In a new quarterly letter to GMO's institutional clients, co-head of asset allocation Ben Inker examines whether emerging-market equities might be a "value trap," and if U.S. equities are "deserving of trading at a premium P/E to the rest of the world" ("Just How Bad Is Emerging, and How Good Is the U.S.?").

In part two of the letter, chief investment strategist Jeremy Grantham provides "a list of propositions that are widely accepted by an educated business audience ... but totally wrong. ...When you have run through this list you may be a little more aware of how dangerous our wishful thinking can be in investing" ("Give Me Only Good News!").

Just How Bad Is Emerging, and How Good Is the U.S.?

Ben Inker

The past year was a lousy one for investors in emerging markets. The MSCI Emerging Equity index fell 19.3% in the 12 months ended September 30, 2015, the J.P. Morgan ELMI Plus index of emerging currencies was down 12.5%, and the J.P. Morgan EMBI Global index of emerging sovereign hard currency debt was down 2%. By comparison, the S&P 500 was down 0.6%, the Russell 2000 up 1.3%, MSCI EAFE down 8.7%, and the Barclays U.S. Aggregate Bond index was up 2.9%. It would seem to qualify as a nightmare year for emerging, but those of us old enough to have been paying attention back in the 1990s can remember what a true emerging nightmare is. In the year to September 30, 1998, MSCI Emerging was down 48% and the J.P. Morgan EMBI Global down 24%, against a rise of 9% for the S&P 500 and 11.5% for the Barclays (then Lehman) U.S. Aggregate Bond index. So those past 12 months could have been worse. But considering that we thought that emerging assets were some of the cheapest around a year ago, Lord knows it could have been better.

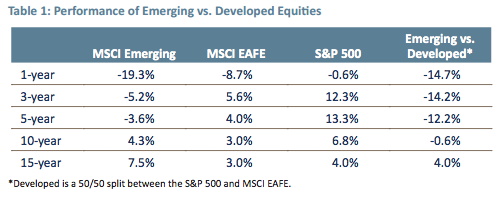

And this wasn’t the first bad year for emerging, or the second, or the third. Table 1 shows the 1-, 3-, 5-, 10-, and 15-year performance for emerging versus EAFE and the S&P 500, and it is abundantly clear that things have been quite bad for half a decade now.

Losing to the rest of the world by 14.7% in a year is bad enough, but losing by 12.2% per year for five years is a lot worse. A dollar invested in MSCI Emerging has turned into $0.83 over that period, while a dollar invested in MSCI EAFE has grown to $1.21 and a dollar in the S&P 500 to $1.87.

Is it any wonder investors are questioning why they allocate to emerging markets in the first place? Even going beyond the woes of emerging, we are starting to hear some investors asking whether holding non-U.S. stocks is at all necessary. As market historians we can say that the timing of such sentiments tends to be bad – no one seems to ever decide to give up on an asset class after it has just had good performance, and the last burst of “why bother with non-U.S. stocks” occurred just before the top for the S&P 500 in 2000. But just complaining that investors got it wrong last time they voiced these sentiments does not qualify as thoughtful analysis. Relative to what we were thinking five years ago, emerging equities have done surprisingly badly, and the U.S. equity market has done surprisingly well. Was that the luck of the draw, which has no bearing on future returns? Was it a temporary phenomenon that will soon reverse? Or does it tell us something important about emerging being a value trap and/or the U.S. being extraordinary that we need to take into account in our forecasting of the future?

The short answer to these questions is that while emerging markets “deserved” some of their bad luck over the last several years and the outperformance of the U.S. has made some sense, we do not believe that emerging is a value trap, nor do we believe that the U.S. has proved itself particularly extraordinary. There are some reasonable models for valuing the U.S. stock market that make it noticeably more attractive than our overall seven-year forecast estimate of -0.6% real, but others that make it look meaningfully worse. The different valuation models for emerging are actually saying surprisingly similar things today with regard to expected returns, and one of the major headwinds for emerging over the past five years, currencies, may well soon turn into a tailwind. None of this is to say that emerging doesn’t have its share of problems or that the U.S. may not pull a rabbit out of its hat, but we do not currently see any reason to assume the worst from emerging or the best for the U.S.

Is EM a value trap?

What would it mean for emerging equities to be a value trap? If we are valuing these equities on a normalized earnings basis, which GMO’s forecasts effectively do, two possible reasons emerging would be a value trap is if “true” normalized earnings are a lot lower than our models make them out to be, or if the return to the stocks is not commensurate with an assumption that outside shareholders get the benefit of corporate earnings. There is also a third potential problem that is a little harder to quantify, but still important. If there were some sort of malign interaction between the equities and currencies such that we should expect foreign currencies to fall against the dollar with no corresponding increase in local real returns, we could find emerging equities winding up a value trap from a U.S. dollar perspective even if not from a local one. Because any of these problems could trip us up, let’s take them in turn.

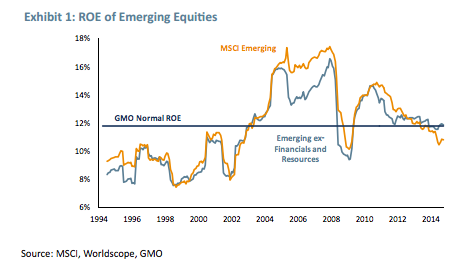

We use a variety of ways to come up with the normalized earnings power for stocks, but for this purpose, let’s focus on ROE and book value as the measure. We generally assume that book value grows slowly over time while ROEs are volatile and bounce around with the state of the business cycle. This means that to calculate normalized earnings we need to come up with a normal ROE. This is not a trivial exercise, but here is how we have done it in this case. Exhibit 1 shows the ROE for emerging markets and emerging markets ex-financials and resources over time, along with our assumed normal ROE.

We can see the impact of the resource companies and financials on the profitability of emerging stocks, but it isn’t overwhelming. We prefer excluding resource companies for analyzing the profitability of emerging today because not only are they quite unprofitable now, but from 2005-2012 their profitability was significantly better than other stocks and, hence, dragged up the averages. As a result, we prefer to build a separate forecast for the resource companies taking into account the fact that their profits are likely to be much lower than they averaged over the last decade. So the profitability line we are more interested in is for the group excluding resources, and on that basis current profitability looks slightly better than normal.1 Now, the actual way we come up with our profit normalization uses book and other measures to help us estimate economic capital, for it is really return on economic capital that should be mean reverting. Table 2 shows the different estimates for return on economic capital that come from the four models we use to proxy for that unobservable quantity.

