The news continues to move in a bearish direction. Although the UK and Australia are in decent economic shape, neither country is setting growth records. And on the bearish side, Mario Draghi stated the EU recovery is weak and may need additional stimulus while Japan entered a technical recession for the second time in two years. And all this is occurring at time when the global growth juggernaut of China is slowing. Overall, the scales appear to be more and more tipped in a bearish direction.

Mario Draghi’s speech was the most important news from the EU this week. He noted three risks to the EU region:

First, the downside risks to our baseline scenario for the euro area economy have increased in recent months due to the deterioration of the external environment. The outlook for global demand, especially in emerging markets, has notably worsened, while uncertainty in financial markets has increased. Global growth this year will be the weakest since 2009.

Second, even factoring in those headwinds, the strength of the underlying recovery is modest. Taking the Purchasing Managers’ Index, the present upswing which started in 2013 is the weakest euro area rebound since 1998. That is striking considering that we are in the early phase of a recovery, where one would expect to see a much more vigorous pickup. Deferred spending typically comes back on stream in a bulky way, aided by more favourable financing conditions.

It is also striking considering the important tailwinds helping the economy along – not just our monetary stimulus, but lower prices for energy. None of those previous rebounds since 1998 could benefit from cheapening energy: in fact, oil prices have been a constant headwind blowing against previous recoveries. Moreover, in none of those previous upswings was monetary policy, measured by real EONIA rates, as supportive as it is now.

Third, the recovery remains very protracted in historical perspective. It took between five and eight quarters for the countries now making up the euro area to recover their pre-recession level of real output after the slumps of the 1970s, 1980s and 1990s. During the recent recession – which was admittedly the worst since the 1930s – it took the US economy 14 quarters to reach its pre-crisis peak. If our current assessment is correct, it will take the euro area 31 quarters to return to its pre-crisis level of output – that is, in 2016 Q1.

Exports have been an area of strength for the EU economy for the duration of the expansion; as a percent of GDP, they rose from .1% in 2010 to 2.1% in 2014. But weaker global economies obviously translates into lower trading volumes. Regarding overall growth, the EU region grew between a 2%-4% annual rate in the late 1990s and the latter part of the expansion ending in 2008. But growth during the current expansion is still below a 2% annual rate. This leads to his third point: weak growth means the length of time it has taken for the economy to return to previous levels has lengthened. This corroborates the impression of an overall period of economic weakness. Due to the increased downside potential, the ECB may increase stimulus:

We cannot say with confidence that the process of economic repair in the euro area is complete. At the December Governing Council meeting we will thoroughly assess the strength and persistence of the factors that are slowing the return of inflation towards 2%. If we conclude that the balance of risks to our medium-term price stability objective is skewed to the downside, we will act by using all the instruments available within our mandate. We consider the asset purchase programme to be a powerful and flexible instrument, as it can be adjusted in terms of size, composition or duration to achieve a more expansionary stance. The level of the deposit facility rate can also empower the transmission of APP, not least by increasing the velocity of circulation of bank reserves. If we decide that the current trajectory of our policy is not sufficient to achieve our objective, we will do what we must to raise inflation as quickly as possible. That is what our price stability mandate requires of us.

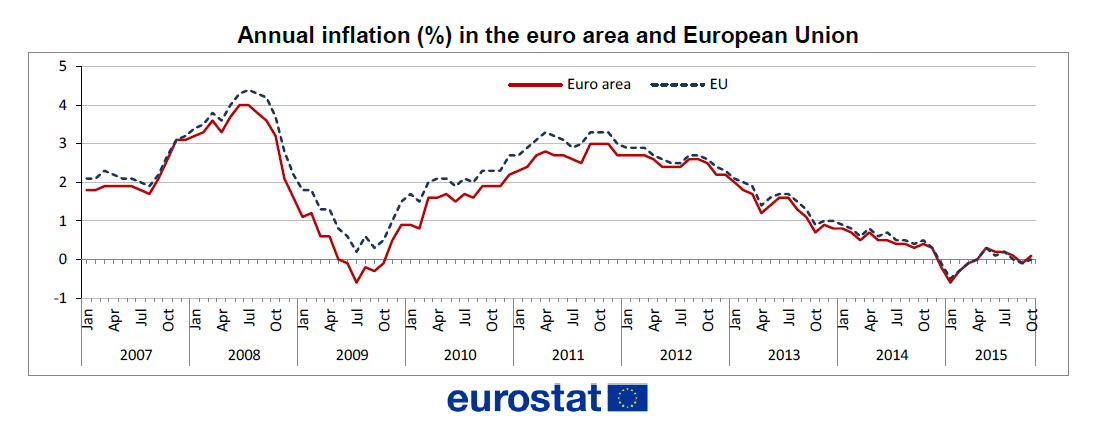

In no uncertain terms, Draghi again stated the ECB would to “whatever it takes” to reignite inflation and growth. This is fortunate, because the latest inflation number was .1% Y/Y, with core up 1.1%. This chart from the release shows total inflation hovering just above 0% for all of 2015:

