2016 will likely be a “Jekyll and Hyde” market. As financial advisors meet with their clients at or around the beginning of the new year, they should be mindful of these economic and market trends:

- The US economy is likely to slow next year. Although there will not be a recession in 2016, the economy is being weighed down by the following factors:

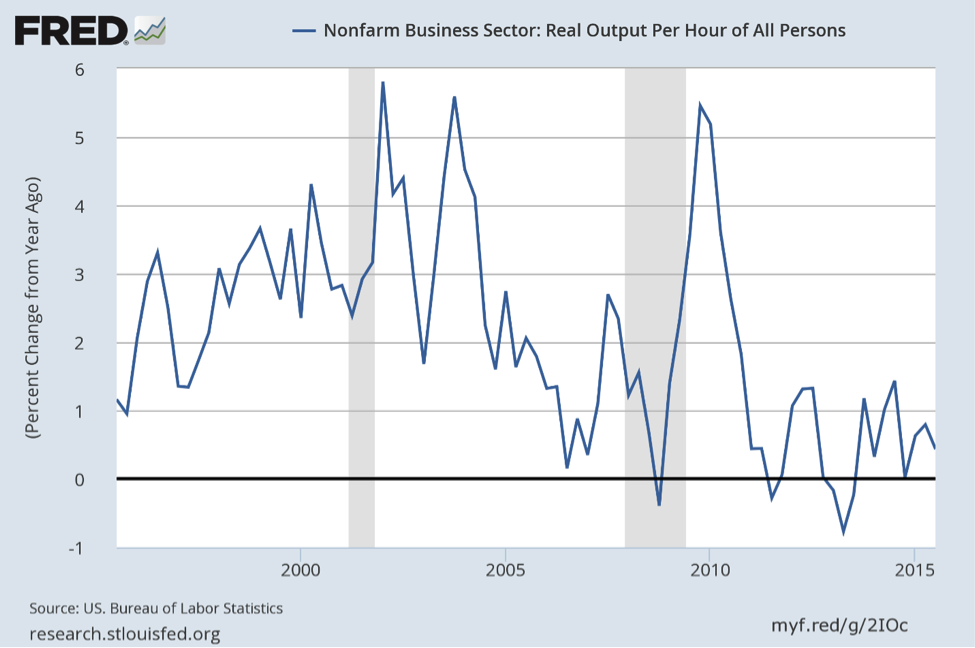

- Productivity growth continues to slow. As the graph below indicates, the annual growth in output per worker has declined from an average 3% in the 2000s to under 1% in recent years. Although demographics has some bearing on this slowdown, the lack of business technology spending growth coming out of the 2008-2009 recession has had its impact. Although technology growth has accelerated in 2015, it will take some time to see its impact on productivity numbers.

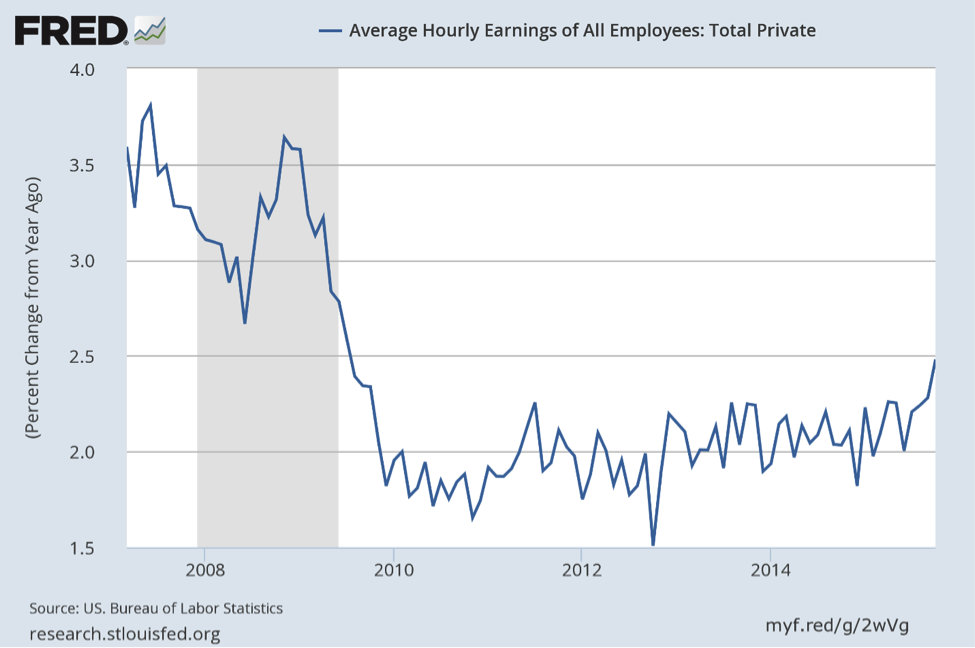

- Fortunately, wage growth has begun to accelerate although below the historical trend. Unfortunately, the labor force continues to rise at an anemic rate. Thus, total income growth has accrued to providers of capital that do not consume to the same extent as the typical worker. This reduces potential economic growth.

