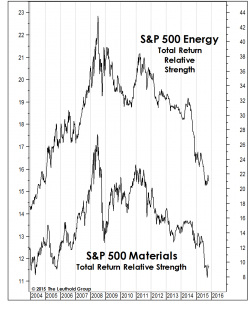

Commodities and commodity stocks have been a disaster in recent years, but fortunately one that our Group Selection (GS) Scores managed to avoid. Underperformance in both the Energy and Materials sectors during the last 12 months in particular (Chart 1) is so severe that any contrarian with a pulse probably can’t help but take a peek. We’ll admit the wreckage is beginning to look interesting, and—what with our cautious stance on the stock market—it would be fun to be bullish about something. But both our GS Scores and our intuition suggest it’s still too early.

Chart 1

The Select Industries Portfolio holds the only commodity-oriented group that’s currently eligible for purchase (rated Attractive)—Oil & Gas Refining & Marketing. None of the remaining Energy and Materials groups rates better than Neutral (Table 1), but we wouldn’t be surprised to see some upgrades in the next several months. We pulled together this piece as preparation for that possibility.

Table 1

Overstimulated?

Commodities certainly haven’t fallen for lack of stimulus. For nearly seven years, anywhere from one to three major central banks pumped out so much liquidity that it should have—on the surface—been bullish for commodities (and from late 2008 through early 2011, it was).

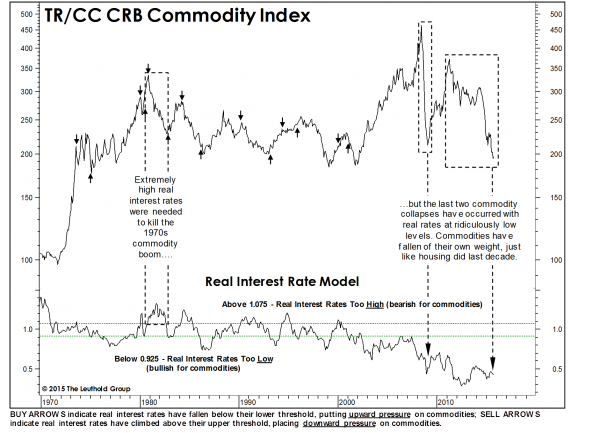

Chart 2

Is there such a thing as too much stimulus? Commodity market action in recent years would seem to say so. While low rates are obviously intended to stimulate demand, policymakers (and investors) have probably underappreciated the extent to which the same rates have allowed economically borderline supply to remain in place, particularly in the few sectors where capital spending has boomed in recent years (i.e., Energy and Materials).

· Excessive policy stimulus may help explain the failure of a Real Interest Rate Model we once found helpful in identifying cyclical swings in commodities (Chart 2). For years, commodities tended to respond to changes in real long-term interest rates, with “buy” signals triggered by a decline in real rates below a certain threshold and “sell” signals triggered by a rise in real rates. The model’s last “buy” signal occurred in December 2000, about 10 months in advance of the great 2001-2008 secular bull in commodities. The problem is that there was never a subsequent “sell” signal. Real interest rates have remained incredibly low, spending the last 14 years in a zone that had previously been reliably bullish for commodities. But all of this supposed liquidity failed to prevent two historic commodity busts (2008-09 and 2011-to-date).

· What should we make of the model’s breakdown? Counter to its original logic, a rise towards normalcy in real interest rates might actually prove bullish for commodities if it finally drives marginal drillers/miners out of business.

Capacity Overhang?

Beyond the generally bearish stance of our GS Scores, we’ve long worried about supply-side excesses among the commodity producers. Following the near-vertical recovery in commodities from 2009 to the spring of 2011, capex-to-depreciation (C/D) ratios for the Leuthold Materials sector actually exceeded the levels associated with the peak of last decade’s boom. But the sector composite C/D ratio has now trended downward for three years, recently undercutting the lows it made in the late 1980s and mid-1990s.

· While these capital spending trends have certainly contributed to our understanding of recent commodity cycles, they’re of limited use in helping us pinpoint any turnaround in commodity prices. Note that prices have reliably led the C/D ratio by about 12 to 18 months over the past 30 years (Chart 3). Given the recent path in commodities, any rebound in capex in the next year is unlikely.

· The relationship between oil prices and Energy sector capex is nearly identical, with prices again leading the sector capex-to-depreciation by 12 to 18 months (Chart 4). Given the 60% collapse in crude, we’d have expected more aggressive spending cuts than what’s occurred to date. But, based on recent history, those cuts are imminent—and prices should trough well before the C/D ratio hits bottom.

Commodity Stocks & “Real” Commodity Prices

Analysis of inflation-adjusted commodity prices proved helpful last decade when we were heavily invested in the industrial metals, and the same approach yields insight into this decade’s decline.

· Oil’s 2011-2013 trading range of roughly $90 to $110 per barrel, was (with hindsight) exceptionally high on a CPI-adjusted basis, and helps explain why Energy capital spending went through the roof. But crude’s latest decline finally pulled the real crude oil price below its 1973-to-date median (Chart 5). While the collapse must feel like an overshoot to anyone connected with the industry, the inflation-adjusted crude oil price has never approached the washed-out levels recorded twice during the 1980s and throughout much of the 1990s.

