In business and economics, a “first-mover advantage” is defined as the benefit accrued to a company whose product is the first to enter a market. These products often create or define an entirely new market opportunity that the world hadn’t known before. Some “first-mover” examples have created very attractive long-duration opportunities. EBAY (EBAY), a company we own in our portfolios, was the first online auction service. It has maintained leadership in that area for the last two decades. Kleenex was a first-mover in the facial tissues market, and has become so common that most people don’t know what a facial tissue is without saying the product name. A prime first-mover example is Coca-Cola, which created its soda pop market in 1896 and continues to dominate it 120 years later.

Examples like these give credence to the idea that the early bird indeed catches the worm. The notion has become more powerful as you consider the massive ego and financial benefits of being the next Elon Musk or Jeff Bezos. The possibility of relatively immediate notoriety and wealth has not been lost on private equity investors. It is estimated that private equity firms sit on more than $1.2 trillion of cash that is waiting in the wings to find those kind of attractive targets. When looking at the cash plus advantage that private equity firms can apply towards deal making, it has never been higher than today. Private equity deals of today are done at very rich multiples. EBITDA and net income multiples of 6x and 21x higher than the S&P 500 are typical. This all sounds very exciting to us. It brings to mind something Warren Buffett says, “Investors should remember that excitement and expense are their enemies.”

At Smead Capital Management, we like companies who have a long history of profitability and strong operating metrics. With very few exceptions, we will not consider a company where we can’t find at least 7-10 years of history in the public markets. We like businesses that have very wide moats (defensible positions) around their products and services. We like products that are so ubiquitous that they are associated with categories or industries. We think Aflac (AFL), H&R Block (HRB), and Disney (DIS) are nearly inseparable to concepts like supplemental health insurance, taxes, and wholesome family entertainment. Brand identity and awareness of these sorts translate to very strong and durational business value. We know this sounds substantially more boring than what goes through the blood of those who believe there’s “gold in them thar hills.”

There may be gold, but most of the real world stories told around the campfire of first-movers are laden with pain and destruction. After all, was it really helpful to be the first-mover in online search (AltaVista / Infoseek), video-tape (Betamax), cellular phones (Blackberry / Motorola), social networking (MySpace), new grocery delivery systems (Webvan), or new and innovative ways of transportation (Segway)? Especially in a world where most innovation efforts are geared towards the technology sector, an area that can be defined by disruptive innovation, we at Smead Capital Management don’t think so. What we find exciting is attempting to understand how our portfolio of companies may be able to leverage brands and products using newer technologies that will extend awareness and increase interaction. What kind of probability can we assign to the success of our companies gaining meaningful leverage from modern day innovation?

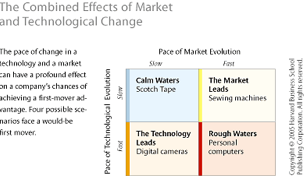

A Harvard Business Review article by Fernando Suarez and Gianvito Lanzolla gave us a very helpful framework to think about the concept of technological changes in relation market development.

Suarez and Lanzolla argue that maintaining a long lasting dominant position is most probable if the market and technological evolution is slow and stable. They use Scotch Tape as an example of “calm waters,” where being first to market has a high likelihood of durability. For calm water situations, even if technological innovation is attainable, the advantage is not large enough to disrupt or dislocate the core value proposition. The appeal and adoption of calm water products is also very gradual, giving ample time to organize production, distribution, and branding. Scotch Tape was originally intended for industrial use and, as the product developed just prior to the Great Depression, became widely used by individuals looking to repair household items that might otherwise be discarded. Its parent company, 3M, had plenty of time to build a strong and wide moat before full market adoption.

Nordstrom (JWN) began in 1901 as a humble shoe store, and began selling apparel in the early 1960’s. Starbucks (SBUX) has been selling an addictive legal drug for over 40 years, and H&B Block (HRB) began its campaign towards dominating the world of tax services just after WWII. Gannett (GCI) and News Corporation (NWSA) operate media franchises whose brands have been around for decades. Experts who are the most excited about the evolution of technology think these brands have far less relevancy in an on-demand era driven by digitization. We think these examples are calm water situations. The moats are very large, and the products and services have been developed over many years. The possibilities for innovative disruption are real, but in our opinion, far less likely to interrupt the value proposition of the brands themselves.

We think we can assign a reasonably high probability of success as these companies utilize innovation to extend brand awareness and reach. Nordstrom’s Direct (online) business has mushroomed from less than $500 million in 2006 to nearly $2 billion last year, but management speaks of this as just one important piece of its larger omni-channel strategy. It’s very complimentary to the core proposition, and greatly leverages what Nordstrom has done extraordinarily well for years. Starbucks has greatly enhanced the experience of its customers through innovation as well. Gannett and News Corporation are dealing with the challenge of applying technology to its core content offerings, causing the stocks to trade at deep discounts to intrinsic value. We believe they are very well positioned to leverage their brands in the digital world. News Corporation, with waterfront property brands like the Wall Street Journal and Barron’s (whose subscriber bases continue to grow), has highlighted the success it is having with digital migration in recent earnings calls. Similarly, we believe the content Gannett provides with its 5,000+ journalists will be relevant for years to come, and is set up to extend its brands digitally.

Calm water situations provide an essential buffer for a company to positively leverage the technological evolution, not be displaced by it. A wide moat affords a company the time necessary to properly assess the best strategy to position itself in new channels and venues. At Smead Capital Management, we don’t expect our companies to win every battle. We are very optimistic about how our companies are positioned to win wars, even as evolutionary change presents itself.

Warm Regards,

Tony Scherrer, CFA

The information contained in this missive represents SCM's opinions, and should not be construed as personalized or individualized investment advice. Past performance is no guarantee of future results. Tony Scherrer, CFA, Director of Research, wrote this article. It should not be assumed that investing in any securities mentioned above will or will not be profitable. A list of all recommendations made by Smead Capital Management within the past twelve month period is available upon request.

This Missive and others are available at www.smeadcap.com.

Follow us on Twitter @SmeadCap