The four estimates are actually quite close to each other for the groups excluding financials and resources, which gives us some comfort that we are not doing anything too aggressive with our normalization of earnings. The figures would all be far friendlier if we included the financials and resources, but our best guess is that doing so would be too friendly.

We therefore estimate that emerging normalized profitability is a little better than current levels on an overall basis and a good bit worse excluding financials and resource companies. It is hard to be supremely confident in this, but for true normalized earnings to be significantly lower than we are estimating, it would mean that today’s environment is currently a very good one for profitability compared to true “normal.” That seems out of keeping with the general state of most emerging economies today, and none of our proxies for profitability suggests that it is true.

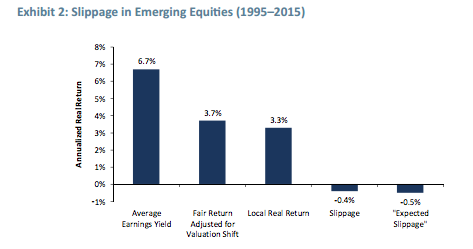

But profits only tell part of the story. We know that in parts of the emerging world, earnings yields overstate the likely long-term returns to outside shareholders. In the case of Gazprom, for example, corporate investment decisions are made with a lot of concern for the Russian government’s view of its strategic priorities and much less worry about the return on capital employed. If emerging equities are generally characterized as acting like Gazprom, we would see returns to emerging that are systematically well below what one would expect from the stated earnings of the companies. So let’s look at the results. We’ve got decent financial data on emerging companies going back 20 years, so Exhibit 2 shows what has happened.

This exhibit takes a little explaining. The average earnings yield over the 20 years has been 6.7%. So, we might have expected real returns to be 6.7% over the period. But the earnings yield of emerging has risen from 4.8% to 7.6% since 1995. A rising earnings yield equates to a falling price, and the effect of that change has been to suppress returns by 3% per year. That means a fair return to emerging would have been 3.7% real, and the actual return has been 3.3% real. The 0.4% gap is something we refer to as “slippage” and it says that emerging stocks have indeed done a bit worse than one would expect given their earnings yield. However, given the long-term data for equities around the world, we assume 0.5%/year slippage in our forecasts, so emerging equities have been almost exactly in line with what we expected from them. The one fly in the ointment for this analysis, though, is the fact that these returns are local real returns, so there remains the possibility that currencies could have led to further problems for emerging equities.

Is it just a currency thing?

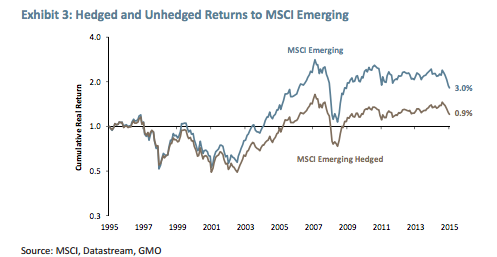

Falling currencies have indeed been a significant driver of losses in emerging equities over the past few years. In the 12 months ending September 30, for example, the local return to emerging stocks was -7.1% while the loss from the currency movements cost 13.1%. This might tempt one to think about currency hedging their holdings in emerging markets, but this turns out to be a bad idea historically. In fact, it seems to be a spectacularly bad idea, as we can see in Exhibit 3.

This is a truly striking chart. Since 1995, the rather anemic returns of +3.0% real in U.S. dollars for emerging equities turn into a truly depressing +0.9% real. So much for the idea of curency hedging! Actually, this speaks to a broader question. If the return to holding the currencies has been so close to that of holding the equities, is it possible that just owning emerging currencies is the right way to play emerging markets?

In order to answer this question, we need to dig into the sources of return for emerging currencies. Currencies are pretty simple assets, so the breakdown is straightforward. The two sources of returns to a currency are the real interest rate earned and the change in the real exchange rate. While you could look at both in nominal instead of inflation-adjusted terms, for countries whose inflation rates have differed considerably from the U.S., that could easily give quite misleading answers. Exhibit 4 shows the returns to the J.P. ELMI Plus Emerging Currency index broken down into the real interest rate and FX components.

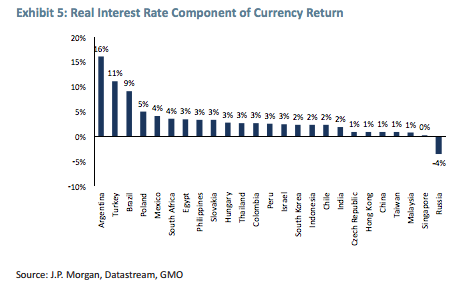

We can immediately see that a little more than 100% of the return has come from real interest rates. The changes to the real exchange rates have been a mild drag, although all of that drag has come quite recently. This is actually supportive of the idea that there is a sustainable return here, because it would be implausible to expect exchange rates to appreciate forever, but risky countries could easily have high real interest rates.2 The place where trouble comes in is when we look on a country by country basis to see what those real interest rates were. Exhibit 5 shows the real interest rate component of the currency return by country for the emerging universe.

The problem here is that the countries at the top of the list have had implausibly high real interest rates. I don’t mean by this that the data is wrong, but suggest a somewhat subtler issue. While these are likely correct figures for the ex-post real offshore cash rates in these countries, for Argentina and Turkey, and probably for Brazil, they are likely to have been a lot higher than the ex-ante expected real offshore cash rates. All three countries went through fairly recent periods of hyperinflation, and, from the looks of it, market participants were pleasantly surprised by how quickly their governments got inflation under control. Certainly investors did demand high expected real interest rates in these countries to compensate them for the risks of inflation, but double-digit real returns do not pass the sniff test. This means that some of the return to the ELMI came from a source you’d be very nervous about counting on going forward – a large positive surprise in inflation relative to expectations. There is one country on the other side of things where you’d have to believe that inflation was a negative surprise, however. Real rates in Russia have been -4% on average since 1995, and it is almost impossible to imagine that investors actually expected to be losing money after inflation on their Russian investments and chose to make those investments anyway.

