|

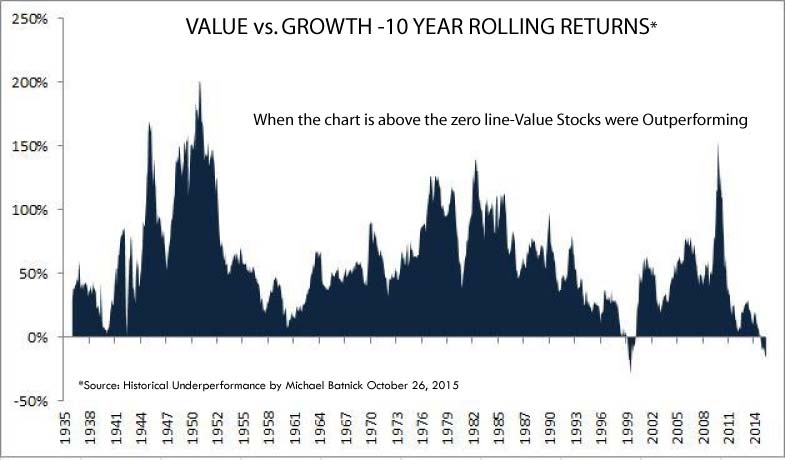

The biggest stock market story for 2015 is divergence of returns. The year 2015 is looking a lot like 1999 where performance was driven by a narrow group of stocks while most stocks did poorly. In 1999, technology stocks seemed to suck money from every other part of the stock market in what in hindsight was clearly a bubble. The aftermath was brutal. The 15 technology companies with the largest market capitalization (cap) in 2000 lost 60% of their combined market value, or about $1.3 trillion. Only Microsoft has a market cap higher today than in 2000. What most people forget however is the bursting of the tech bubble coincided with the bottoming of value and small-cap stocks. Berkshire Hathaway, PepsiCo, Anheuser Busch, Southern Co., Wells Fargo, Diageo, and small-caps all started multi-year advances in March 2000. In the past couple of months you may have heard the term FANG stocks. FANG refers to the stocks Facebook, Amazon, Netflix and Google. These four stocks along with a few others are mostly responsible for the S&P 500 remaining in positive territory in 2015. The year-to-date returns for these stocks are: Facebook, 34%, Amazon, 112%, Netflix, 143%, and Google, 43%. Because the S&P 500 is a market cap index these massive companies have an outsized influence on the index's returns. As we have highlighted this year the world economy is limping along and U.S. earnings seem to have peaked. As a result investors have flocked to these growth companies and ignored most everything else. Of the four stocks we own Google whose valuation we still consider reasonable, albeit full. The other three stocks have stratospheric valuations, and while great companies, will probably disappoint investors over time. The divergence is best seen in the performance of the S&P 500 Value, down -3.5%, versus the S&P 500 Growth, up +5.4%. This performance spread of 8.9% is huge and is reminiscent of what occurred in 1999. Moreover, this performance trend has been going on for several years to the point where the outperformance of growth stocks is at an extreme. OVER THE LONG RUN - BETTER VALUES HAVE OUTPERFORMED*

The above chart shows the Performance of Value stocks relative to Growth over ten - year rolling periods. When the chart is above the zero line, Value stocks were outperforming. As we would expect value consistently outperforms most of the time. However, today we are at an extreme level of underperformance for value relative to growth, a situation similar to 1999. The silver lining is that despite a challenging macro environment for stocks many companies have already seen large declines and are attractive. We are more active in our stock research currently than we've been in a long time and expect to gradually add high-quality value stocks to the portfolios. |