The market downturn and ensuing volatility in the third quarter of 2015 is a timely reminder about the benefits of diversifying your portfolio with investment strategies that are expected to exhibit little-to-no correlation with the broad equity and bond markets.

Moreover, as the US enters the late innings of its current economic growth cycle, many professional and individual investors are expecting lower returns from equities going forward than they’ve enjoyed over the last few years. These lowered expectations are on top of concern about what will happen to investors’ bond holdings when today’s historically low interest rates eventually rise.

The Invesco Quantitative Strategies team believes one potential way to buffer the effects of market downturns, volatility and rising interest rates is to add market neutral equity strategies to traditional portfolios, as they potentially offer a unique approach to generating return regardless of the general movements of the equity and bond markets.

In this blog, I outline four of the top reasons to consider market neutral equity strategies:

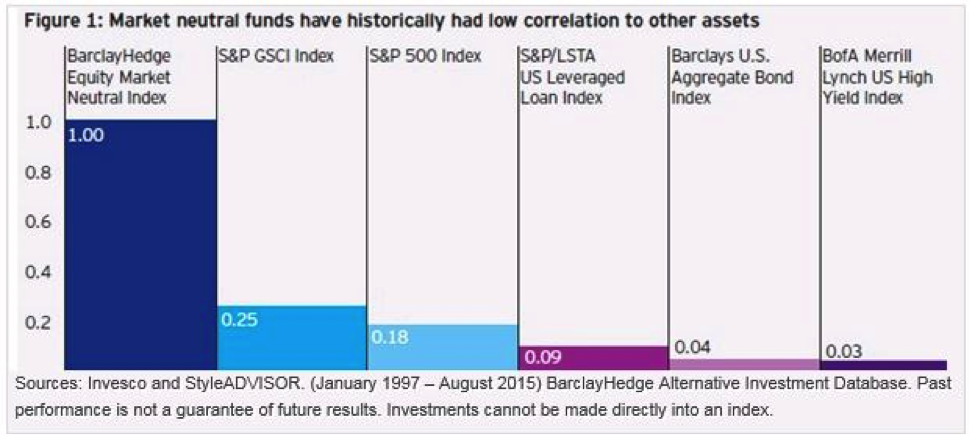

1. They have very low levels of correlation to other asset classes

One of the ways investors attempt to manage and mitigate risk is by combining strategies that differ within and across asset classes to help diversify their return pattern over time. Using this approach, investors’ wealth creation is not tied to the fortunes of just one or a few investment options. Since market neutral strategies typically seek to eliminate exposure to the broader market, these strategies have also delivered attractively low levels of correlation, not only to the equity markets, but to other broad asset classes as well.

As shown in Figure 1, from January 1997 to August 2015, market neutral strategies had only a 0.18 correlation to equities and a 0.04 correlation to bonds. Market neutral also had low correlation to another popular asset class, commodities, as well as to other segments of the fixed income market, such as leveraged loans and high yield. As investors seek to diversify their holdings in order to lower overall volatility, we believe market neutral strategies should be considered as a way to achieve that goal.

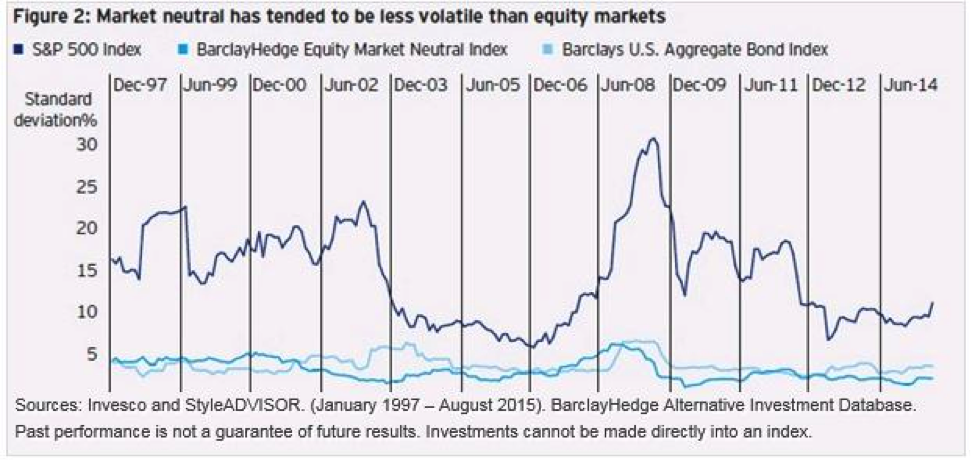

2. They may offer lower levels of total volatility

Another way to potentially mitigate risk across an investment lineup is to include strategies that may offer lower levels of total volatility (variation in portfolio returns). Even if these strategies were perfectly correlated with other investments, their potentially lower total volatility profile could help lower the overall average volatility of the full lineup. Market neutral strategies also may be appealing to investors from this total volatility perspective, as their volatility has tended to be less than the broader equity markets, and in some cases, similar to broad fixed income indexes (see Figure 2). Furthermore, since market neutral returns are expected to be independent of the broader equity market, a spike in market-level volatility may not necessarily mean a spike in market neutral volatility.