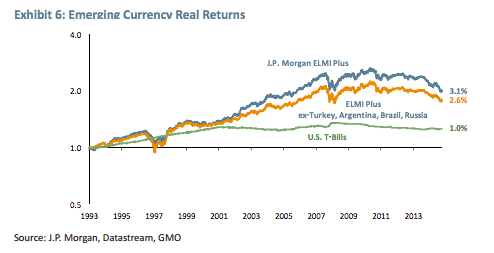

If we recalculate the returns to the index excluding Argentina, Turkey, Brazil, and Russia, the resulting returns are noticeably lower than for the whole index, which we can see in Exhibit 6.

But it still leaves a fairly large return in excess of U.S. cash rates. Again, this probably shouldn’t come as a real shock. Many emerging currencies are risky, with countries needing to attract foreign capital despite historical inflation problems. It would be natural to think that investors in emerging currencies should demand a risk premium to invest, and it looks like they have gotten one. Once we adjust for the valuation drop in emerging equities over the last 20 years, however, there still seems to be a decent equity risk premium remaining.

But what about the possibility of a nasty interaction between the currencies and stocks? In essence, this would require that the currencies fall in real terms and fail to recover. This certainly is possible, but the data from the last 20 years doesn’t suggest it has been happening so far. Exhibit 7 shows the valuation of an index of emerging currencies since 1995 in terms of standard deviations against the U.S. dollar.3 As of September 30, the currencies were about 1.3 standard deviations cheap.

But what about the possibility of a nasty interaction between the currencies and stocks? In essence, this would require that the currencies fall in real terms and fail to recover. This certainly is possible, but the data from the last 20 years doesn’t suggest it has been happening so far. Exhibit 7 shows the valuation of an index of emerging currencies since 1995 in terms of standard deviations against the U.S. dollar.3 As of September 30, the currencies were about 1.3 standard deviations cheap.

But that doesn’t tell the whole story. If the cheapness of the currencies doesn’t have any bearing on the future returns from them, then the possibility of a problem for emerging equity holders is quite meaningful. But historically, at least, valuation has been quite predictive. Exhibit 8 shows the subsequent 1-year returns to the emerging currencies based on how cheap or expensive they were at the start.

Value has been quite a good predictor of emerging currency returns, and from levels similar to today’s, the average return of currencies between 1 and 2 standard deviations below fair value has been about 4% real over the next year. That is no guarantee that the pattern will hold in future, but there is nothing in the historical data that suggests that it will not continue to hold. And looking at the last five years of bad relative returns for emerging equities, we can see that the currencies were almost two standard deviations expensive five years ago, “deserving” a good chunk of the 30.8% of losses that falling emerging currencies have caused since then – about 18% of the total was just the currencies falling back to fair value, while the other 13% has been the currencies moving onto the other side of undervaluation. But even had you been prescient enough to know that the currencies were going to fall over this period, hedging would have cut the currency pain by only a little more than half, as the high interest rates in emerging countries would have eaten into the gains of being short the currrencies.

In total, we can surmise that emerging currencies are a “risk asset” of sorts and that they have delivered a return above U.S. cash over time and should probably continue to do so given the capital needs and vulnerabilities of emerging economies. There still seems to be a meaningful equity risk premium above the return to the currencies, and over history the returns to emerging equities have been of a level that is consistent with them being “equity-like.” Real returns to emerging equities have been reasonably close to the average earnings yield if you adjust for starting and ending valuations, and that’s about all you can ask from equities. We cannot reject the possibility that our normalization of earnings is high relative to “true” normal, but our various estimates are all giving pretty similar answers and there is nothing in the historical data that makes them seem less well-behaved than any other equity group.

Forget about emerging for a second—maybe it is all about the U.S.?

All of the above suggests that valuing emerging equities in the fashion we are doing seems justified. But our ownership of emerging equities stems not just from their expected returns (after all, the current seven-year forecast4 is +4.6%, which implies they are more expensive than “normal”), but from the lousy expected returns available from other equity markets, notably the U.S. A number of justifications have come through in recent years for why the U.S. should trade at higher multiples, much of it centered on the superiority of American shareholder capitalism and the more dynamic U.S. economy. So, let’s look at the evidence for the U.S. superiority.

The first place it seems worthwhile to look is the long-term historical data. Has the U.S. actually outperformed other markets in the long run? The short answer is yes. Exhibit 9 shows the real annualized stock market performance of the countries for whom Dimson, Marsh, and Staunton have continuous stock market data since 1900.

The U.S. was not actually the best performing country, but third out of 21 is still pretty impressive, and the return was a full 2% per year better than the average of all 21, about 1.2 standard deviations above the mean.

Chalking all of this up to American exceptionalism seems a little too hasty, however. If we look at the stronger performing countries over the past 115 years, the secret to success seems to have been “stay away from Europe.” And before declaring that this is an argument for European patheticness even if not American exceptionalism, it is worth remembering that Europe was devastated by two major wars in the period, and the countries in Europe that did the best were generally those that had the good fortune not to be invaded at some point along the way. If we ran a regression using invasion or civil war as one factor and massive inflation as another, the expected return to any country experiencing neither over the period moves to +5.7%, leaving the U.S. 0.8% per year better than expected, down from the 2% outperformance versus all countries, 0.8 standard deviations away from the model. So, in the long run, we could say the U.S. shows evidence of being better than average, but probably not being “exceptional.”

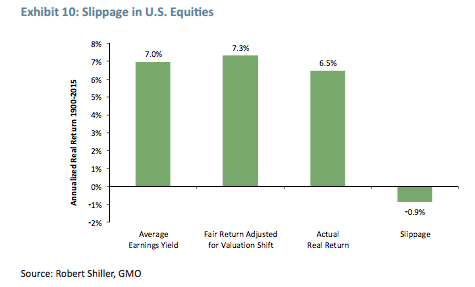

And over that period, the U.S. has certainly not acted "better than equities" in the sense of having a return higher than could be explained by its earnings yield and valuation shift, as can be seen in Exhibit 10. The average earnings yield for the U.S. since 1900 has been 7%, and rising valuations should have added 0.3%/year to returns, but the actual return to U.S. equities has been +6.5%. This suggests 0.9%/year has been lost to slippage, which is not suggestive that the U.S. has been deserving of a premium P/E in the long run.

