in the final month of 2015. Despite easing, the rate of expansion in production was robust overall. Meanwhile, growth in total new work picked up to the second-highest since October last year. Supporting this was a rise in international demand as new export orders increased further.

But the recently released industrial production numbers showed a decrease of 1.4%:

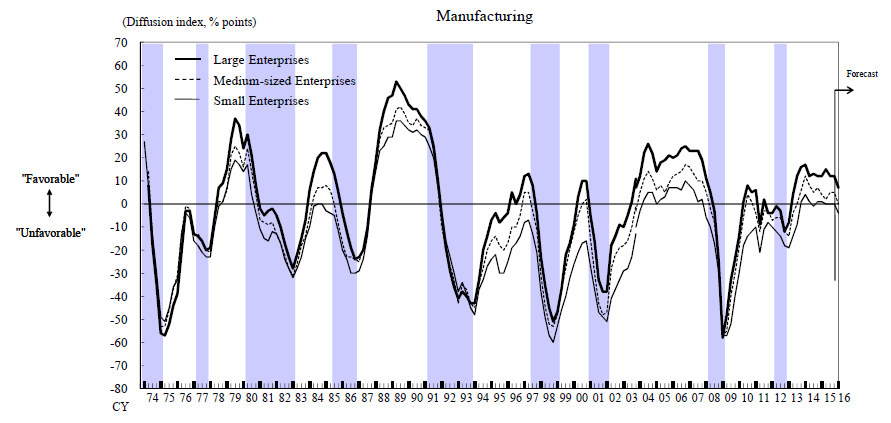

And the light blue line shows high inventory levels that will suppress production going forward. The bifurcated nature of the industrial expansion explains the difference:

The above graph from the latest Tankan survey indicates that while large manufacturers view current conditions favorably, mid-size and small size manufacturers do not. In fact, small companies have had an unfavorable impression of the Japanese economy since the Great Recession. And mid-size companies’ outlook is quickly turning negative.

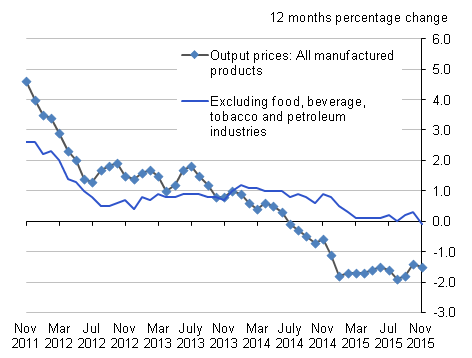

UK news was positive. Inflation remains subdued: PPI dropped 1.5% Y/Y while CPI increased a modest .1% Y/Y:

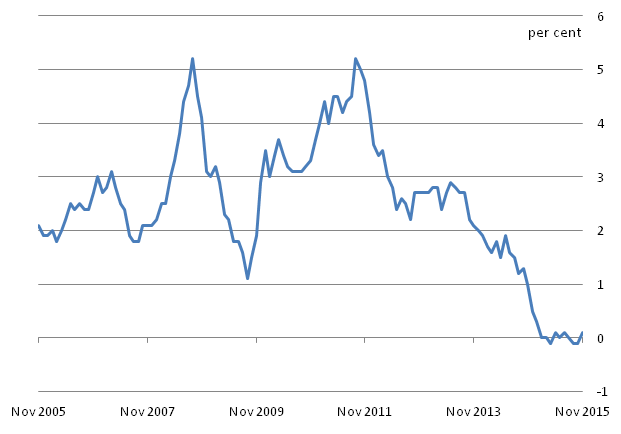

Unemployment ticked lower, dropping .1% to 5.2%, while retail sales increased 5% in volume Y/Y. The three month rolling average continues to be very strong:

Both figures provide the Bank of England with a large amount of room to maneuver. In fact, it’s distinctly possible they’ll let the strong position of the Sterling do most of their work for them right now.

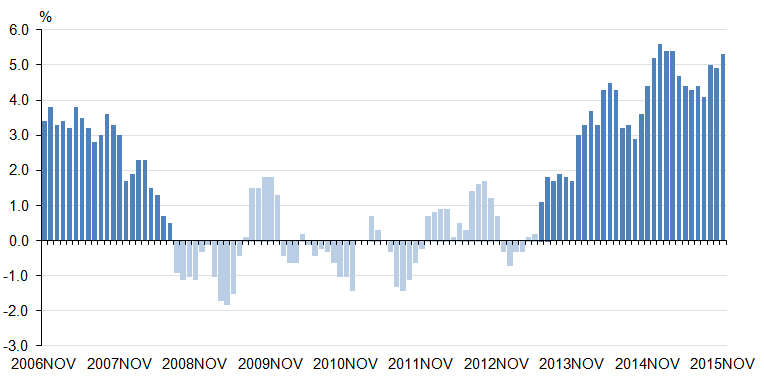

The RBA released their latest meeting minutes, which contained the following assessment of the Australian economy:

Members noted that the September quarter national accounts would be released the day after the meeting. GDP growth looked to have picked up in the quarter, but was likely to have remained below average over the year. Resource exports and dwelling investment were expected to have made positive contributions to growth in the September quarter, following declines in the June quarter. Based on partial indicators, household consumption growth was likely to have increased in the September quarter but business investment was expected to have declined.

