Editor’s note: We are publishing early this week in advance of Thanksgiving weekend here in the United States. For those celebrating with us, our best wishes for a warm holiday with friends and family.

With December just around the corner, awards for full-year achievement are beginning to come out. Sport, politics and the arts are recognizing those who reached the highest heights in 2015.

There is no trophy given for outstanding achievement in financial policy. And even if there were, it would not be a rival for the Ballon d’Or or the Palme d’Or in the public consciousness. Nonetheless, Mario Draghi deserves significant acclaim for the work he has done as president of the European Central Bank (ECB) in 2015. He is, arguably, the economic man of the year.

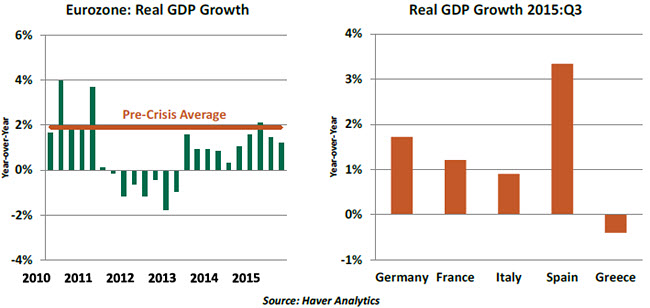

Late last year, many feared the potential “Japanification” of Europe. The Continent was suffering from a damaged banking system, an aging population and high levels of unemployment in most countries. The gap between actual and potential growth in gross domestic product (GDP) was still widening, six years after the onset of the financial crisis.

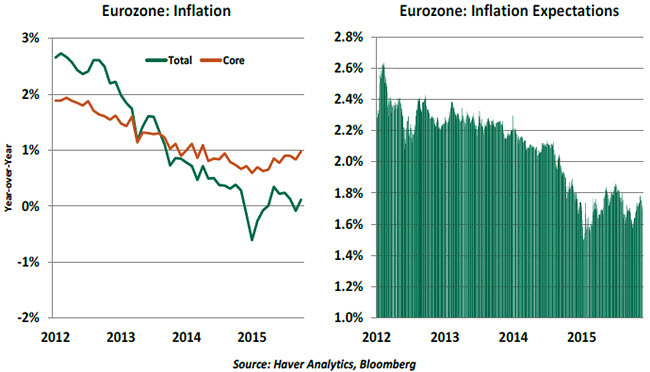

This was all reflected in a falling inflation rate, and diminishing inflation expectations. Once entrenched, these conditions are very difficult to dislodge; they are a central banker’s worst nightmare. To combat this outcome, the ECB had brought rates down to very low levels, but policy was clearly limited by the zero lower bound.

Quantitative easing (QE) had been suggested for quite some time in Europe, but many resisted it. There was skepticism over whether it would work; QE has shown mixed results in the United States and the United Kingdom, with early rounds having more of an impact and later rounds more effete. Japan continues to press ahead with the largest QE program in the world (in relation to its GDP), with only modest effect to date.

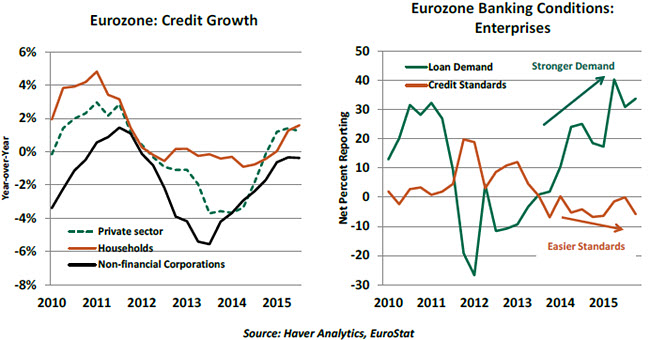

The structure of Europe’s credit system argued against QE. Most borrowers in Europe get the capital they need from banks, and not the financial markets. (QE programs have the most effect when the opposite is true.) And eurozone banks had been conserving capital by limiting the growth of their balance sheets, restricting credit at a time when more was needed.

