As we approach the end of the year, it is customary to take stock of major developments. Economic data point to continued forward momentum in the United States. All in, the economy has grown at an average pace of 2.2% during the first three quarters of the year, nearly matching the potential growth rate of the economy. The labor market is in a significantly better spot than it was at the beginning of the year. Inflation is low despite the age of the expansion.

Third-quarter real gross domestic product (GDP) growth was revised to 2.1% versus the advance estimate of 1.5%. The revision reflects mostly a smaller reduction of inventories than previously reported. The final quarter of the year shows a small acceleration in activity compared with the prior quarter.

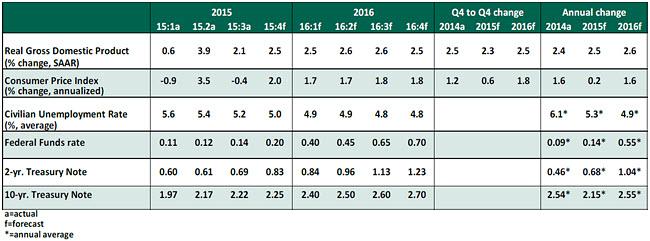

Key Economic Indicators

Key Elements of Forecast

- Consumer spending posted increases of 3.0% or higher in five of the last six quarters. Warm weather resulted in smaller utility bills and trimmed total consumer spending in October. Auto sales averaged 18.2 million units in the October-November period versus a 17.8 million average in the third quarter. Early reports of holiday sales suggest a modest increase. Lower gasoline prices could give an extra boost to holiday gift shopping.

- The housing sector reports point to soft conditions. Purchases of new homes rose nearly 11% in October to 495,000, but it largely offset the revised weak September data. Sales of existing homes fell 3.4% in October to 5.36 million units and reversed a large part of the improvement seen in September. The reason for the recent disappointing pace of activity in the housing sector is unclear, as employment conditions and low mortgage rates are supportive of growth in home sales. Inventories of unsold homes are low, and home prices are moving up. The outlook for housing is positive but not robust.

- Business-sector spending (+9.5%) was surprisingly strong in the third quarter. Factory production advanced 0.4% in October following two monthly declines. However, the new orders and production indexes of the Institute of Supply Management’s factory survey fell in November. Weak foreign demand and a strong dollar are holding back factory activity. Hiring in the oil-related industry remains weak. Outside of the auto sector, manufacturing activity has been very modest.

- Exports remain vulnerable to the dollar’s strengthening trend and the weak position of U.S. trading partners. Exports slipped 1.4% in October following a 0.5% decline in the third quarter. Imports recorded an unexpected decline in October. The bottom line is that the trade gap widened in October. These preliminary signals suggest that net exports will be a drag on fourth-quarter GDP growth.

- Inflation readings are far below the Fed’s 2.0% target. Oil prices, one of the major drivers of inflation, have declined recently. The inability of the oil exporting nations to compromise on production has affected oil prices. Rents that make up a large part of inflation are lifting core price measures.

Of late, Federal Reserve Bank presidents have drawn attention to the Dallas Fed’s Trimmed Mean Personal Consumption Expenditure Index (excludes outliers of components of the Personal Consumption Expenditure Price Index), which shows a 1.7% increase from a year ago. The Federal Reserve predicts an acceleration of inflation, as the economic growth trajectory looks promising.

- Uncertainties about the labor market stemming from modest hiring gains during August and September were set aside after the October and November employment numbers. The unemployment rate held steady at 5.0% and the 3-month moving average for job growth is 218,000. Other labor market indicators that Fed Chair Janet Yellen follows closely have shown improvements in the last six months. The U.S. economy is close to meeting the Fed’s full-employment mandate.

- China remains the main source of global economic risk. China’s foreign exchange reserves, its largest economic arsenal, have begun dwindling. The geopolitical risks in the Middle East remain a threat to global economic growth.

- Market expectations for a change in Fed policy have risen. The 2-year U.S. Treasury note’s ascent to 0.93% as of this writing – about a 20-basis-point increase since the October Fed meeting – reflects this assessment.

- Given the nature of U.S. economic progress, the discourse has turned to normalizing interest rates. Monetary policy has long and variable lags, so getting a head start allows the Fed to proceed cautiously. Stay tuned for an update about Fed policy following the Federal Open Market Committee meeting on December 16.

(c) Northern Trust