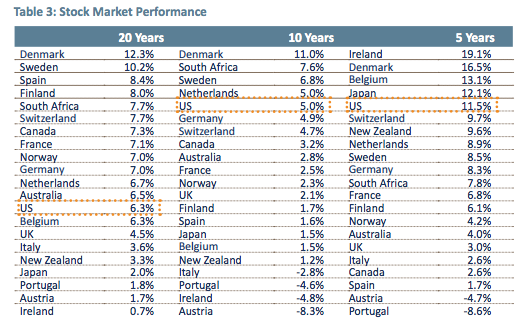

However, 115 years is a pretty long time, and most people arguing for the superiority of the U.S. are thinking about the more recent past. Table 3 shows the performance of the U.S. against the other Dimson, Marsh, and Staunton countries over the past 20, 10, and 5 years.

Over 20 years, the U.S. has clearly been nothing particularly special return-wise. Over the past 10 and 5 years it has been more impressive, in the top quartile of countries and about 0.6 standard deviations above the mean. And, under the surface, it looks somewhat more impressive still over the last decade. If you look at the other countries that have done very well since 2010, almost all of them had a lousy 5 years prior – Ireland, Portugal, Belgium, and Japan were strong performers recently but in the bottom half over 10 years. The lone exception was Denmark, where a single stock, Novo Nordisk, was a huge driver of the returns in both periods.

So the U.S. has been both a strong performer over the last decade and a consistent one. You could see that as a reason why people might want to tell stories about U.S. exceptionalism, but it does not, by itself, count as a lot of evidence that the U.S. truly is exceptional. So what would make the U.S. exceptional? It all comes down to the metrics we looked at for emerging. If the U.S. shows evidence that returns are better than can be explained from earnings yields and valuation shift, it may be deserving of a P/E premium. And if our normalization of earnings is too harsh to them, we could be marking them down for an earnings fall that will not occur.

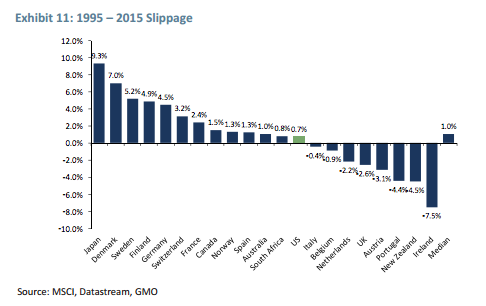

While we know the 115 years of data shows significant slippage from U.S. stocks, that doesn’t mean they might not be doing better over shorter periods. Unfortunately, since our means of calculating slippage can easily get fooled by cyclical shifts due to the business cycle, it’s probably not reasonable to look over periods of less than about 20 years for the evidence, and longer would be better. Exhibit 11 shows the slippage for the U.S. since 1995, along with that of the rest of the developed market universe.

The positive spin on this chart would be that the U.S. has indeed been “better than equities,” giving a return higher than can be explained by its average earnings yield and valuation shift. However, it has not been “better than the rest of equities” in that its slippage has been slightly worse than the median developed country over the period. It is worth spending a little time reflecting over the fact that the emerging markets exhibited worse slippage than the average developed market over that period, with an annualized -0.4%, but that would have actually put it next in line to the U.S. over the period and was only 0.3 standard deviations away from the average over the period.5

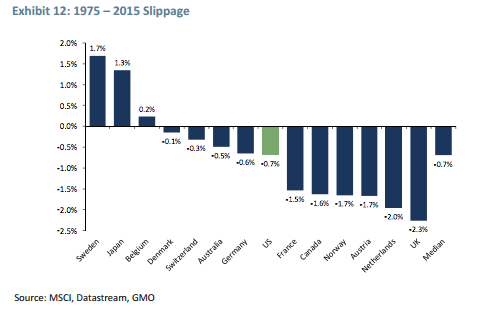

But the large standard deviation of results in this period does suggest that 20 years is at the short end of the length of period you’d want to look at for this type of analysis. Forty years would almost certainly be better. Exhibit 12 shows the results from 1975-2015.

The U.S.’s claim to specialness over this period is more or less completely lacking. Slippage was not materially different from the long-run result for the U.S. and the U.S. was precisely at the median of the countries we have data for. It is worth pointing out that the case for the superiority (at least on this measure) of Anglo-Saxon capitalism is even worse than for the U.S. alone, as the U.K. had the worst slippage of any country over the period, and was noticeably below median for the shorter period as well.

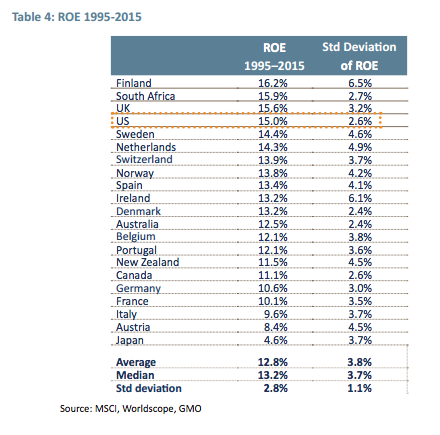

So, does the U.S. have any cause for being called extraordinary? Maybe. It all comes down to the average level of profitability. The U.S. has been one of the highest ROE countries in the world over the last 40 years, as well as one of the most stable from a profitability perspective. Looking since 1995, the U.S. wasn’t quite the top country in the world from an ROE perspective, but close to it, coming in fourth out of 21 countries, just under 1 standard deviation above the mean country (see Table 4).

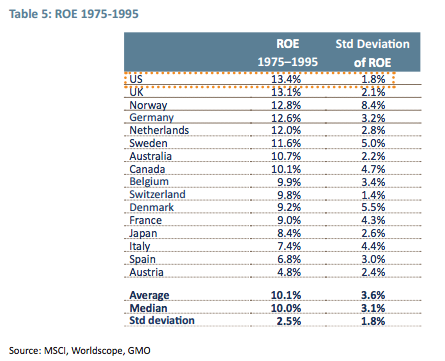

The U.S. also had one of the lowest standard deviations of ROE over the 20-year period, giving it the lovely combination of “high and stable” return on capital, which is the hallmark of high quality companies. And the 1995-2015 period was, if anything, a little less extraodinary than the 20 years from 1975-1995, where the U.S. was the top out of 16 countries for which we have good data (see Table 5).