Little in the Australian story has changed over the last year. The economy, which relied almost exclusively on raw material exports for growth, is slowly changing to a more diverse economy. But this chart from the latest RBA Chart Pack shows the depth of the problem:

From 1992 to ~2014, non-mining investment doubled while mining investment rose 16x. The capital build-out overshot demand, contributing to the current commodity price rout. But companies are still more concerned with protecting market share, so they aren’t cutting production yet. This situation has led the Australian government to lower their overall growth projections for budgetary purposes:

Australia’s government has downgraded its growth forecasts for the second time this year, warning on Tuesday that its budget deficit will grow because of a sharp drop in the value of commodity exports.

The economy is now expected to grow by 2.5 per cent in the year to the end of June, compared with a 2.75 per cent forecast in the budget in May. The budget deficit is forecast at A$37.4bn ($27.1bn) in 2015-16, an increase of A$2.3bn on the previous projection.

Finally, news from China added to concern for the country. First, the Beige Book (which is produced by a private company) highlighted continuing industrial weakness.

China’s economic conditions deteriorated across the board in the fourth quarter, according to a private survey from a New York-based research group that contrasted with recent official indicators that signaled some stabilization in the country’s slowdown.

National sales revenue, volumes, output, prices, profits, hiring, borrowing, and capital expenditure were all weaker than the prior three months, according to the fourth-quarter China Beige Book, published by CBB International. The indicator is modeled on the survey compiled by the Federal Reserve on the U.S. economy, and was first published in 2012.

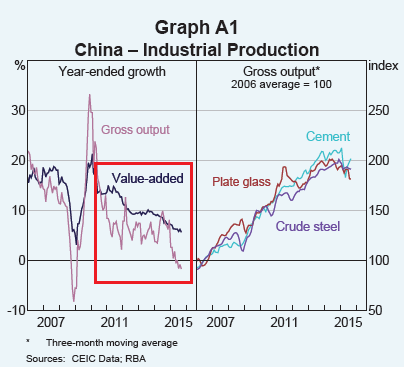

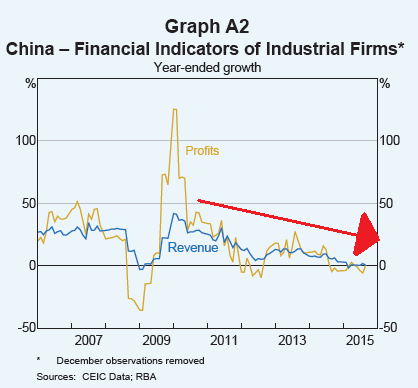

A report issued by the RBA confirms this trend. The report contained the following two graphs:

The above chart shows that gross industrial output is now negative while total value added by the industrial sector continues to decline.

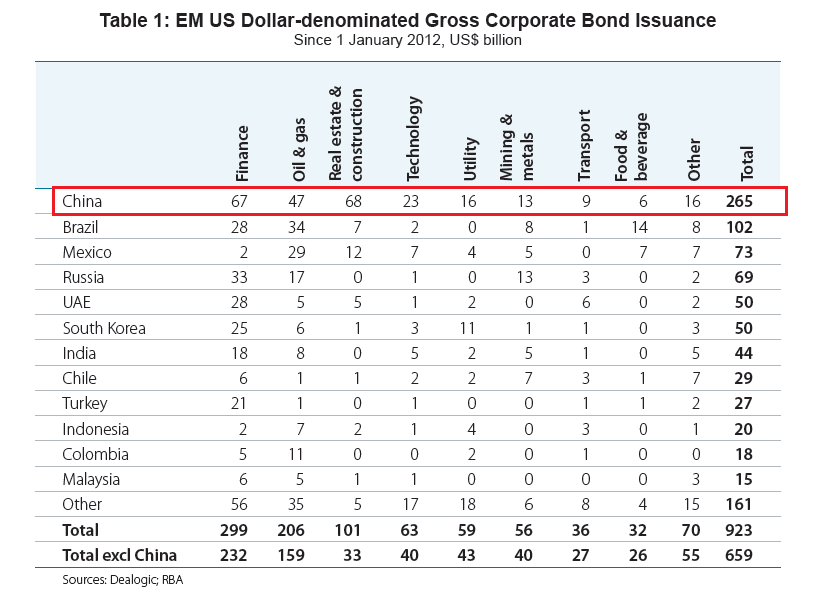

The above chart shows that industrial companies’ revenue and profits are weak as well. Another report from the RBA shows that Chinese companies are by far the largest issuers for debt, to the tune of $265 billion dollars:

Further complicating this situation is that China is now a net capital exporter, meaning some these companies may be scrambling for cash in the next 12-24 months.

As we go into year end, the world economic situation is tenuous. The US, UK and EU are doing fairly well, but Japan and China are weakening. And while Australia is growing, it's clear the Chinese slowdown is hurting. Overall, as noted by the Dallas Fed, the global economic environment is fragile.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis