Rising Rates? How About Some Inflation First?

Some pundits have expressed surprise the Fed did not raise rates in September, citing low unemployment and improving GDP numbers as evidence the Fed has gone too far with its dovish policies. Unfortunately, many market commentators gloss over the relationship between interest rates and inflation. HiddenLevers examined the effects of inflation in our End of Inflation webinar, and we have summarized some of our takeaways below.

The relationship of inflation and interest rates is a tenant of macro-economic theory. High inflation=high interest rates and conversely low inflation=low interest rates. This concept can be quickly illustrated by charting the yield of the 10-year T-Bill against CPI.

Those who had the pleasure of living through the stagflation of the late 1970s understand this relationship firsthand – high inflation comes with high borrowing costs, both of which fell in tandem when the Fed crushed inflation in the 1980s.

Disinflation Doldrums

What has caused our extended period of low inflation? First let’s recognize one of the principal drivers of inflation – wages. Unfortunately, wages have been stagnant since the 1990s and the trend was aggravated further in 2008 after a dramatic pruning and reorganization of jobs during the financial crisis. Top performers have been asked to take on more work and technology has disrupted entire industries, pushing wages downward and increasing efficiencies.

Commodity prices have also taken a hit. Technology has supplanted the emerging world’s thirst for crude and other commodities continue to fall in price.

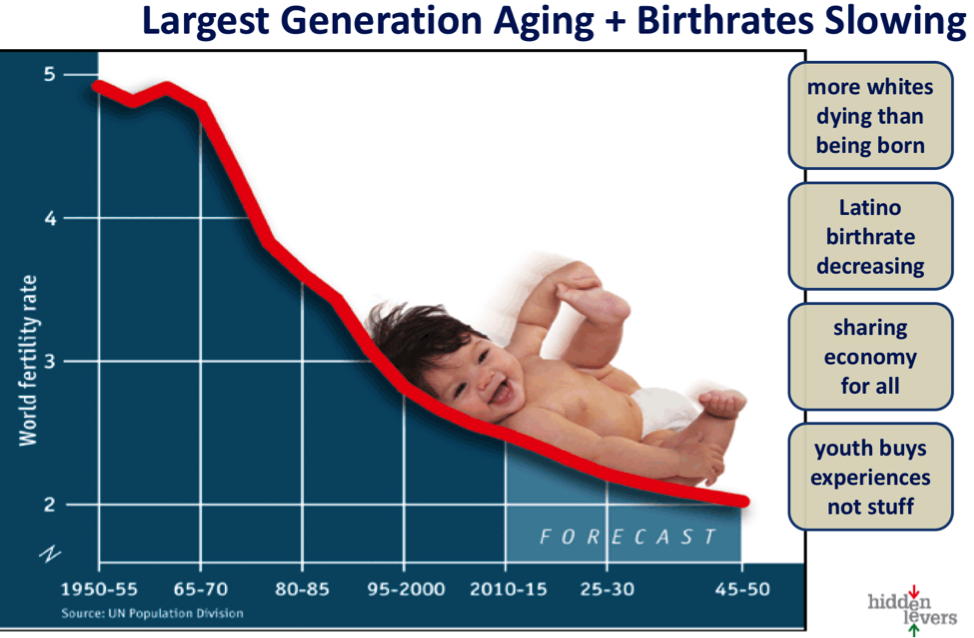

The Coming Demographics Dilemma

To add fuel to the fire, the global economy is following in Japan’s footsteps, with demographic trends working against the quest for economic growth.

The world’s fertility rate has been declining rapidly since the 1950s. Unfortunately, global policy makers have only exacerbated the problem by encouraging less fertility amongst couples. This has hoisted the costs of retirement onto a relatively small base on millennials and shifted spending solely towards the healthcare sector – one of the few industries to see a marked appreciation in costs over the past couple of decades.

No end in sight

It is anyone’s guess if the strength of disruptive technology and demographic trends will continue to defy the will of central banks. So what does this mean for your client’s portfolios? It is best to examine any portfolio under multiple lenses. Stress testing allows an advisor to simultaneously model what would happen if the US turns into Japan or if central banks decide to hike rates before the end of the year. Looking at both scenarios helps advisors better hedge against downside risks and set client expectations in both outcomes.