· The “real” oil price might seem like a largely academic concept. But Chart 6 shows the crude/CPI ratio has in fact moved in virtual lockstep with the Energy sector’s relative performance for the past 45 years, with a stunning correlation coefficient of +0.86. There’s unlikely to be a major sector rebound without higher oil prices, and vice versa.

· Equity analysts frequently refrain from making directional bets on underlying commodity prices. But even in the Materials sector—where the diversity of output is far greater than in the Energy patch—a directional bet is essentially implied:Relative performance of the S&P 500 Materials sector has tracked the inflation-adjusted CRB Raw Industrials with a correlation of +0.81 over the last 60 years. The sector is unlikely to recover without a strong upturn in the underlying commodities (Chart 7).

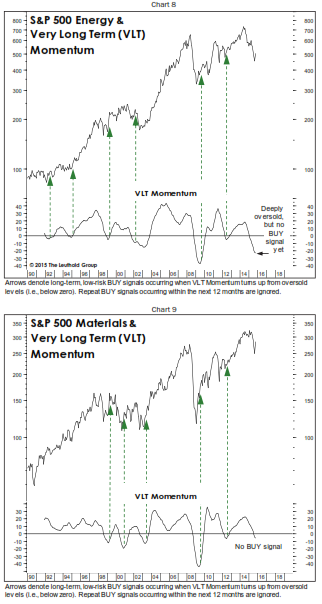

Commodity Sectors: A Long-Term Technical View

· We noted in this month’s “Inside The Stock Market” section that our VLT Momentum algorithm triggered a long-term BUY signal on crude oil at the end of October. The same discipline, though, failed to issue a bullish signal for the S&P 500 Energy sector (Chart 8). VLT is one of the components in our industry-level GS Scores, but its record on the broader sectors has been mixed. Note, for example, VLT’s misfire on the Energy stocks in 2002. On the other hand, the BUY signal from the summer of 2012 was excellent.

· The S&P 500 Materials sector is nowhere near as oversold as the Energy sector, but as shown in Chart 9, VLT also failed to trigger a new BUY in October. Again, though, the 25-year performance of VLT on the Materials sector has been mixed, with only five signals to evaluate. We’d rate the 2003 and 2012 BUY signals excellent, the 2009 signal good, and the 1999 and 2000 signals poor. But we’ll certainly pay attention if VLT turns up in the months ahead.

Commodities And The CPI-PPI Spread

The commodity collapse has obviously benefited the cost structures of virtually all industries within the Consumer Discretionary and Consumer Staples sectors. For decades, we’ve monitored the spread between Consumer Price Inflation and Producer Price Inflation as a proxy for the relative pricing power of consumer goods versus commodity producers.

· While consumer goods firms possess, in the aggregate, essentially no pricing power (with the CPI inflation rate near zero), that remains a relatively better situation than in the commodity sectors (where prices have fallen more than 8% in the last 12 months, based on the PPI-All Commodities). The only CPI-PPI gaps larger than today’s (Chart 10) were recorded in 1938 and 2008-2009—i.e., during severe economic declines.

· While not a perfect tool, its 85-year record suggests the CPI-PPI spread has been helpful in setting the allocation mix between consumer goods stocks (Consumer Discretionary & Staples) and commodity stocks (Energy & Materials). This is yet another tool suggesting it’s too early to plunge into the commodity sector (Table 2).

Table 2

Commodities: Miscellaneous...

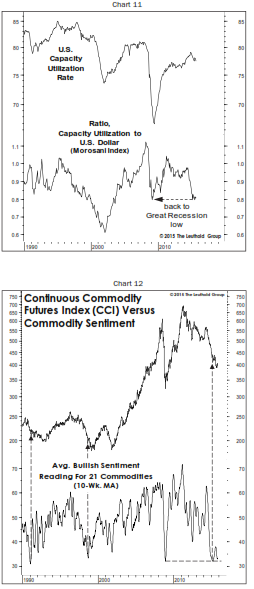

While the labor market may be approaching full employment, the same can’t be said for “capital” employment. The total industry capitalization utilization rate remains several percentage points below the level typically seen late in an economic expansion. The picture of excess slack is even more dramatic when utilization rates are divided by the value of the U.S. Dollar Index—an adjustment recommended by former C.J. Lawrence economist John Morosani (Chart 11). The dollar’s 17-month rally has driven the Morosani Index to levels last seen at the 2009 recession trough. Put another way, the dollar’s surge provides manufacturers with cheap access to foreign excess capacity, reducing the “effective” domestic capacity utilization rate.

We’ll wind up this piece with a ray of hope for commodity bulls in Chart 12: Commodity sentiment certainly looks fully washed out, with the average Bullish Consensus reading across a basket of 21 commodities nearing its Great Recession low. Sentiment extremes can occasionally pinpoint precise market turning points—like the CCI low of late 2008 or the spring tops of 2011 and 2014. But sentiment extremes precede extremes in price just as often. The trough in commodity sentiment reached during 1990-91 preceded the ultimate low in commodity prices by about 18 months, while the fall 1998 sentiment low was made several months before the commodity price low. And the extreme low in commodity sentiment, recorded early in 2015, has obviously been followed by even lower lows in prices. But prior sentiment extremes were eventually followed by a major reversal…

© 2015 Leuthold Weeden Capital Management. www.leutholdfunds.com