The Bank of Japan maintained their current interest rate policy and asset purchase program, offering the following assessment of the economy:

Japan's economy has continued to recover moderately, although exports and production have been affected by the slowdown in emerging economies. Overseas economies -- mainly advanced economies -- have continued to grow at a moderate pace, despite the slowdown in emerging economies. Exports and industrial production have recently been more or less flat, due mainly to the effects of the slowdown in emerging economies. On the domestic demand side, business fixed investment has been on a moderate increasing trend as corporate profits have continued to improve markedly. Against the background of steady improvement in the employment and income situation, private consumption has been resilient and housing investment has been picking up. Public investment has entered a moderate declining trend, although it remains at a high level. Financial conditions are accommodative. On the price front, the year-on-year rate of change in the consumer price index (CPI, all items less fresh food) is about 0 percent. Inflation expectations appear to be rising on the whole from a somewhat longer-term perspective, although some indicators have recently shown relatively weak developments.

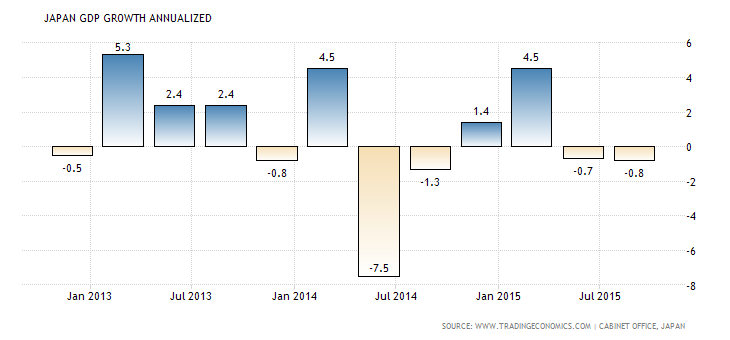

This assessment misses the mark, because Japan is in a recession for the second time in the last 4 years:

At some point, the Japanese government and BOJ need to come to grips with the deteriorating nature of the domestic economy.

The RBA released their latest policy minutes which offered the following assessment of the Australian economy:

Members observed that the Australian economy continued to grow in the September quarter as economic activity continued to shift away from mining investment to other sectors of the economy. Members noted that the forecasts for GDP growth were not materially different from those presented three months earlier. Growth was expected to be between 2–3 per cent over the year to June 2016, before rising to 2¾–3¾ per cent over the year to June 2017. The forecast for GDP growth towards the end of the forecast period had been revised down slightly to incorporate information about minor delays to the commencement of production at some large liquefied natural gas (LNG) projects.

They characterized the consumer, housing and service sector as expanding. Mining investment, however, continued to decline. Meanwhile, inflation was contained. Overall, Australia remains one of the best positioned developed economies.

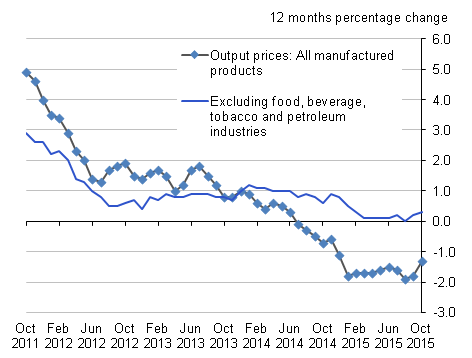

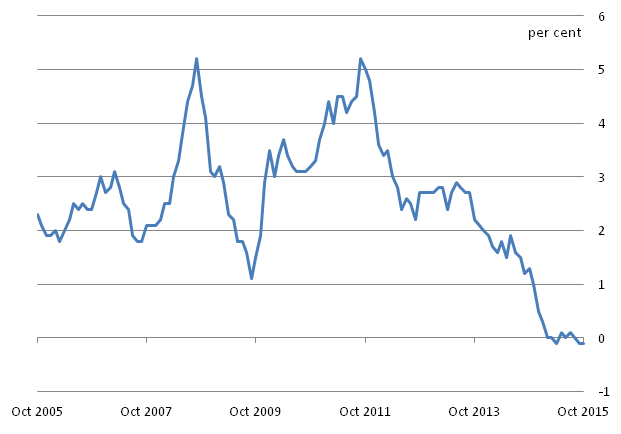

The Office of National Statistics released two UK statistics this week. Producer prices decreased 1.3% Y/Y while consumer prices declined .1%. The following charts (PPI and CPI, respectively) show a very weak price picture in the UK:

Finally, retail sales increased 3.8% Y/Y.

The UK, like Australia, remains in decent shape. But between China's transition, Japan's second recession and Draghi admitting the overall weakness of the EU economy, it appears the bearish tenor to the news is increasing.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis