This was a very light week of news. Only the BOE had a policy meeting. And other major countries released very few economic numbers.

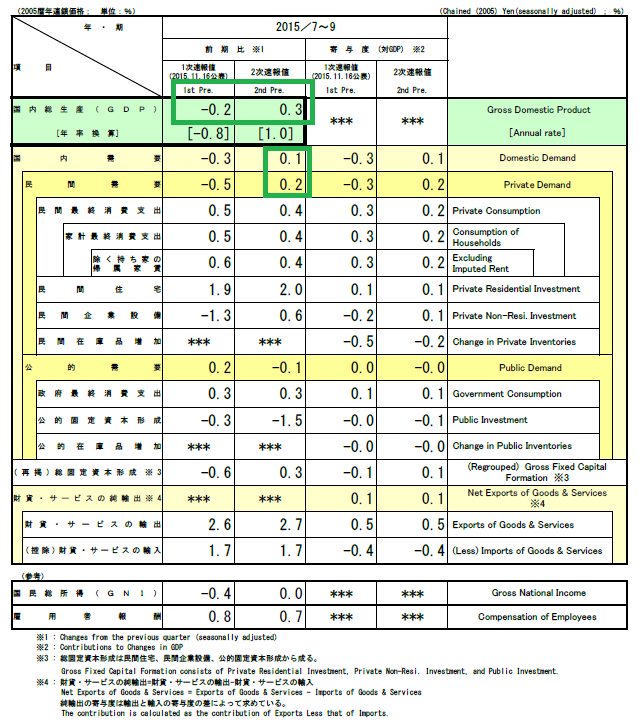

Japanese news was surprisingly strong, starting with an upward revision of 3Q GDP to an annual rate of 1%. This revision means Japan didn’t experience a technical recession. As this table from the report shows, personal consumption expenditures were largely responsible for the positive results:

Unlike other developed countries, Japanese GDP figures are notoriously volatile. Thanks to strong results from job offers and inventory improvements, the LEIs increased 1.3%. Durable goods shipments and industrial production increases were largely responsible for the CEIs rising 2 points. However both composite indicators are still more or less moving sideways for the last year:

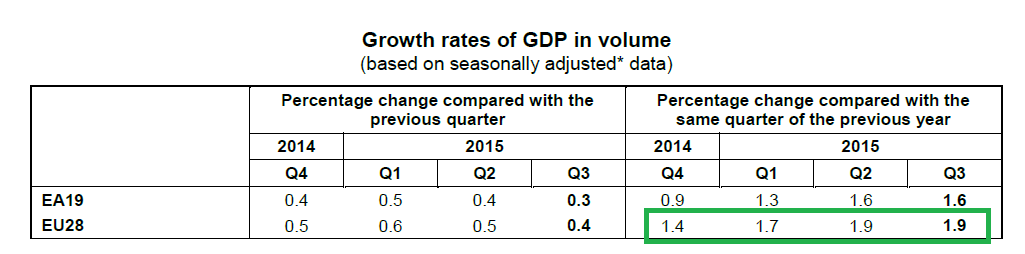

The only news from the euro area was GDP, which increased .4% Q/Q and 1.9% Y/Y. While weak, Y/Y GDP growth is increasing:

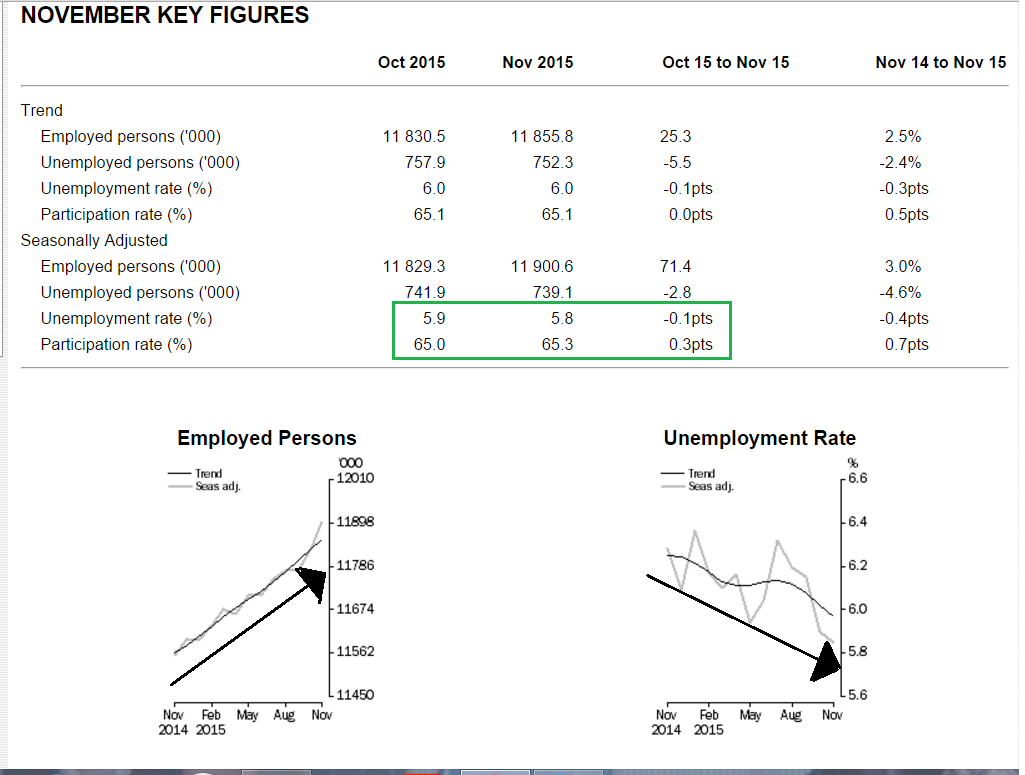

News from Australia was positive. First off, employment increased, the unemployment rate dropped .1% to 5.8% and the participation rate rose .3%. All three are shown in these graphs and tables from the report:

Next, the Australian Industry Group (AIG) released their monthly manufacturing, services and construction reports. The headline manufacturing number increased 2.3 to 52.5, marking the fifth consecutive months of expansion. 7/8 sub-indexes expanded and 5/8 sectors are growing. However, services contracted for a second month with a 48.2 reading. All the sub-indexes contracted while only 4/9 sectors expanded. Finally, construction expanded for a fourth consecutive month, but only because the apartment sector is growing strongly; all other sectors are contracting.

The BOE maintained rates this week, offering the following assessment of the UK economy:

Twelve-month CPI inflation remained at -0.1% in October, a little more than 2 percentage points below the inflation target. Inflation is expected to have been slightly positive in November, and is projected to rise further as some of the large falls in energy and food prices at the turn of last year drop out of the annual comparison. Nevertheless, core inflation remains subdued, and CPI inflation is expected to stay below 1% until the second half of next year.

The outlook for inflation reflects the balance between persistent drags from factors such as sterling and world export prices and prospective further increases in domestic cost growth. The MPC’s objective is to return inflation to target sustainably; that is, without an overshoot once persistent disinflationary forces ultimately wane. Given these considerations, the MPC intends to set monetary policy to ensure that growth is sufficient to absorb remaining spare capacity in a manner that returns inflation to the target in around two years and keeps it there in the absence of further shocks.

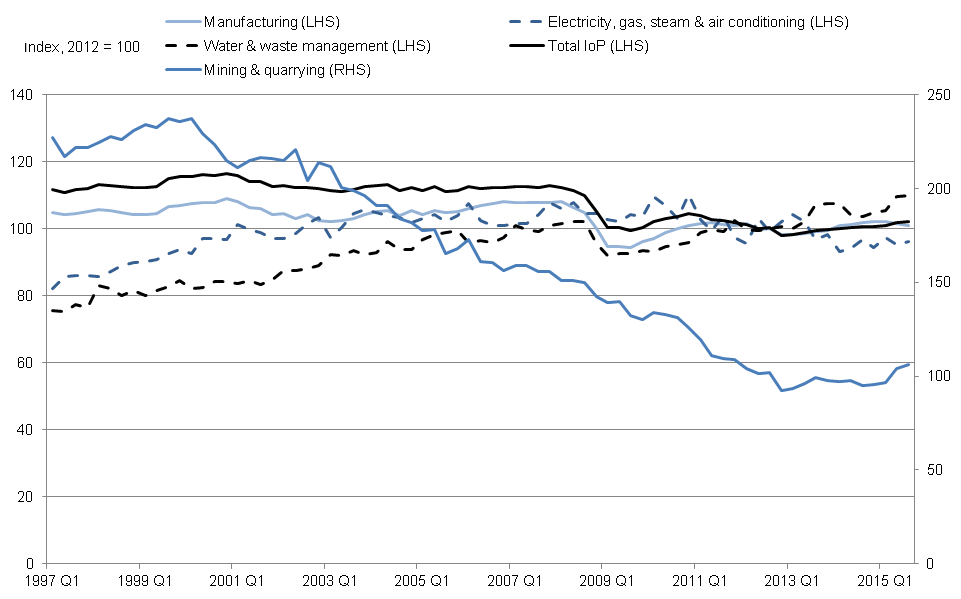

Unlike the US, the BOE has a far more nuanced view of inflation, which I believe to be correct. In addition, overall production increased 1.7% Y/Y while manufacturing was down .1%. However, as shown in this chart from the report, the overall condition of manufacturing and production is still below pre-recession levels:

There was insufficient information released this week to draw any type of conclusion. The data is being offered in the name of completeness. Next week promises to be far more substantial.