Again, it makes the U.S. look like the class of the bunch, although the U.K. must also get a shout-out as being basically as profitable over the entire period as the U.S. with only marginally higher volatility. This is certainly exceptional performance in a profitability sense, although because it hasn’t led to lower than normal “slippage,” it implies that while the U.S. should trade at a higher price/book than the average country, it doesn’t deserve a higher P/E. As a firm that has consistently underweighted the U.S. versus non-U.S. markets for the last couple of decades, what we at GMO seem to have gotten wrong is continually fading U.S. profitability back toward that of the rest of the world and its own longer history, while U.S. profitability has instead moved higher. Over the full 40-year period, the margin of U.S. superiority has eroded somewhat, from 3.4% above the average country to 2.2% better since 1995, or from a 1.4 standard deviation outlier to a 0.8 standard deviation one.

Exhibit 13 shows the ROE for the U.S. against EAFE ex-Japan since 1974, with emerging also charted since 1995.

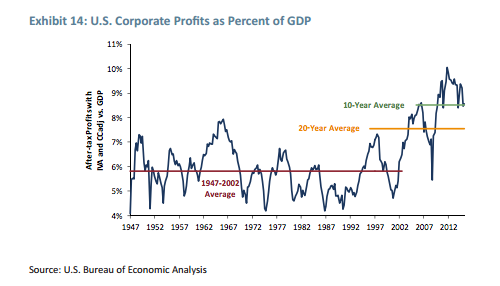

The U.S. has been pretty consistently more profitable and on a generally upward trend. We have been expecting some reversion to the mean on this measure, with the U.S. falling back toward its longerterm average and the rest of the world closing some of the gap over time. The gap over the last decade is smaller than it used to be, but the U.S. has shown no tendency to move back down. Why? Some of this might be chalked up to accounting rules and the impact of stock buybacks on book value, but we see a fairly similar pattern on profitability measures that should be unaffected by problems with book calculations. The clearest driver of the surprisingly good profitability is the rise in corporate profits as a percent of GDP, shown below in Exhibit 14.

When we began building our forecasts, this series had a wonderfully mean-reverting look to it. There had been no obvious trend for the close to 50 years of data, despite plenty of good times and bad in the interim. And the appearance of long-term stability still seemed strong as late as the early 2000s. At the time we excused the new highs of profitability as the consequence of the housing boom and bubble in risk assets. Afterwards profits were good enough to fall through the old average in the financial crisis, although not to the lows we saw in prior recessions. And since then, after the fastest and sharpest recovery on record, we saw them rise well beyond anything the U.S. has ever seen. On this measure, while profitability is off of its recent highs, it is higher than any point in history before 2010.

And this leads to the quandary for thinking about the U.S. stock market. We cannot find any convincing evidence that the U.S. is deserving of trading at a premium P/E to the rest of the world. This profitability, however, could be read either of two ways. Either the U.S. has somehow unlocked a secret to permanently higher profitability or this is an extremely dangerous time to be investing in the U.S. U.S. profitability has never looked materially better relative to the rest of the world than it does today. The bull case would be that, for whatever reason, this profitability gap is sustainable and U.S. stocks are only mildly more expensive than the rest of the developed world given U.S. P/Es are only about a point higher.

But, frankly, we have a hard time believing this bull case. U.S. outperformance in recent years can be readily explained by the better trends in profitability, but that is a long way from saying that outperformance was truly justified. From a macroeconomic perspective, maintaining such high levels of profitability in the face of low investment rates implies ever-increasing wealth inequality in this country, unless taxes were to be raised in a way that seems highly implausible. Generating sufficient end demand in the economy given the inequality would call on either the rich to start spending their wealth at signficantly greater rates than we have seen historically or the rest of households to spend more than 100% of their income, as they did in the housing bubble. It is hard to envision that an economy that relies on those foundations to be a sustainable one.

And even if the U.S. has somehow managed to unlock the secret to permanently high profits and the economy remains solid, it seems unlikely that the secret will remain an entirely U.S. phenomenon. If we imagine a world in which U.S. profitability is able to remain well above historical levels, we would expect non-U.S. companies to begin to copy their American counterparts, similar to the way profitability converged from the 1970s to the early 2000s. In that scenario, we are being too tough on U.S. stocks, but they are still the worst of the global bunch as our forecasts for other equities are similarly underestimated.

Conclusion

The clearest evidence for the U.S. being special today is inextricably tied to its recent performance. In the long run, the U.S. clearly had the good fortune of not having its capital stock destroyed, but otherwise doesn’t look that special. In the shorter term, we have seen an impressive expansion of American profitability that has not been mirrored in the rest of the world, and U.S. stocks have duly outperformed. This has, not surprisingly, led investors to try to convince themselves of the inherent superiority of U.S. stocks to justify continuing to hold them. We cannot completely reject the possibility that those arguments are correct, but the evidence seems pretty thin. Certainly there is no strong evidence that would cause us to believe the U.S. is truly deserving of trading at a higher P/E than the rest of the world. On the profitability front, there seems little doubt U.S. corporate profitability is better than normal, but the question is how much better? Our best estimate is that profit margins are about 24% better than normal, but there is a wider than normal range of possibilities here, with the plausible figures anywhere from 5% to 40% above normal. The impact on our forecast is a range as high as +2% real to a disastrous -4% real for the next seven years, depending on which measure of profitability was the “true” one.

The data on emerging also provides evidence that emerging equities are just equities – neither meaningfully better or worse than those in the developed world over the period for which we have reasonable quality data. There is not a lot of compelling evidence that emerging equities are a value trap, as their slippage has been in the middle of the range against the developed world and completely consistent with the assumptions behind our forecasts. Profitability measures all seem to be saying that today’s earnings are about normal, suggesting a range around our forecast of +4.6% real of as much as +5.7% and as little as +3.4% – and even the worst of these is better than the best of our range for the S&P 500. Currencies make for a further twist to the story, but not a negative one. Their overvaluation in 2011 helps explain the dismal performance of emerging equities since then, but current valuations suggest currencies are more likely to be a tailwind than a drag for emerging equities over the next several years. The historical evidence on emerging currencies further tells us that hedging an emerging equity portfolio is quite likely to reduce returns in the long run, as emerging currencies have had returns consistent with the intuition that they are a species of risk asset.

