SPY and NDX are near support and breadth is either washed out or close to being so. Volatility experienced an extreme spike; mean reversion usually follows. Seasonality, especially with December OpEx up next, is very bullish. All things being equal, risk/reward should be skewed higher.

The wild card is oil: equity markets are being driven lower by falling oil prices and their impact on high-yield. That could pressure markets further. Adding to the drama is the Fed is expected to initiate the first rate hike since 2006 this week.

* * *

For the week, SPY and NDX lost 3.6%, about the same as the high-yield ETF, HYG. Oil was the biggest loser, dropping 11%.

The week's biggest move belongs to VIX, which gained an astounding 63%.

What's going on?

First, recall that SPX has seen an average drawdown in December of 3.7% since 1928. Since the December 1 close, SPY is now down 4.2%. So what has happened is, in some ways, not so unusual.

Second, while December is typically very strong, the beginning of the month is not. The positive performance in December typically starts in the second half (meaning the week that's upcoming). Again, so far nothing extraordinarily unusual.

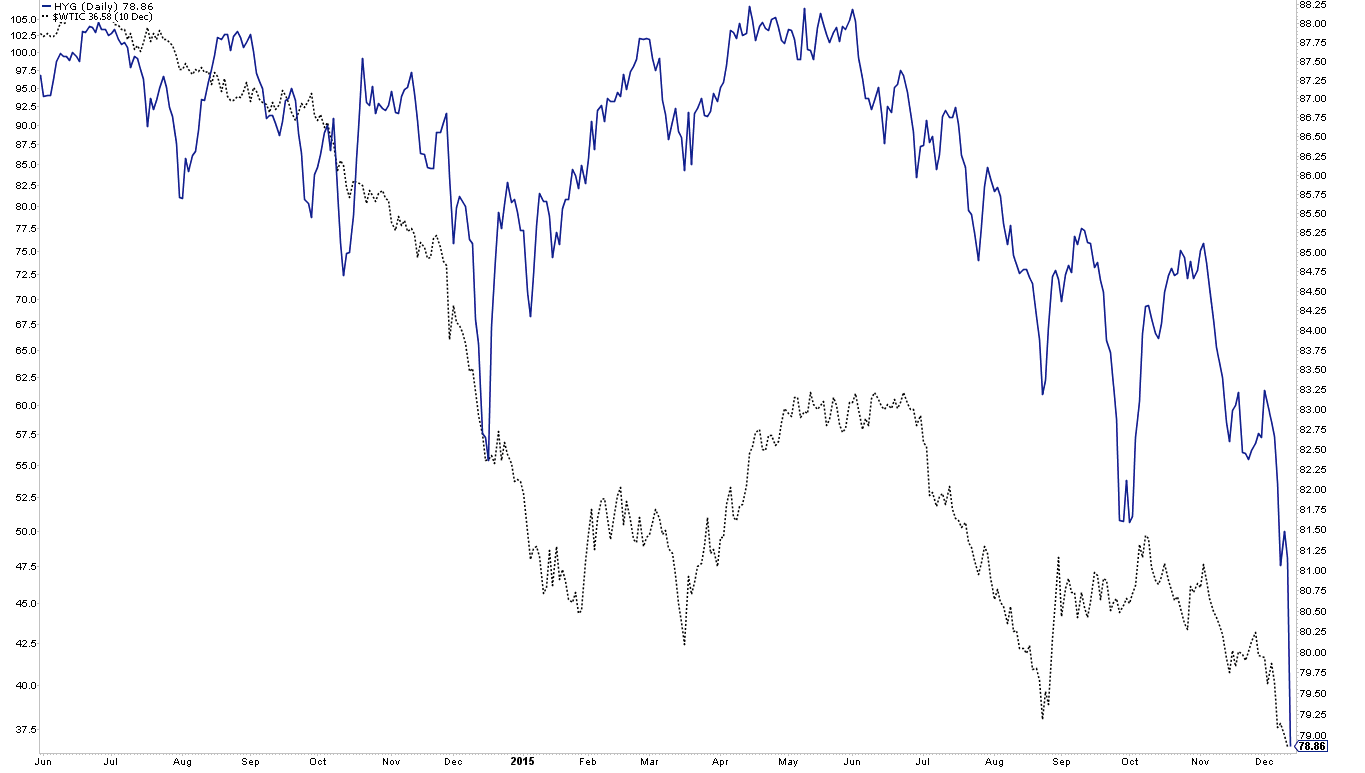

Third, and most importantly, the market is being driven by the collapse in oil. About 15% of the high-yield market is exposed to energy; so, falling oil (gray line) is pushing high-yield prices lower (blue line). And lower high-yield price (wider spreads) is creating concern that a larger credit crisis is unfolding, foreshadowing a recession.