As conditions worsened, Draghi worked hard to fulfill his pledge “to do whatever it takes.” He worked tirelessly to bring his governing council on board with the idea of QE, and his staff worked out the intricate details of which assets to buy and who would bear the risk of any underperformance. Finally, in mid-January, Draghi delivered a program that was larger than expected, gaining some psychological points from investors.

Quantitative easing works in mysterious ways. As we discussed in our October 16 commentary, QE programs encourage risk taking by making safe assets less attractive; the resulting capital flows provide money for investment and can create wealth effects that augment consumption. Since mid-January, European equities are up by 14%, and consumption is growing at its fastest pace since 2008.  The road to improvement reached a fork in the middle of the year, as Greece teetered on the brink of exit from the eurozone. Some parties to the negotiations thought that the Greeks should be excused, but Draghi argued forcefully for keeping Greece in the fold. (That took on a literal meaning during a late night meeting in July, when Draghi reportedly engaged in a shouting match with German Finance Minister Wolfgang Schäuble.)

The road to improvement reached a fork in the middle of the year, as Greece teetered on the brink of exit from the eurozone. Some parties to the negotiations thought that the Greeks should be excused, but Draghi argued forcefully for keeping Greece in the fold. (That took on a literal meaning during a late night meeting in July, when Draghi reportedly engaged in a shouting match with German Finance Minister Wolfgang Schäuble.)

Draghi put a lot of the ECB’s money at risk to support Greece, at great personal risk. But in the aftermath, Draghi has been hailed for acting in the best interest of all of the eurozone’s members. He is a leading European, transcending the parochial politics of individual countries.

But job well done is not mission accomplished…far from it. Inflation readings from the eurozone are still well below the ECB’s objective, even after adjusting for recent declines in energy and commodities prices. And while growth seems to have been re-established in the eurozone, it is far from robust. The area exports considerable amounts to China and other emerging markets where growth has moderated.

The longer that Europe remains mired in underperformance, the more complicated the Continent’s politics will become. There are parties in many countries who are questioning whether the Eurosystem is the right one for them. With elections in Spain next month and governments in other countries struggling to stay the course, showing tangible results soon is critical for the ECB.

As the governing council gathers next week, it will give serious consideration to redoubling stimulus efforts. The ECB’s benchmark deposit rate, already slightly negative, may be made more so to encourage more bank lending. Other central banks have moved deeper into negative territory without initiating any apparent dislocations.

The ECB could also choose to increase and/or extend its quantitative easing program. Currently set at €60 billion of bond purchases monthly until September 2016, the effort has some room to enlarge. The challenge will be the relative dearth of eligible securities to buy; including new asset classes raises some additional issues of risk and appropriate allocations across countries.  Some additional steps were clearly hinted at during the October ECB meeting. With the Federal Reserve stepping up its rhetoric in support of a rate hike next month, the euro has once again lost ground to the U.S. dollar. Some analysts expect this exchange rate to touch parity before too long, an outcome that would be beneficial for European exports.

Some additional steps were clearly hinted at during the October ECB meeting. With the Federal Reserve stepping up its rhetoric in support of a rate hike next month, the euro has once again lost ground to the U.S. dollar. Some analysts expect this exchange rate to touch parity before too long, an outcome that would be beneficial for European exports.

The ECB was late in applying the level of stimulus needed to facilitate its objectives. Europe faced hindrances that other areas did not: a sovereign debt crisis in peripheral countries and austerity measures in core countries that held back economic growth. And growth was uneven, which made achieving consensus difficult. But if the eurozone is to catch up to other centers, policy must remain aggressive.

Mario Draghi has proven to be a great communicator. His phrasing at press conferences steers the media and the markets with skill. He takes every opportunity to remind his audiences that there is only so much that the ECB can do in the absence of structural reform to make Europe’s economies more flexible. He even composed himself and carried on after a protestor interrupted his April presentation.

But the skeptics he fears most are not young activists who are critical of the ECB’s power, but rather the 335 million eurozone residents that are anxious for better times. With each decision and dictum carefully scrutinized, Mr. Draghi will have to stay at the top of his game if he hopes to retain the award we have bestowed upon him. We wish him well, because his success will mean success for all of us.