KEY TAKEAWAYS

· Our view is that the U.S. economy—as measured by real GDP—is likely to post growth of 2.5–3.0% in 2016.

· Manufacturing, business capital spending, and net exports may take larger roles in U.S. economic growth, with continued support from consumer spending.

· We believe that economic growth outside the U.S., in both developed and emerging economies, may accelerate modestly in 2016.

This week’s commentary features content from LPL Research’s Outlook 2016: Embrace the Routine.

Our view is that the U.S. economy—as measured by real gross domestic product (GDP)—is likely to post growth of 2.5–3.0% in 2016. This rate is below its post-World War II average of 3.2%, but above the 2–2.5% average growth rate seen in the first six-and-a-half years of this expansion, based on the factors discussed below. Despite the length of the current expansion (already the fourth longest on record), it has not followed what would be considered a routine path. Supportive monetary policy from the Federal Reserve (Fed) has remained in place throughout the expansion; economic growth, while steady, has been below trend; and inflation, which often picks up near the middle of the cycle, remains near cycle lows. While we believe we are likely in the second half of the economic cycle, 2016 may be the first typical mid-cycle year of the expansion, and investors may need to figure out what it means to get back to that routine.

Returning to Our Typical Sources for Growth

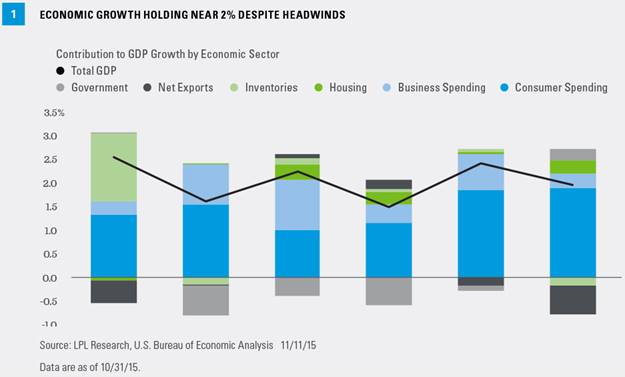

As we plan ahead for 2016, the mix of economic growth may look a bit different than in 2015, with manufacturing, business capital spending, and net exports potentially taking larger roles. The manufacturing economy is stabilizing after a difficult 18-month period (mid-2014 to late 2015) and may accelerate further. The housing sector is expected to contribute to growth for the sixth consecutive year, and the consumer sector may continue adding to growth, benefiting from low energy prices, record levels of household net worth, and still low consumer interest rates. Business capital spending struggled in late 2014 and throughout 2015 amid the collapse in oil prices and stronger U.S. dollar. We believe oil prices may move modestly higher as demand remains strong and, as we’ve started to see in 2015, supply comes down. Business capital spending may add to growth in 2016 as commodity prices stabilize [Figure 1].

The hallmark of this current economic expansion has been underinvesting, especially in research and development, and while we do not expect a boom in 2016, there is potential for some catch-up spending. Net exports, which were a sizable drag on growth in both 2014 and in the first three quarters of 2015, may stabilize as the dollar consolidates after the 20%+ gain between mid-2014 and mid-2015—matching the largest 12-month increase in the value of the dollar versus its major trading partners since the dollar went off the gold standard in the early 1970s [Figure 2]. We expect the dollar will begin to stabilize as central bank policies and the outcomes of those policies become clearer. A stabilizing dollar should help to boost exports and remove a key headwind for manufacturing and profits of U.S. corporations.

Continued Progress for Employment & Wages

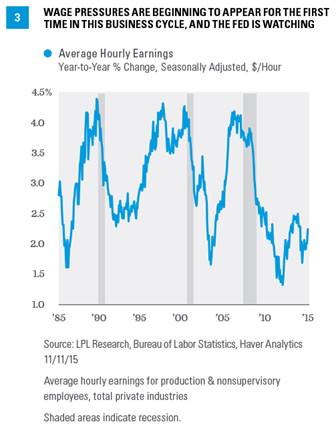

We expect continued progress in the U.S. labor market in 2016, with the economy generating enough jobs to nudge the unemployment rate ever closer to the elusive “full employment” range, the level at which, in the past, businesses need to raise wages to attract and retain skilled employees. Wage growth has been limited but should continue to accelerate in 2016 [Figure 3]. This acceleration in wages—if not accompanied by better economic growth—may cause headaches for the Fed as it begins to normalize policy in 2016. We expect the Fed to begin raising rates in late 2015 or early 2016, with our focus on the pace of hikes throughout 2016 and beyond.

Checking Off Inflation

Inflation remains in check, but commodity/goods inflation may be poised to make a comeback, which would help keep the Fed on schedule to begin raising rates. Since the middle of 2009, prices of services in the economy (as measured by the Consumer Price Index [CPI] for services) accelerated from under 1.0% to as high as 2.8% in early 2014, and then settled into a range of 2–2.5%. Prices of services (medical services, rents, etc.) account for over two-thirds of overall CPI, and history suggests that as the business cycle ages, and as the housing and labor markets tighten, service inflation may continue to accelerate. The Fed has to watch this closely.