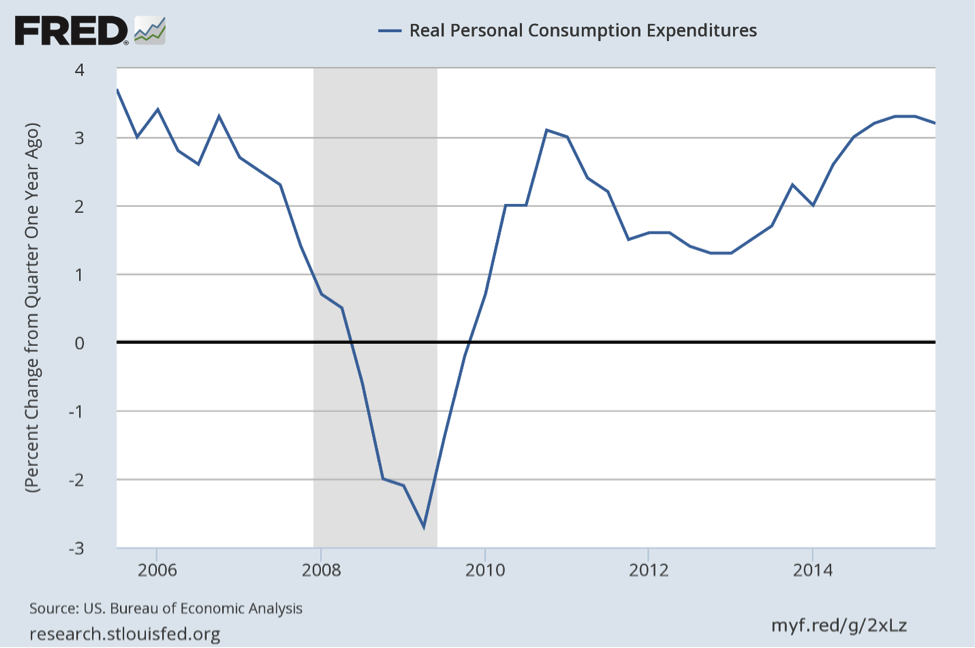

- The good news this year has been the increase in household consumption and its positive effects on the US gross domestic product numbers. As the chart below indicates personal consumption, adjusted for inflation has risen from the 1.5% level in 2013 to over 3.0% recently. Declining oil prices have aided this growth. The effect of lower oil prices on growth will wane throughout 2016 putting downward pressure on consumer expenditure growth.

- International economic growth has decelerated in 2015. Although European, Japanese and US economic growth increased this year, other Asian countries, commodity producing advanced countries such as Canada and Australia and emerging markets slowed. China’s declining economic growth had a deleterious effect across the globe. This has led central banks outside the US to generally keep rates low and, in some cases, provide further easing of monetary policies. This has given the US dollar a strong bid and increased the pressure on commodity prices. Although the dollar has increased 30% off of its 2011 lows, history indicates, and the fundamentals support, a potential 20% further increase from current levels.

- US equity market will continue to move in a wide trading range at the beginning of the year. The current earnings recession and uncertainty in the pace of Federal Reserve increases will put pressure on equity returns in 2015’s 2016’s first half. The market will recover in the second half when it becomes clear that the Fed will be raising rates at a very slow pace and global growth recovers. Select sectors will benefit from later cycle growth factors:

- Financial companies are seeing a rebound in demand as consumers’ balance sheets are being repaired and demand for business investment has increased.

- Technology spending is a prime beneficiary of lending growth. Both consumers and businesses are accelerating replacement and upgrade purchases as confidence in the economy rises to normal levels.

- The biggest surprise in 2016 could be the bottom of the commodity cycle. Supply is starting to decline while demand could normalize if global growth accelerates towards the end of the year.

- Investors need to be on the lookout for the following events that may impact equities negatively:

- If the Federal Reserve continues to mismanage expectations as interest rates rise, investors will be nervous about the pace of increase. This can lead to stock price declines until the picture becomes clearer.

- If commodity (especially, oil) prices rebound unexpectedly, consumers may reduce current expenditures and focus on savings.

- Investor sentiment could turn negative due to a variety of geopolitical events that are unforeseen at the present time.

Recommendation: For the past few years, the phrase “be long or be wrong” summarizes the correct equity market stance. Even with the wobbly stock market in 2015, investors have benefitted from generally rising prices over the past three to five years. Although we are positive on equities over the long run, now is the time to decrease client portfolio risk and increase diversification. Advisor are counseled to recommend to their clients that half of their equity weightings be invested in a tactical allocation with an equity market benchmark. This will provide a baseline of exposure to the stock market that all investors should have while increasing and decreasing equity weightings based on the market’s outlook.

Recommendation: As indicated above, many clients are likely to have too strong of equity allocations since stocks has have been the best asset class to own over the past six years. To increase potential principal protection over the rocky market times ahead, we believe all portfolios should allocate to the following income strategies:

- Enhanced cash allocation – This strategy owns only short bonds (under 3 years to maturity.) The allocation should have capital preservation as the number one goal with a secondary objective of higher yields than cash equivalent securities.

- Conservatively invested balanced allocation – This strategy will own mainly high quality intermediate-term (under 10 years to maturity) bonds. A small allocation to a dividend-tilted equity portfolio for extra yield (higher than that of the Barclays Aggregate Index) could increase the portfolio’s return.

- Publicly-traded alternatives allocation – This strategy owns a group of exchange traded funds, mutual funds and other exchange-traded securities that are expected to create a return pattern that is different from that of the stock and bond markets. This adds diversification to the portfolio and can help smooth returns in volatile markets.

Since each client has different objectives and risk tolerances, it is difficult to create model portfolios that are applicable in every, or even, most cases. Financial advisors are responsible to take this information and determine the best investment program for each client. As a benchmark from which to start, an advisor with a client with moderate risk tolerance that has historically been invested in a 60% stock and 40% bond portfolio (minimum $500,000), may wish to consider the following allocation design:

- 30% - Strategic Broad Market Equity

- 30% - Tactical Allocation With Equity Benchmark

- 20% - Enhanced Cash Allocation

- 10% - Conservatively Invested Balanced Allocation

- 10% - Publicly-Traded Alternatives Allocation

Again, this portfolio should only serve as a guide for financial advisors.