None of this guarantees that future developments might not prove the U.S. to be more extraordinary than its history suggests, or that emerging markets may prove worse than their history implies. Still less does it suggest that emerging markets will necessarily outperform the U.S. next year. We have seen more extreme valuation discrepencies between the two before, and such a gap can only occur when the relatively cheap asset continues to underperform. But our goal here was not to generate guarantees, but rather take a hard look at these assets to understand whether the basic assumptions underlying our forecasts still seem like the correct ones. Despite the strong recent performance of the U.S. and the weak performance for emerging, neither has shown evidence that suggests we should change our assumptions.

1 Our reason for excluding financials is somewhat different. The rather odd thing about financials relative to other industries is that a high return on equity capital is as likely to be a sign of weakness as strength. Overly-levered financial firms generally look extremely profitable in the good times but have no cushion against losses when the cycle turns.

2 Actually, there is an economic theory, the Balassa-Samuelson effect, which suggests that emerging countries could have permanently increasing real exchange rates as long as their productivity growth is outstripping that of the developed world. The theory is intuitively plausible and the historical evidence for it is pretty strong, but for plausible levels of productivity growth, the effect is going to be fairly small on an annualized basis.

3 I’m doing something here that may look like cheating. The “index” of currencies I’m using is a static equal weighted index of 10 emerging currencies, rather than the actual MSCI equity index or J.P. Morgan Currency index. The MSCI and J.P. Morgan indices have different weights from each other and both include some currencies that are fairly illiquid and difficult to trade. This group’s valuations are quite similar to those of both of those indices, but are liquid enough that we are pretty confident we can properly estimate the returns to holding the currencies accurately.

4 The above forecast is for the named asset class as of September 30, 2015 and not for any GMO fund or strategy. These forecasts are forward‐looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward‐looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward looking statements. Forward‐looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from the forecasts above.

5 It isn’t quite right to compare emerging equities, a universe that consists of over 20 countries, to individual countries on this measure, but, on the other hand, looking at each individual country could be misleading as well, given that the country weights in the index have changed quite significantly over the 20-year period.

Disclaimer: The views expressed are the views of Ben Inker through the period ending December 2015, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2015 by GMO LLC. All rights reserved.

Give Me Only Good News!

Jeremy Grantham

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

(Attributed to Mark Twain)

It takes little experience in the investment business to realize that investors prefer good news. As a bear in the bull market of 1999 I was banned from an institution’s building as being “dangerously persuasive and totally wrong!” The investment industry also has a great incentive to encourage this optimistic bias, for little money would be made if the market ticked slowly upwards. Five steps forward and two back are far more profitable.

Similarly, we environmentalists were shocked to realize how profoundly the general public preferred to believe good news on our climate, even if it meant disregarding the National Academies of the world. The fossil fuel industry, not surprisingly, encouraged this positive attitude. They had billions of dollars to protect. If the realistic information were to be widely believed, most of their assets would be stranded.

When dealing with realistic limits to growth it is also obvious how reluctant everyone is to accept the natural mathematical limits: There simply cannot be compound growth in a finite world. A modest 1% growth compounded for the 3,000 years of Ancient Egypt’s population would have multiplied its economic output by nine trillion times!1 Yet, the improbability of feeding ten billion or so global inhabitants in 50 years is shrugged off with ease. And the entire economic and political system appears eager to encourage optimism on resources for it is completely wedded to the virtues of quantitative growth forever.

Hard realities in these three fields are inconvenient for vested interests and because the day of reckoning can always be seen as “later,” politicians can always find a way to postpone necessary actions, as can we all: “Because markets are efficient, these high prices must be reflecting the remarkable potential of the internet”; “the U.S. housing market largely reflects a strong U.S. economy”; “the climate has always changed”; “how could mere mortals change something as immense as the weather”; “we have nearly infinite resources, it is only a question of price”; “the infinite capacity of the human brain will always solve our problems.”

Having realized the seriousness of this bias over the last few decades, I have noticed how hard it is to effectively pass on a warning for the same reason: No one wants to hear this bad news. So a while ago I came up with a list of propositions that are widely accepted by an educated business audience. They are widely accepted but totally wrong. It is my attempt to bring home how extreme is our preference for good news over accurate news. When you have run through this list you may be a little more aware of how dangerous our wishful thinking can be in investing and in the much more important fields of resource (especially food) limitations and the potentially life-threatening risks of climate damage. Wishful thinking and denial of unpleasant facts are simply not survival characteristics.

Let me start with one of my favorites. For the 50 years I have been in America, Business Week and The Wall Street Journal have been telling us how incompetent at business the French are and how persistently we have been kicking their bottoms. If only they could get over their state socialism and their acute Eurosclerosis. And as far as I can tell we have generally accepted this thesis. Yet Exhibit 1 shows what has actually happened to France’s median hourly wage. It has gone from 100 to 280. Up 180% in 45 years! Japan is up 140% and even the often sluggish Brits are up 60%. But the killer is the U.S. median wage. Dead flat for 45 years! These are the uncontestable facts. So, all I can say is that it is just as well the French have not been kicking our bottoms. But how is it that we can believe so firmly in something that just ain’t so, and by such a convincing amount?