However, the CPI for goods (prices of oil and other commodities purchased by consumers) sank along with oil prices from mid-2014 through late 2015. This kept the U.S. economy flirting with deflation (a prolonged period of falling wages and prices). Overall CPI posted a 2.1% year-over-year gain in mid-2014, and by the end of October 2015, the overall CPI was just 0.2%. Looking ahead to 2016, if oil prices move up as we expect, the goods portion of CPI may increase by 2–3%; and if the pace of service sector inflation remains between 2% and 2.5%, overall CPI will accelerate quickly and may be well over 2.0% by year-end. By then, the Fed will have already begun raising rates.

The Consumer Price Index (CPI) is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services, and is a commonly used measure of inflation.

Watching the Fed: Disruption or Distraction?

The start of a new Fed rate hike cycle may grab investors’ attention in 2016, but investors must distinguish where it is more likely to disrupt their accustomed routine (bonds) and where it is more likely to be just a distraction (stocks). In addition, the market and the Fed remain deeply divided over the timing and pace of Fed rate hikes, and how that gap is resolved will determine the extent of the effects on the markets. As a reminder, the start of Fed rate hikes does not signal the end of economic expansions. Indeed, since 1950, the start of Fed rate hikes meant that the economy was still in the first half of the expansion.

We believe a rate hike in December 2015 remains a strong possibility. Our view remains that when the Fed does raise rates—likely in late 2015 or early 2016—that the timing of the first hike matters less than the pace of the hikes; the end point for the fed funds rate in this tightening cycle (the first since 2004) and the gap between the Fed’s own view of rates and the market’s view remain crucial.

The Federal Open Market Committee’s (FOMC) latest forecast of its own actions (September 2015) puts the fed funds rate at 1.375% by the end of 2016. As of November 23, 2015, the market (as defined by the fed funds futures market) puts the fed funds rate 0.50–0.75% lower at around 0.81% by the end of 2016. How that gap closes—between what the market thinks the Fed will do and what the Fed is implying it will do—against the backdrop of what the Fed actually does, will be a key source of distraction for markets in 2016. Our view is that the Fed will hike rates in late 2015/early 2016, and by the end of 2016, push the fed funds rate into the 0.75–1.0% range.

Fiscal Stimulus Around the Globe

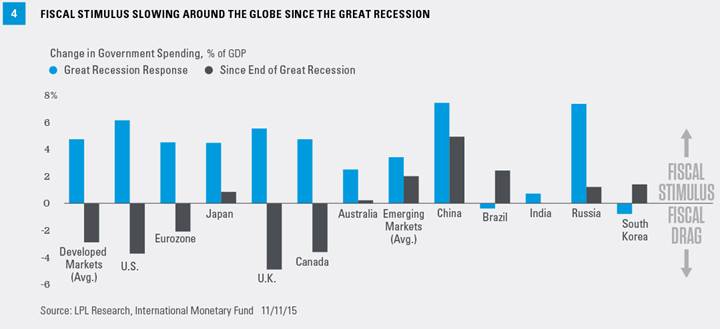

In the wake of the Great Recession (2007–09), governments across the globe, in both developed and emerging markets, increased fiscal stimulus (more government spending, tax cuts, or some combination of the two) to combat the worst global downturn in 75 years. As the global economy emerged from the Great Recession over the past half-decade or so, governments reined in—and in some cases, reversed—the fiscal stimulus put into place during and after the Great Recession, most notably in developed markets. In emerging markets, fiscal stimulus continued, but at a slower pace than during the Great Recession, led by China [Figure 4].

Looking out to 2016, markets don’t expect much in the way of fiscal stimulus in either developed or emerging economies. Thus, any stimulus that is enacted would likely be viewed as a positive surprise to markets looking for any boost to global growth.

Focusing on the U.S., outside of the major entitlement programs (Medicare, Medicaid, and Social Security), U.S. fiscal policy at the federal level has been restrictive since the $787 billion fiscal stimulus plan was enacted by Congress in 2009. While there is some historical evidence that fiscal stimulus picks up in an election year, historically, the odds of Congress passing meaningful fiscal stimulus that would impact growth before 2017 is low. However, the election of Paul Ryan (R-WI) as Speaker of the House in October 2015 increases the chances that market-friendly legislation is passed into law in 2016.

Adding Global Growth to the Agenda

We believe that economic growth outside the U.S., in both developed and emerging economies, may accelerate modestly in 2016, albeit from fairly low growth in 2015. A key differentiator is likely to be the role commodities play in a given economy. While economic growth in developed economies (generally commodity consumers) accelerated in 2014 and 2015, emerging market economies have, in aggregate, been decelerating since 2010. Though many factors are at play, China has an outsized role as the marginal consumer of commodities. While the U.S. economy is becoming increasingly sensitive to global matters, on balance, the U.S. economy is still among the least export sensitive of any major economy.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide or be construed as providing specific investment advice or recommendations for any individual security. To determine which investments may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

Economic forecasts set forth may not develop as predicted, and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, disease, and regulatory developments.

Currency risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

DEFINITIONS

The Federal Open Market Committee (FOMC) is the branch of the Federal Reserve Board that determines the direction of monetary policy. The 11-person FOMC is composed of the 7-member board of governors, and the 5 Federal Reserve Bank presidents. The president of the Federal Reserve Bank of New York serves continuously, while the presidents of the other regional Federal Reserve Banks rotate their service in one-year terms.