KEY TAKEAWAYS

This week’s Fed meeting minutes may provide insight into the likelihood of a December rate hike.

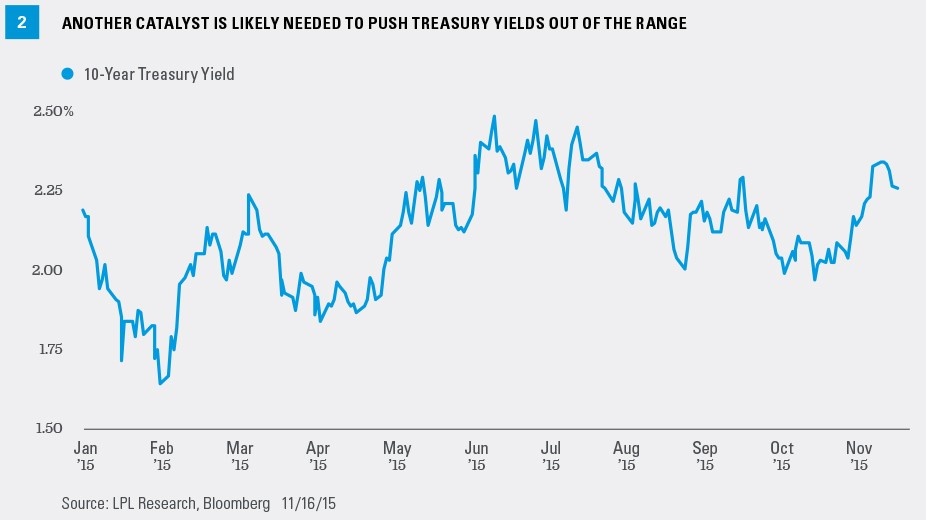

Another catalyst is likely needed to break bonds out of a broader range that has defined trading for the past several months.

The inverse correlation between stocks and high-quality bonds failed to hold over the past week, after holding for October 2015, suggesting other forces are at work. The answer to the bond market’s indifference to risk asset performance may lie in market fixation over a possible Federal Reserve (Fed) rate hike in December 2015. According to fed fund futures pricing, market expectations for the timing of the Fed’s first rate were essentially unchanged, with the probability of a December rate hike marginally lower on the week to 64% from 70%.

HOLDING FIRM

Fed speakers’ public remarks, notably Fed Chair Yellen and Vice Chairman Dudley, indicated that a slow pace of rate hikes is likely warranted given global challenges but that liftoff is still likely in December. They are holding firm to a possible December timeline, despite tepid domestic economic data last week and mixed results from China’s latest batch of economic data. Additionally, U.S. dollar strength (a driver of low inflation expectations and a support for high-quality bonds) persisted and oil prices dropped, raising default expectations in the high-yield bond market. The economic backdrop may have tempered investors’ longer-term growth expectations, but the Fed’s message kept investors focused on December as the likely liftoff for rate hikes.

CORPORATE ISSUANCE

When performance does not respond to fundamental drivers as expected, it may point to other market forces at work. Investment-grade corporate bond issuance remains heavy, with year-to-date 2015 new issuance running almost 15% greater than the 2014 pace and well on its way to a record year. When corporate issuance is robust, bond dealers often sell-short Treasuries as a hedge. By shorting Treasuries, dealers protect against price declines in the event a corporate bond deal takes longer to sell. The short Treasury position can help offset price declines on new issue corporate inventory. Short Treasury trades, or even bond traders anticipating new issuance-related Treasury selling, can influence prices and override the impact of fundamental news. Of course, the unwinding of these hedges can also push Treasury prices higher in the absence of fundamental data. For now, the continued surge in corporate new issuance, which includes a hefty $30 billion per week pace thus far in November, has proven a headwind for high-quality bonds. Over the past three years, investment-grade corporate bond issuance has averaged $20 billion per week.

A similar muted reaction by Treasuries occurred this past August as stock market volatility resulted in only a limited change in Treasury yields. In August, investors were also focused on the Fed and a potential rate increase at the September Federal Open Market Committee (FOMC) meeting.

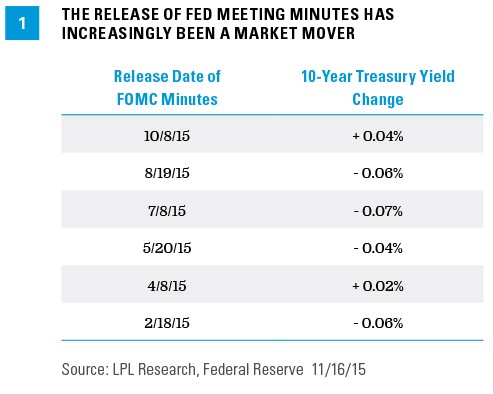

This week’s release of minutes from the October 27–28, 2015, FOMC meeting may be a focal point for the bond market in the absence of significant economic data. Investors will parse the minutes to fine-tune expectations around a potential December rate hike. The release of the Fed meeting minutes has increasingly been a market mover [Figure 1].

With the exception of the April 8 release, Treasury yields have experienced significant single-day moves on the release of Fed meeting minutes. Yields have more frequently declined rather than increased as the Fed has often deferred to a cautious go-slow approach. Even the September meeting minutes, released on October 8, 2015, were interpreted as dovish by the markets; but strength in more economically sensitive assets, stocks and high-yield bonds, pressured Treasuries.

CONCLUSION

The bond market appeared indifferent to a stock market pullback with only a modest rise in high-quality bond prices last week. High-yield bond prices weakened as well but also failed to spark any surge in Treasuries. Investor rotation to high-quality bonds as a protective measure did not materialize, as would often be the case when stocks and high-yield bonds decline by just over 3% and 1%, respectively.[1] Conversely, a 1.5% surge in stock prices on Monday, November 16, 2015, failed to generate a significant sell-off in U.S. Treasuries.

Focus on a December rate hike, which futures pricing shows as the most likely point for Fed liftoff, led to a muted reaction to stock market weakness last week. The release of the October Fed meeting minutes this week, the last full week of trading before the Thanksgiving holiday, may provide insight into the likelihood of a December rate hike, but it will likely take another catalyst to break the bonds out of a broader range that has defined trading for 2015 [Figure 2].

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate, and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

High-yield/junk bonds are not investment-grade securities, involve substantial risks, and generally should be part of the diversified portfolio of sophisticated investors.

Selling short can result in losses should the borrowed security increase in price, rather than decline. The theoretical potential loss is unlimited. Additionally, short sales will incur interest on the borrowed shares while also being subject to margin calls, or early sales in the event that the original owner wishes to sell their position.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Barclays U.S. Corporate High Yield Index measures the market of USD-denominated, noninvestment-grade, fixed-rate, taxable corporate bonds. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below, excluding emerging market debt.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 5296 1115 | Tracking #1-441093 (Exp. 11/16)

1 As measured by the S&P 500 Index and Barclays High-Yield Bond Index, respectively, from Nov. 6, 2015 through Nov 13, 2015.