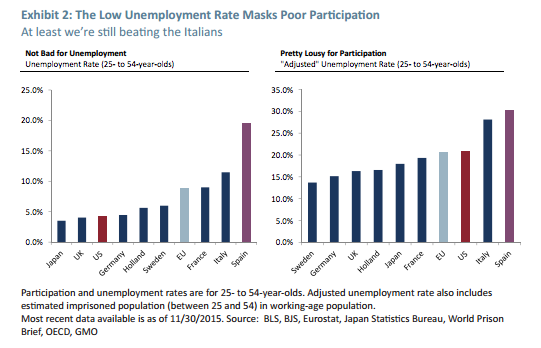

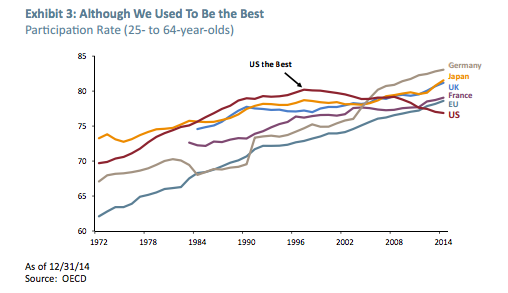

Exhibit 2 examines the proposition that although our wages may have done poorly, we are still the place that creates jobs. The left-hand panel certainly seems to confirm that with our modest official unemployment rate for 25- to 54-year-olds of below 5% compared to 9% for the E.U. The righthand panel, though, shows the true picture. It looks at the unemployment rate adjusted for the nonparticipation rate, the percentage of all 25- to 54-year-olds who are not actually working (i.e., it includes those discouraged, uninterested, or even sitting in jail). There are now 21% not employed in the U.S. compared to 20.5% for the E.U., and our long-suggested job creating skills are looking a little thin. The problem lies in the so-called participation rate, as shown in Exhibit 3. The U.S. was one of the leaders in the percentage of women working, and from 1972 to a peak in 1997 the U.S. participation rate rose from 70% to 80%. From 1984 on, the U.S. spent 20 years ahead of most other countries in participation rates, but after 1997 something appears to have gone wrong: While other developed countries continued to increase their participation rate, that of the U.S. declined from first to last in fairly rapid order. What a far cry this reality is from the view generally accepted by our business world.

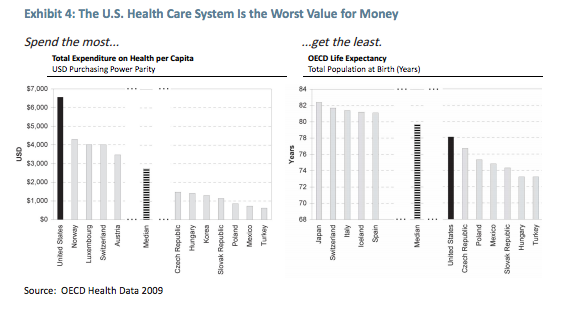

Exhibit 4 examines our belief that we have the best health care system in the world. And why shouldn’t we, given the money we put in (left-hand bar chart), over twice the average cost paid by the E.U. But the right-hand bar chart shows what we get back. Two years less life than the median. And watch out for when the Turks, Poles, and Czechs cut back on smoking, for then we may find our way to the bottom of the list.

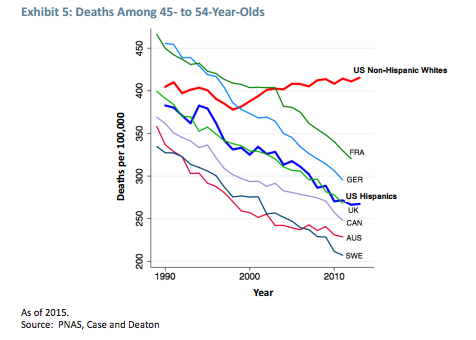

But if you really want to be worried about our comparative health you should take a look at Exhibit 5, which comes hot off the press from the guy2 who was just awarded the Nobel Prize for Economics (wait a minute, must be some mistake, this work seems perfectly useful). The data shows the death rate for U.S. whites between the ages of 45 and 54, which happily these days is when very few people drop off. Since 1990 there has been a quite remarkable decline for other developed countries, about a one-third reduction, as you can see, including for U.S. Hispanics. But for U.S. whites there is a slight increase! Further analysis for that group reveals that the general increase is caused by quite severe increases in deaths related to alcoholism, drug use, and suicides. Had the rate for U.S. whites declined in line with the others there would have been about 50,000 fewer deaths a year! (For scale, this is nearly twice the yearly number of traffic deaths in the U.S.)

You have to be careful these days when you suggest connections. For example, people have been told off for proposing that dramatic increases in population can help destabilize societies. Syria had two and a half million people when I was born and has 29 million people now. You can guess how much worse the situation is because of this but you should not talk about it. Similarly, Prince Charles has been extensively criticized by professors in The Guardian3 for suggesting that a several-year drought in Syria exacerbated social tensions by ruining many farmers. As if! (You cannot prove precisely what effect climate damage had, but you certainly cannot prove that it did not have a large effect. It certainly had a contributory effect.)

With that caveat, let me seriously suggest a connection between Exhibit 1, which shows no increase in the U.S. median wage for over 40 years following a wonderful prior 30 years of a rise of over 3% a year, and Exhibit 5, which shows the uptick in unnecessary deaths among U.S. non-Hispanic whites aged 45 to 54. This is precisely the age group that was led to expect better for themselves and much better for their children. But those aspirations have not been generously fulfilled. The U.S. Hispanics, in contrast, mostly arrived later and had different expectations. All in all, this data is quite bleak. The point here is that it bears absolutely no similarity to the more optimistic belief set that is generally accepted.

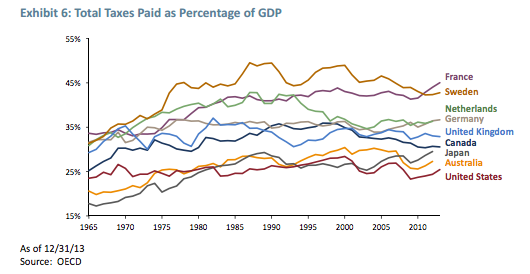

The data presented in Exhibit 6 examines the proposition that “more and more goes to the government and soon they will have everything.” You have heard that many times recently in the political debate. Sorry, “bull sessions.” You can see that the U.S. share going to the government in taxes is about the least in the developed world and that it has barely twitched for 50 years. Yet, apparently we have been steadily going to hell. How is it possible that such a view is given such credence in the face of the data, which is, after all, official and simple, not ingeniously manipulated by some perfidious Brit. (Yes, I admit it, I consider myself American or British depending on whether the context is favorable or not.)