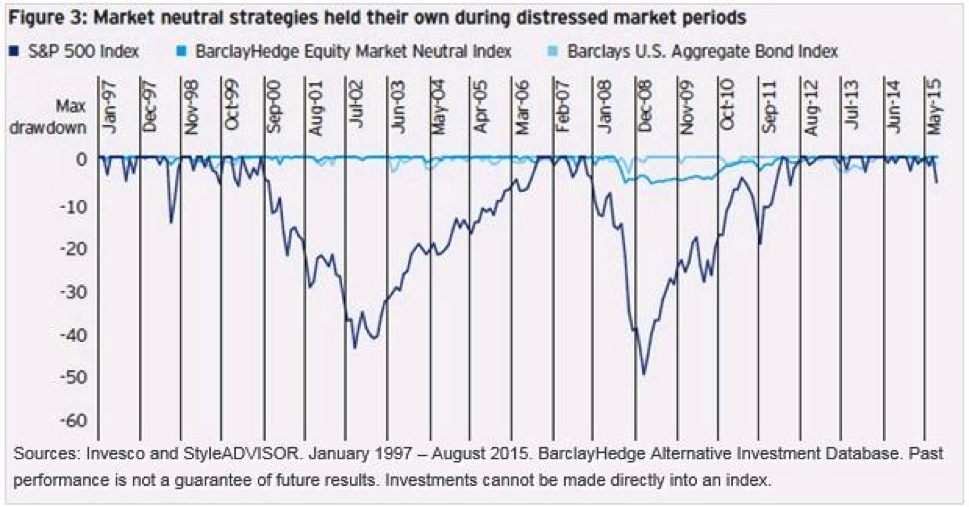

3. They have a history of attractive downside protection during extreme market stress

Another often-cited potential benefit of market neutral is that the strategies may offer investors a way to mitigate severe losses during a sharp equity market sell-off. Because these strategies typically have beta exposure to the market that hovers around zero, a big drop (or surge) in equities should not influence the performance of the strategy. This contrasts sharply with traditional, benchmark-centric strategies, which typically have very high levels of market exposure and tend to vary similarly to the broader market.

4. They can provide an opportunity for higher returns in a rising interest rate environment

We believe an increase in the federal funds rate from the US Federal Reserve is inevitable; at this point it’s simply a matter of when and by how much. For market neutral equity strategies, a rise in interest rates – specifically short-term interest rates — can potentially provide a boost to returns. This occurs when market neutral equity strategies short a stock and receive proceeds from that sale. Those proceeds typically earn a rate of return tied to the prevailing short-term interest rate, such as the fed funds rate. When that rate increases, so does the interest earned by market neutral equity strategies on their short sale proceeds.

Key takeaway

We believe a market neutral equity strategy is a valuable complement to a traditional portfolio of stocks and bonds, as well as an excellent diversification tool that enables investors to pursue increased returns from assets that respond differently to changing market conditions. Such characteristics may be important to today’s investors given the recent market downturn, volatility and expectation of rising interest rates.

Important information

Beta is a measure of risk representing how a security is expected to respond to general market movements.

Correlation is the degree to which two investments have historically moved in relation to each other.

Volatility measures the amount of fluctuation in the price of a security or portfolio over time.

The S&P 500® Index is an unmanaged index considered representative of the US stock market.

The S&P/LSTA US Leveraged Loan 100 Index is representative of the performance of the largest facilities in the leveraged loan market.

The S&P GSCI Index is an unmanaged world production-weighted index composed of the principal physical commodities that are the subject of active, liquid futures markets.

The BofA Merrill Lynch US High Yield Index tracks the performance of US dollar-denominated, below-investment-grade corporate debt publicly issued in the US domestic market.

BarclayHedge Alternative Investment Database is a computerized database that tracks and analyzes the performance of approximately 6800 hedge fund and managed futures investment programs worldwide. BarclayHedge has created and regularly updates 18 proprietary hedge fund indices and 10 managed futures indices. BarclayHedge indexes reflect performance of hedge funds, not of retail investment strategies, and are used for illustrative purposes only solely as points of reference in evaluating alternative investment strategies. Please note: BarclayHedge is not affiliated with Barclays Bank or any of its affiliated entities. Performance for funds included in the BarclayHedge indices is reported underlying fees in net of fees.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

About risk

Commodities may subject an investor to greater volatility than traditional securities such as stocks and bonds and can fluctuate significantly based on weather, political, tax, and other regulatory and market developments.

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Most senior loans are made to corporations with below investment-grade credit ratings and are subject to significant credit, valuation and liquidity risk. The value of the collateral securing a loan may not be sufficient to cover the amount owed, may be found invalid or may be used to pay other outstanding obligations of the borrower under applicable law. There is also the risk that the collateral may be difficult to liquidate, or that a majority of the collateral may be illiquid.

Junk bonds involve a greater risk of default or price changes due to changes in the issuer’s credit quality. The values of junk bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

Derivatives may be more volatile and less liquid than traditional investments and are subject to market, interest rate, credit, leverage, counterparty and management risks. An investment in a derivative could lose more than the cash amount invested.

Short sales may cause the fund to repurchase a security at a higher price, causing a loss. As there is no limit on how much the price of the security can increase, the fund’s exposure is unlimited.

Before investing, investors should carefully read the prospectus and/or summary prospectus and carefully consider the investment objectives, risks, charges and expenses. For this and more complete information about the fund(s), investors should ask their advisors for a prospectus/summary prospectus or visit invesco.com/fundprospectus.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.

Four key reasons to consider market neutral investing