Last week, Fed President Rosengren offered his analysis of the US economy:

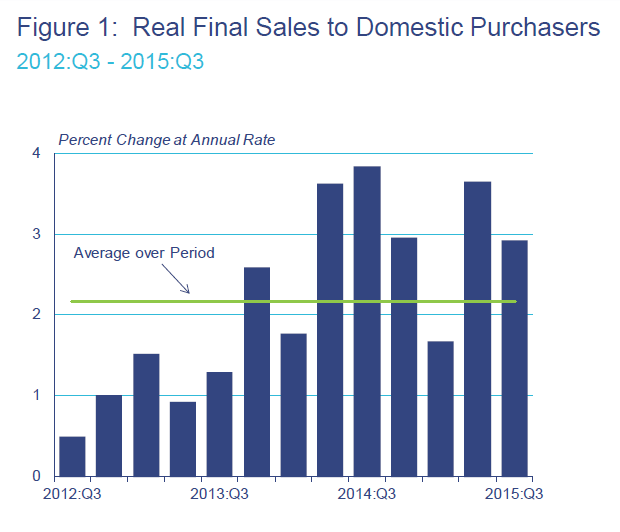

Many headlines have focused on real GDP growing at only 1.5 percent in the third quarter. However, I would like to share with you a measure that focuses on domestic demand – real final sales to domestic purchasers, which is shown in Figure 1. This statistic is similar to GDP, but excludes fluctuations in inventories and net exports. This leaves consumption, investment, and government spending – in sum, a measure that tries to capture the underlying strength in domestic demand. In the third quarter of this year, real final sales to domestic purchasers grew by 2.9 percent, following its second-quarter growth of 3.7 percent.

He offered the following chart:

As he notes, the five year average for this number is a little over 2%. Historically, this number is a bit weak, but still positive:

He then turned his focus to US consumer spending:

