The government official who drafted an obscure add-on to the Internal Revenue Tax Code back in the 1970s could have had no inkling regarding the consequences.

If you're a plan sponsor or retirement advisor, chances are one of the biggest issues you face feels like a four-letter word: QDIA.

In fact, picking the right qualified default investment alternative is such a big issue—it affects millions of Americans who use defined contribution plans—that a government watchdog agency recently looked into it. And what they found might surprise you.

According to a new report by the US Government Accountability Office (GAO), the US Department of Labor's (DOL) guidance on how to pick a QDIA "is unclear and difficult for some plan sponsors to follow." No surprise there. But it's demographics that trip people up.

"Stakeholders we interviewed generally said that plan sponsors had particular difficulty understanding how to account for plan demographics" when selecting a QDIA, the report said.

So what's the problem? The GAO found that this uncertainty "could lead some plan sponsors to make suboptimal choices when selecting a plan's default investment, and could have long-lasting negative effects on participants' retirement savings."

So what's the alternative? Turns out that survey respondents feel that "age should not be the sole determinant" for whether a QDIA is right for a plan.

As a result, the GAO is hoping that the DOL will "amend the QDIA regulations to require fiduciaries to document whether they had considered participant characteristics other than age when choosing a QDIA."

We agree wholeheartedly with the GAO's findings. There is no such thing as a one-size-fits-all glidepath, which is a large part of what makes choosing a QDIA such a challenge. But we also believe it's possible to make a smarter choice if you pick a plan's glidepath based on specific plan demographics—not just the participants' ages, but also their risk-tolerance levels, investment behaviors and savings rates.

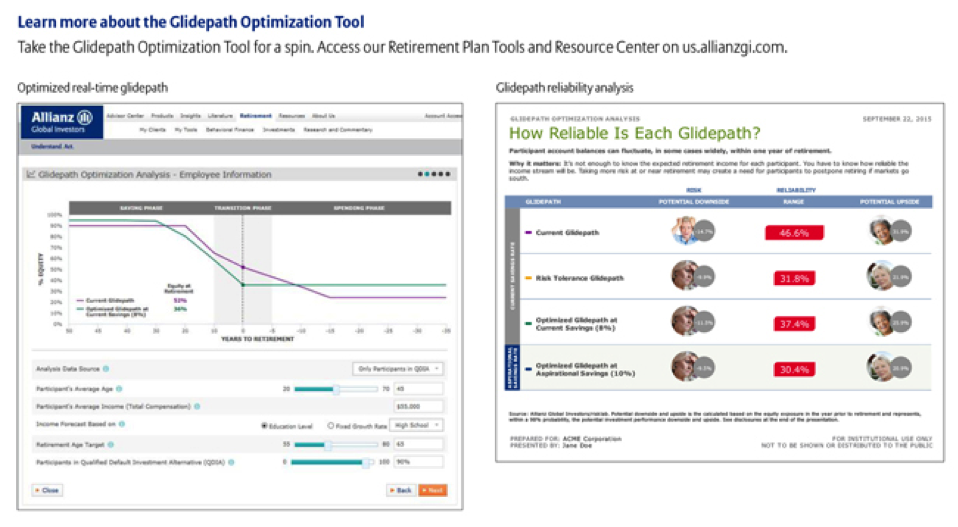

That's why we developed the first-of-its-kind Glidepath Optimization Tool, which seeks to fill the crucial void that the GAO identified in the standard QDIA selection process. Here's just a glimpse at what our Glidepath Optimization Tool can do for your plan.

|

• |

Calculate optimized and risk-tolerance glidepaths using real plan demographics—including age, risk-tolerance levels, investment behaviors, savings rates, education levels and plan goals. |

|

• |

Compare optimized and risk-tolerance glidepaths with the plan's current glidepath. |

|

• |

Document the target-date-fund selection process to help plan sponsors meet their fiduciary obligations. |

|

• |

Forecast the results, reliability and risk of each glidepath, and provide a customized list of target-date solutions that align with the chosen glidepath. |

Our Glidepath Optimization Tool was the result of years of development, but it couldn't have come at a better time. As the GAO report confirms, plan sponsors are becoming increasingly frustrated by trying to incorporate participant demographics into their QDIA selection process. That results in a big gap right at the heart of many plans. But the Glidepath Optimization Tool is here to help you fill that void.

Glenn Dial is Head of Retirement Strategy in the US with Allianz Global Investors, which he joined in 2011. He has 23 years of defined contribution experience. Mr. Dial is a co-inventor of the method and system for evaluating target-date funds, and is also credited with developing the target-date fund category system known as “to vs. through.”

Subscribe Today

Dialed In to Retirement is available as a subscription for financial professionals only. New issues will be delivered via email every month. Your email address must be in our records for your subscription to take effect.

The Glidepath Optimization charts above are provided for illustrative purposes only to provide examples of sample glidepaths and should not be considered a recommendation to purchase or sell any particular security or strategy.

Investing involves risk. The value of an investment and the income from it may fall as well as rise, and investors may not get back the full amount invested. Past performance is not indicative of future results. This document is being provided for informational purposes only and should not be considered investment advice or recommendations of any particular security, strategy or investment product. The information provided is for informational purposes only and investors should determine for themselves whether a particular service or product is suitable for their investment needs or should seek such professional advice for their particular situation. Statements concerning financial market trends are based on current market conditions, which will fluctuate. If presented, references to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Allianz Global Investors U.S. LLC (“AllianzGI U.S.”) is an SEC registered investment adviser that provides investment management and advisory services primarily to separate accounts of institutional clients and registered and unregistered investment funds. AllianzGI U.S. manages client portfolios (either directly or through model delivery and wrap fee programs) applying traditional and systematic processes across a variety of investment strategies. AllianzGI U.S. may also provide consulting and research services in connection with asset allocation and portfolio structure analytics. NFJ Investment Group LLC is an SEC registered investment adviser and wholly-owned subsidiary of AllianzGI U.S.

Allianz Global Investors U.S. LLC, 1633 Broadway, New York, NY 10019-7585, us.allianzgi.com, 1 800 926 4456.

AGI-2015-11-20-13826