As the dollar continues to move to multi-year highs, we are reminded that very few market moves matter as much as what happens to the reserve currency of the world. We have noted several times that a stronger dollar tends to be associated with lower profit margins (but higher US equity multiples), lower commodity prices, and lower emerging market equity prices.

We are now over 4+ years into the dollar’s move and the question facing investors currently is are we nearing the end of the dollar’s bull run? Based on a purchasing power parity basis, we would answer no, the dollar’s run is not over and in fact, may just be in the early innings of this stronger phase.

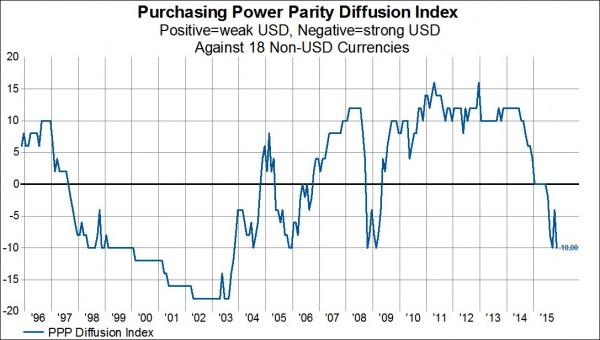

Purchasing power parity (PPP) models are terrible as a short-term market timing tool. The reason is that over-or-under valued trends can, and do, remain in place for years. So just because an undervalued currency is experiencing a six-month period of stronger performance, this doesn’t mean that a long-term trend change has taken place. However, the fact that trends remain in place for years is what makes PPP analysis useful for understanding the base case scenario for any currency trade. Because trends do not flip-flop very often, sustained trend changes are important as they most likely will remain in place for years to come. And over the past 17 months, there has been a significant trend change among almost all currencies in the world against the dollar.

For some historical background, the dollar was strong from mid 1997 to 2003. In August of 1997, nine out of the 18 currencies we track were considered overvalued on a PPP basis against the dollar and nine were considered undervalued on a PPP basis. By May 2002, all 18 currencies were considered undervalued against the dollar and this remained the case for nearly an entire year. From 2003 to 2008, there was a trend change in the dollar wherein by March 2008 15 out of the 18 currencies were overvalued against the dollar and only three were undervalued. Outside of some extreme moves during the financial crisis, this weak dollar environment remained in place until June 2014. Since June 2014, however, the trend has once again changed as of November 2015, 14 out of the 18 currencies are considered undervalued against the dollar while only four are considered overvalued. Many of these currencies that are now slightly undervalued against the dollar were extremely overvalued just a few years ago. Now that they have been undervalued for about a year or so, it seems that this undervalued trend may have several more years left before we see another major trend change in the dollar.

For example, the commodity currencies were some of the most overvalued against the dollar immediately after the financial crisis. The Aussie dollar was consistently 30-40% overvalued on a PPP basis from 2011-2013 and only in the last few months has it fallen to an undervalue level against the dollar. A similar story goes for the Loonie as well.

The Euro as overvalued against the dollar for most of the 2004-2014 period and only in the last year has it turned to an undervalue level against the dollar. It is now nearly 13% undervalued against the dollar which is basically the weakest level since 2002. The pound remains in its multi-year undervalued trend. The Swiss France has just (barely) moved into undervalued territory for the first time since 2010. It is too early to tell if this is a trend change in the Swiss Franc.

The Yen is nearly as undervalued as it has been over the past 20 years while the South Korean Won is about fairly valued. The Philippine Peso and the Singapore Dollar remain overvalued against the dollar. The Thailand Baht is right at fair value.