As investors anticipate the beginning of a new year, we at Invesco Fixed Income are anticipating a new phase in the credit cycle for several bond asset classes. In this post, I will highlight a few areas where we’re seeing substantial changes in asset classes’ fundamentals or operating environment. We believe these areas could influence the broader market in 2016.

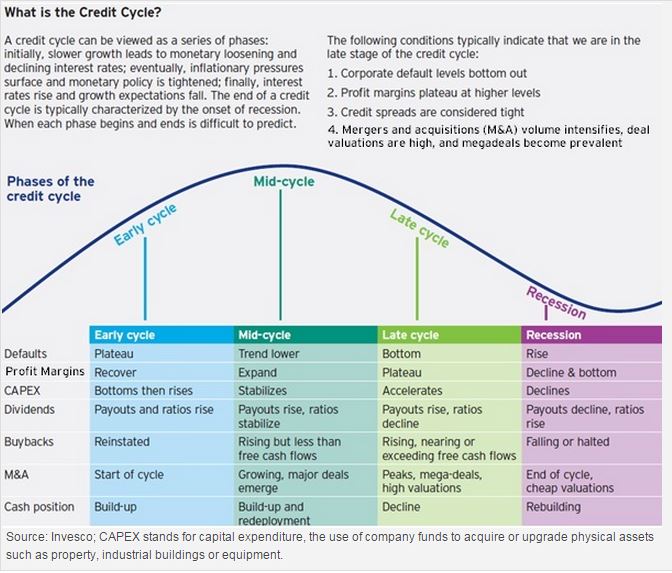

What is the credit cycle?

First, let’s briefly define what the credit cycle is. The credit cycle illustrates how easy, or how difficult, it is for borrowers to access credit. It’s driven by how companies are behaving toward their creditors, and how fundamental credit metrics are evolving.

The credit cycle moves in phases as monetary policy, interest rates and economic growth change over time. It’s important to note that the credit cycle is different from the economic cycle, but they’re related as the level and pace of credit creation is a key factor in economic growth.

Where are we in the credit cycle?

For most fixed income asset classes, the cycle has continued to advance toward the late cycle phase. Here are some notable highlights of markets in transition:

US investment grade. We see growing signs that US investment grade companies are in the late stages of the credit cycle. These signs include a significant level of merger and acquisition activity (especially in technology and health care), rising leverage, aggressive dividend payouts to shareholders, and a drift toward lower credit ratings. Up to this point, these have been balanced by a very low cost of funding and continued investor demand for the asset class.

In 2016, we expect to see new investment grade issuance as a result of M&A acquisition financing, shareholder payouts and regulations intended to strengthen global financial institutions. However, we expect these periodic supply pressures will create tactical opportunities in the current environment. For M&A situations, we prefer to invest in bonds that are issued after the transaction is finalized, when we can thoroughly study the deal’s size, the liquidity, deal concessions and other factors.

Emerging markets (EM). Another market at an inflection point is EM, where the growth and operating environment is putting pressure on fundamentals, and corporations are managing the downturn with more defensive behavior such as reducing costs, managing down debt and limiting dividend payouts to shareholders. We’re seeing classic end-of-cycle characteristics such as rising defaults and restructurings, as weakness in cash flows is increasing debt service burdens. We’ve also seen a decline in issuance as both investor and issuer appetite has waned. As is typical of EM, there is divergence between regions such as EM Europe and Latin America. In Asia, there’s growing divergence between onshore and offshore China.

Given the challenging external environment and continued commodity pressures, we expect to see a more modest level of new EM issuance in 2016 relative to recent years, which would help support the asset class. As mentioned, however, EM is notoriously difficult to paint with a broad brush, and that will again be true in 2016 with the fundamental situations in Eastern Europe relatively more constructive than in Latin America. We are focused on finding bottom-up opportunities in an environment of political instability and increasing asset price volatility.

High yield corporates. We are also monitoring the conditions of high yield corporates. We believe this asset class is marching towards late cycle phase, with financial conservatism fading and looming restructurings in parts of the commodity complex.

We continue to expect high yield to be a tale of two markets in 2016, between global commodity-related firms and those that are mostly exposed to the US, where the expected growth trajectory is slow but steady. Fundamental pressures in the commodity-related sectors will likely lead to higher default rates for the asset class, in our view, but the market is increasingly pricing in such a potential outcome. Outside of the commodity sectors, we maintain a more optimistic view of the high yield asset class given a relatively more positive fundamental outlook, albeit balanced by our expectations of higher volatility in the asset class triggered by expected changes in Fed policy.

Important information

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

The risks of investing in securities of foreign issuers, including emerging market issuers, can include fluctuations in foreign currencies, political and economic instability, and foreign taxation issues.

High yield bonds involve a greater risk of default or price changes due to changes in the issuer’s credit quality. The values of high yield bonds fluctuate more than those of high quality bonds and can decline significantly over short time periods.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s retail products and collective trust funds. Invesco Advisers, Inc. and other affiliated investment advisers mentioned provide investment advisory services and do not sell securities. Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc., and broker-dealers including Invesco Distributors, Inc. PowerShares® is a registered trademark of Invesco PowerShares Capital Management LLC (Invesco PowerShares). Each entity is an indirect, wholly owned subsidiary of Invesco Ltd.

©2015 Invesco Ltd. All rights reserved.

What is the credit cycle telling us about 2016? by Invesco Blog