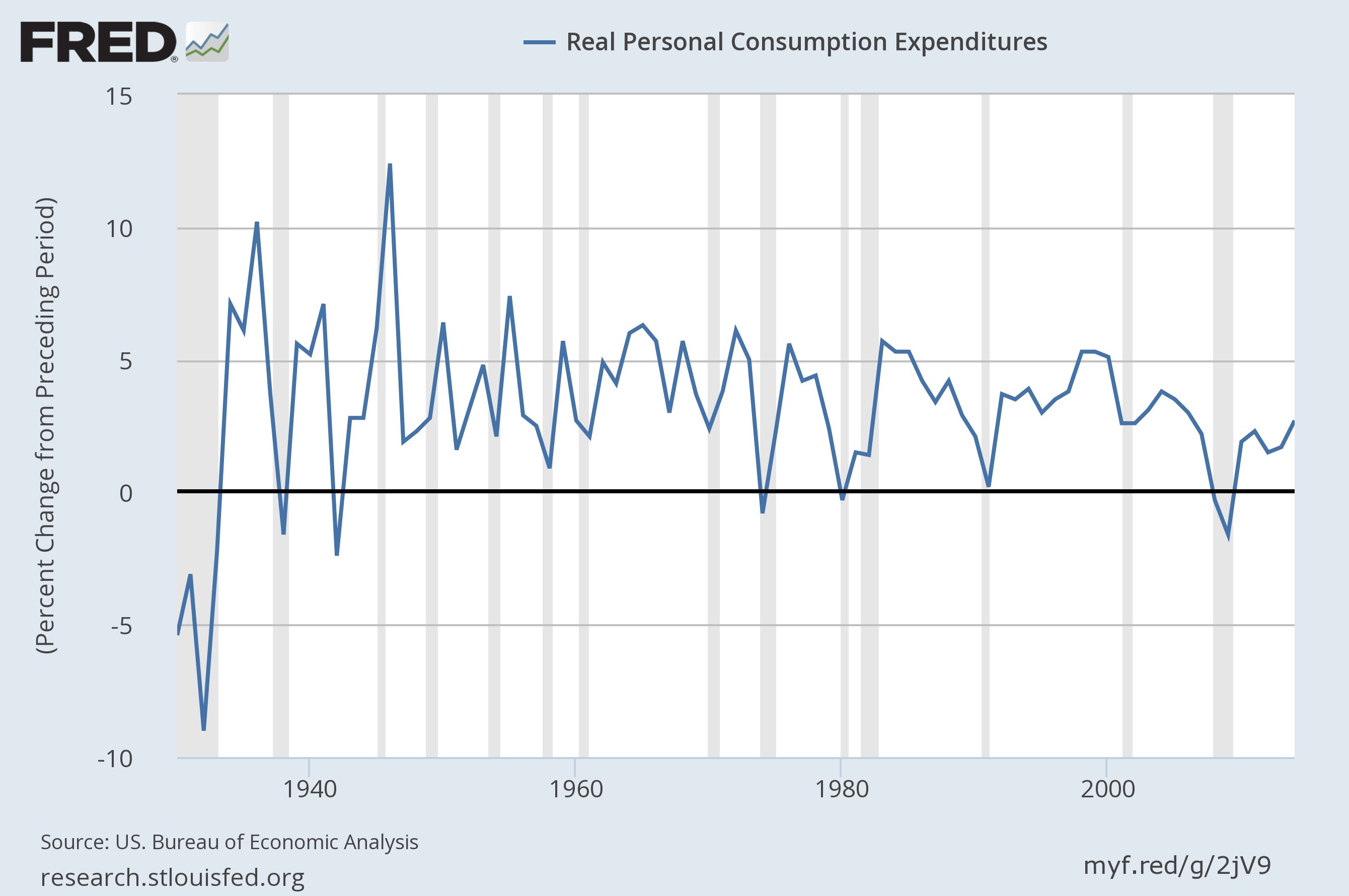

In part, this indicator of more robust growth reflects the strength of consumer spending, shown in Figure 2. Consumer spending has been boosted by the continued gradual improvement in labor markets, lower gasoline prices, and the relative strength in housing prices and stock prices, which have improved household net worth.

While this week’s retail sales number was weak (up .1% M/M and 1.7% Y/Y), the broader measure of consumer spending (total real PCE expenditures) is up 2.7% Y/Y.

Although this is historically weak, it is positive.

Rosengren’s basic analysis is sound: so long as there is sufficient domestic demand and consumer spending, the economy will be fine. Current GDP projections support this analysis. The Atlanta Fed’s GDP now model shows a 2.3% 4Q GDP rate – the same as Moody’s forecast. The Cleveland Fed’s number is a bit lower at 1.9%. Conversely, the Atlanta Fed’s recession probability indicator is at 13%.

The market remains expensive. The current and forward PEs for the SPYs and QQQs are 22.70/22.75 and 17.25/19.75, respectively. The market desperately needs revenue growth, which is not forthcoming:

Including this morning’s reports, we now have Q3 results from 455 S&P 500 members that combined account for 92.8% of the index’s total market capitalization. Total earnings for these 455 companies are down -2.5% on -4.1% lower revenues, with 68.6% beating EPS estimates and only 42.1% coming ahead of top-line expectations. Excluding Energy, total earnings for the rest of the index members that have reported would be up +4.5% on +1.7% higher revenues.

.....

For the Russell 2000 index, we currently have Q3 results from 1693 members that combined account for 86.7% of its total market cap (the index currently has 1979 members at present). Total earnings for these 1693 index members are down -13.9% from the same period last year on +1.8% higher revenues, with 50.6% beating EPS estimates and only 36.7% beating revenue estimates.

The US is clearly in a profits recession as noted in several news reports last week (see here and here. However, the damage so far is contained.

The market clearly noticed the weakening profits picture last week:

After coming close to previous highs, the SPYs fell a little over 4% last week. The MACD gave a bearish cross over and prices are resting right on the 200 day EMA. Adding to the potential problems: the IWMs again fell below the 200 day EMA and transports still couldn’t move through the 200 day EMA.

Conclusion: last week’s price action continues to illustrate my main concern with the market: it’s expensive and needs revenue growth, which isn’t occurring.