US Bond Market Week in Review: Diverging Oil Price Predictions and Rising Junk Yields, Edition

One of the central debates occurring within the Fed regards the causation of current inflation weakness. Some, like Fed President Bullard and Chairman Yellen argue low oil prices are solely responsible for the weakness. Ohers like President Brainard and Chicago Fed President Evans see a more nuanced picture involving declining international trade negatively impacting a wide swath of commodity prices. Regardless, this week various organizations published stories to support and counter each argument. As for oil prices, Goldman Sachs sees oil prices at $20 in the next 12 months.

Goldman Sachs told clients that the increasing glut of oil on the global market has combined with mild weather from a freak El Nino this winter. The twin-effect could send prices plummeting to $20 a barrel, the so-called ‘cash cost’ that forces drillers to abandon production. “Risks of a sharp leg lower remain elevated,” it said.

.....

The US investment bank said the overall glut in the commodity markets may take another twelve months to clear. It cited ‘red flag’ signals on the Shanghai Future Exchange over recent days. Copper contracts point to “imminent weakening” in China’s ‘old economy’ of heavy industry and construction, it said.

In contrast, Ecstrat strategist Emad Mostaque, writing on the FT’s Alphaville argues prices will rise about $100 for two reasons: increased Middle Eastern tensions and solid demand. The ME situation hardly needs elaboration. Here are his thoughts on demand:

Demand is healthy, driven by China and the US in particular. High crack spreads have kept gasoline above $2.50 per gallon in the US, but as refineries come off heavy maintenance this could fall below $2.00 even if oil prices are flat, increasing demand. Chinese demand is likely to plateau but remain solid even as the economy rebalances and slows.

Both sides have ample merit.

However, assuming a broader swath of commodity price declines is the reason for weak inflation, a Fed rate hike might create additional problems:

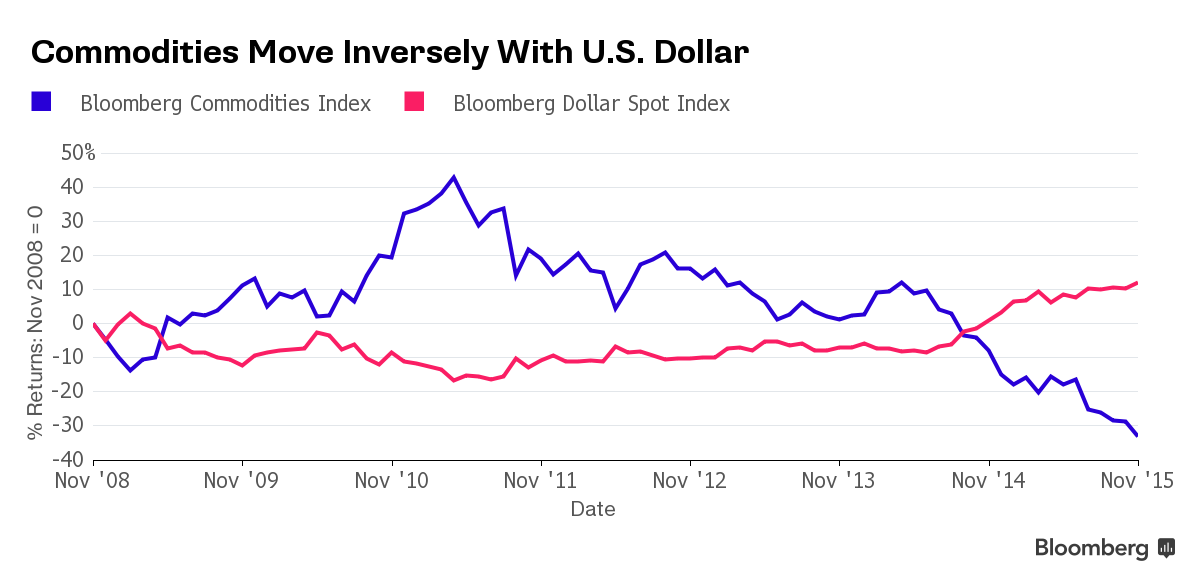

The first U.S. interest rate increase since 2006 is expected next month by a majority of investors, helping push the dollar up by about 9 percent against a basket of 10 major currencies this year. That only adds to the woes of commodities, mostly priced in dollars, by cutting the spending power of global raw-materials buyers and making other assets that generate yields such as bonds and equities more attractive for investors.

The story contained the following chart:

As with the oil arguments, we’ll have to wait and see to determine if this plays out.

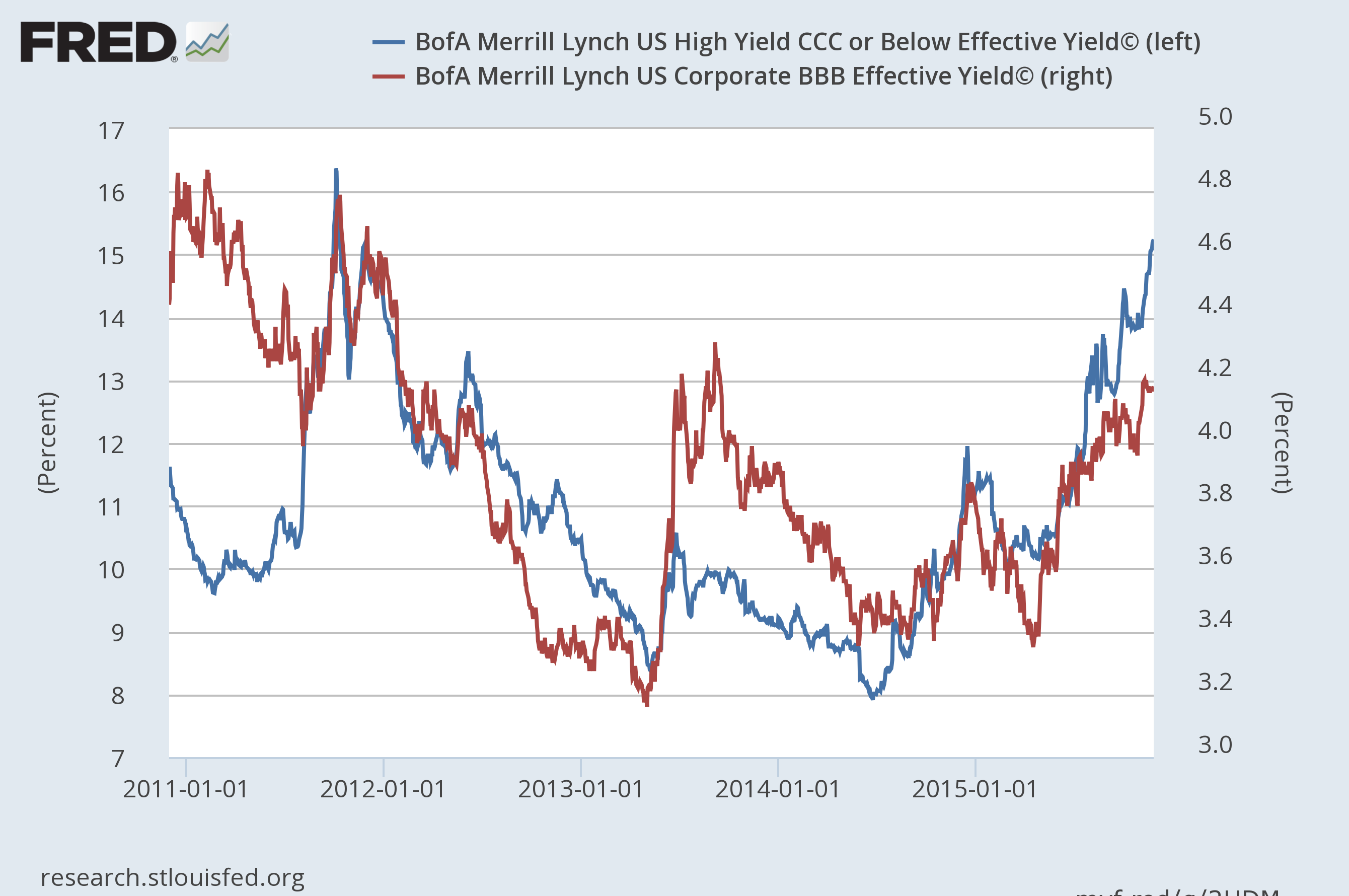

There’s been a second development in the bond market: yields of lower-rated securities are widening:

CCCs have blown out, rising from ~8% to 15% while the BBB market’s rise has been a bit more gradual, increasing from 3.4% to 4.2%. There are several reasons for these developments. First, thanks to low oil prices, there’s been an increase in oil company defaults:

A slide in oil and commodity prices has weighed on smaller energy producers, primarily in the US, as big Opec producers continue pumping crude to maintain market share. In the US, about three-fifths of defaults in 2015 have been among energy and natural resources businesses, including Midstates Petroleum, SandRidge Energy and Patriot Coal.

But this isn’t the only sector hurting; weakness is rising overall:

After six years of easy-money central-bank policies kept over-leveraged companies afloat and left scant opportunities for traders who profit off the market’s scrap heaps, a rout in commodities prices in 2014 presented what had seemed like a perfect chance to buy again. Instead, those prices only declined further this year, causing the debt of everyone from oil drillers to coal miners to fall deeper into distress. As the losses intensified, gun-shy investors pulled back from almost anything that smacked of risk, spreading the losses to industries from retail to technology.

And the losses may just be beginning; money managers are positioning themselves for the upcoming rate hike:

One by one, the giant investment funds are quietly switching out of government bonds, the most overpriced assets on the planet.

Nobody wants to be caught flat-footed if the latest surge in the global money supply finally catches fire and ignites reflation, closing the chapter on our strange Lost Decade of secular stagnation.

The Norwegian Pension Fund, the world's top sovereign wealth fund, is rotating a chunk of its $860bn of assets into property in London, Paris, Berlin, Milan, New York, San Francisco and now Tokyo and East Asia."Every real estate investment deal we do is funded by sales of government bonds," says Yngve Slyngstad, the chief executive.

.....

The Swiss bank UBS - an even bigger player with $2 trillion under management - has issued its own gentle warning on bonds as the US Federal Reserve prepares to kick off the first global tightening cycle since 2004. UBS expects five rate rises by the end of next year, 60 points more than futures contracts, and enough to rattle debt markets still priced for an Ice Age.

This is hardly surprising. The Fed has telegraphed this hike for the last six months or more. It’s only natural for money managers to start preparing.

The rise in lower rated credits could be a harbinger of weaker economic growth in the next 12-18 months. Inverted BBB rates are a long-leading indicator; they usually turn up at least a year before a recession. Adding to that argument is the weakening corporate profits environment. However, the two other long leading indicators (building permits and M3) are still positive.