“At least we live in a fair society” is the proposition examined in Exhibit 7. The Gini Ratio is a measure of income inequality. Low is good. Only Turkey and Mexico outflank the U.S. as more unequal amongst the richer countries. I was a bit surprised to see how high the U.S. already was in 1980 (I had been drinking from the same culture dissemination trough after all), but it was at least importantly lower.

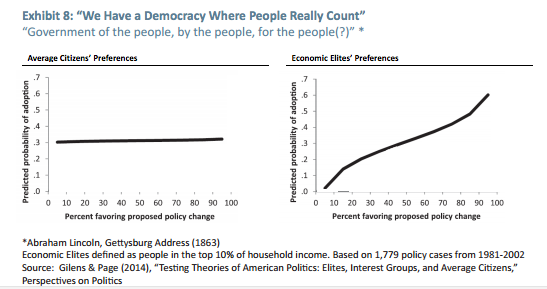

“We have a democracy where people really count” is an idea that is built into the background cultural noise. Exhibit 8 (also covered last quarter) on the left shows how the probability of a bill passing through Congress is affected by the general public’s enthusiasm or horror. In a nutshell, not at all! The financial elite, on the other hand, can double the chance of a bill passing or, much more disturbingly, can completely block passage. Clearly these facts are totally incompatible with the concept of participatory democracy and equally entirely at odds with the much more favorable and optimistic beliefs we share about our democracy. We really, really want to believe good news and to believe that we have a superior system that only needs fine-tuning. But, it ain’t necessarily so.

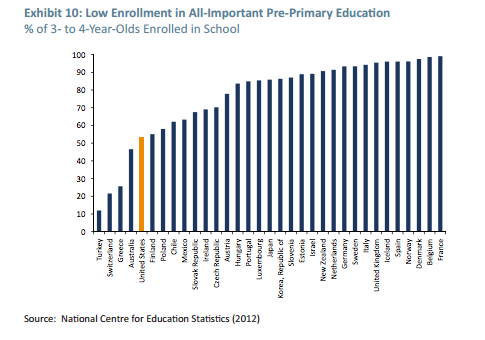

“We have the best education system in the world” is a proposition that goes without saying in Boston, with Harvard, MIT, and literally dozens of other universities. But Exhibit 9 shows the more downto-earth fact: mediocrity. Less than mediocre, though, is the data in Exhibit 10, which shows the percentage of 3- to 4-year-olds enrolled in school. This is an area of emphasis where the returns on investment are said to be particularly high – six for one – although I would not like to guarantee such returns myself. However, our relatively low ranking at the start of the process is not heartwarming.

Exhibit 11 moves on to our production of CO2, which per capita is the largest in the world, just ahead of Australia. The two of us also worry the least, except for one Middle Eastern oil producer. There is a nice, i.e., interesting, negative correlation here of -0.54. Not bad at all. The greater your fossil fuel intensity, the more ingenious your fossil fuel propaganda is to create doubt and the more we are encouraged to think beautiful optimistic thoughts: clean coal and clean oil. And even as more people can see the climate damage, the richer countries can convince themselves that the damage is not that serious. Poorer countries, meanwhile, do not have that luxury and about 20% more are actively concerned (about 80% vs. 60%) than are the richer countries.

And this brings me to the last and my absolute favorite of these false propositions, which I label, “I wish the U.S. government wouldn’t give so much to foreign countries (especially when times are bad)!”

Now, I do not think I have met a single American who does not believe that the U.S. government is generous in its foreign aid. Yet, it just ain’t so, and by a remarkable degree. Exhibit 12 shows what other developed countries give, with the usual goody-goody Sweden leading the way with 1.4% of their GDP and the U.K. having quite recently shot up to 0.8%, for once ahead of Japan and Germany. Dead last is the U.S. at 0.2% of GDP, which it has averaged forever. This is the item with the biggest and most permanent gap between reality and perception. And, as always, the misperception is in favor of the favorable, the data that we would wish to be true.

Conclusion

This is more or less the best I can do to prove the point. We in the U.S. have a broad and heavy bias away from unpleasant data. We are ready to be manipulated by vested interests in finance, economics, and climate change, whose interests might be better served by our believing optimistic stuff “that just ain’t so.” We are dealing today with important issues, one so important that it may affect the long-term viability of our global society and perhaps our species. It may well be necessary to our survival that we become more realistic, more willing to process the unpleasant, and, above all, less easily manipulated through our need for good news.

Postscript/Codicil

Just as I finished my quarterly, I found myself looking at a cover story for The Economist (November 7) that seemed to be a wonderfully convenient example of my general thesis: the efforts that are made by vested interests to exploit our reluctance to face inconvenient facts.

The Paris climate talks have begun and a large number of reasonable speeches and articles are putting their best foot forward in support of sensible progress. But The Economist’s special coverage on climate is not one of them. In fact, I urge you to realize that this normally reasonable newspaper, inadvertently I’m sure, is regrettably helpful in this report to the fossil fuel industry: Ignore carbon taxes, they suggest, and follow Bjorn Lomborg and his Copenhagen Consensus Center, which is discussed so favorably here, into scores of deworming programs before you waste money on combatting climate change. When finally you spend any money at all, spend it on completely new technologies and not on solar and wind, which are by implication considered failed approaches despite the remarkably rapid decline in prices in recent years. But if we wait for entirely new technologies, climate damage may have by then gone beyond a tipping point. Indeed, a great majority of climate scientists would say that there is some chance of that and what chance of real disasters should we be willing to take? Any successful attempt to limit climate damage must at least include a price on carbon. Any suggested program that does not is either disingenuous or an outright con. They may argue that we can wait and research until we have a more perfect solution, but I believe that “wait” is their main purpose, not “solutions.”

1 See the Special Topic in GMO’s July 2008 Quarterly Letter, “Living Beyond Our Means: Entering the Age of Limitations,” available at www.gmo.com.

2 Angus Deaton, recipient of the 2015 Nobel Memorial Prize in Economic Science.

3 The Guardian, like Prince Charles, is very fervent about climate change. It is, however, Republican – as opposed to Monarchist – and likes to beat up on Prince Charles when it can. You can see how its creative tension was resolved this time.

Disclaimer: The views expressed are the views of Jeremy Grantham through the period ending December 2015, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2015 by GMO LLC. All rights reserved.

© GMO