Asset Matters: How Goals-Based Allocation Drives Portfolio Positioning

Goals lead us beyond the simple mix prescribed by a risk profile—conservative, moderate, aggressive—and help us understand how wealth fits into our clients’ lives and what they want to achieve with the assets they have accumulated. This may include providing education for children and grandchildren, having more flexibility in retirement spending or fulfilling specific charitable wishes.

Taking a page from institutional investors

The trend of goals-based allocation first took hold in the institutional world. Think of a company preparing for future pension outlays or a university endowment planning for a specific investment like a new campus building. Because institutional portfolio designers know the particular goal and the exact time horizon, they can design an allocation geared toward that outcome. This is known as liability-driven investing (LDI), and the process has become a standard practice for many institutions.

While a duration-targeted LDI portfolio may not suit the typical family, we can use the same concept to identify specific goals and timelines for clients, which then guide asset allocation proposals and portfolio construction. Here we share a few examples to bring the concept to life.

Sample Allocation Example 1: Spending in retirement

One of the most common client scenarios we face is tackling the allocation for a couple that is spending in retirement. For many families, the entire pool of their wealth is intended to be their support in retirement. In this case, the goal for the entire portfolio is the same—achieving a level of income to support regular expenses, without dipping substantially into the principal balance.

Given today’s low level of interest rates, however, we find that many families are often allocated in too risky a mix of assets. Indeed, if you look at a typical target date fund, the prevailing approach is to hold a majority of assets in stocks even in retirement. The other challenge is that the yield on traditional fixed income, like Treasury bonds, is currently too low to support a majority allocation to traditional fixed income and still provide sufficient yield.

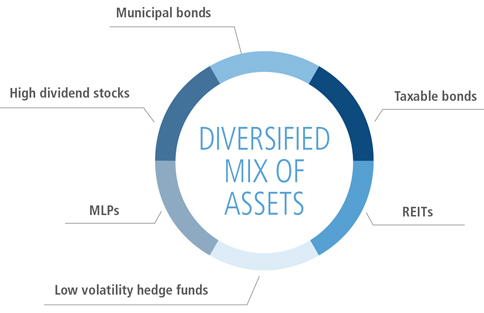

Sample Allocation 1: Spending In Retirement

This single portfolio may include a diversified mix of assets that balance growth and income generation to help meet spending needs through the retirement years.

There are ways to construct a creative and diversifying mix of income-generating investments. For investors that are comfortable moving further out on the risk-return spectrum, a solution could include income-oriented equity (which tends to include higher-quality dividend-paying stocks) alongside higher-yielding fixed income asset classes in both taxable and municipal bond strategies. Another possible option might be an allocation to an absolute return or long-short equity strategy, with the goal of diversifying traditional equities and bonds.

Sample Allocation Example 2: Accommodating lifestyle spending as income changes

Sometimes a family has seemingly conflicting goals for a portfolio, like wanting to spend out of savings in the short term while maintaining long-term growth potential through illiquid investments. For example, let’s assume a married couple with a high level of annual income, about $5 million a year, substantial savings of approximately $6 million and high lifestyle spending: three houses, frequent travel and two children in college. They both expect to scale back on working in the near future to a state of semi-retirement and want to rely on their savings as they adjust. They have a moderate risk profile, but are qualified for alternative assets and interested in incorporating private equity and other less-liquid alternative investments in their portfolio.

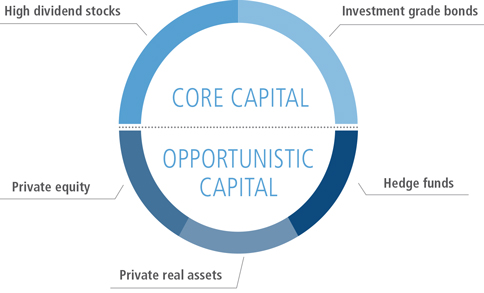

In this case our approach might be to propose an overall portfolio that involves segmenting it into two halves and allocating the two portions separately. The first half, which we call “core capital,” would be allocated to liquid and moderately conservative investments— primarily investment grade bonds and some high-quality dividend stocks. The other half of their assets, which we would call “opportunistic capital,” would be allocated to private equity and other alternative assets with higher growth potential. This approach could give the couple a level of comfort in maintaining their allocations during periods of volatility as the “core capital” half would be available for short-term needs.

Sample Allocation 2: Core Capital + Opportunistic Capital

This clearly segmented portfolio could include a lower-volatility, income-focused component and a more-aggressive, less-liquid growth component.

Sample Allocation Example 3: Earmarking investments for charitable giving

Families may also have specific charitable giving goals. Let’s assume a couple has about $5 million in assets for the family’s personal investments, and another $3 million in assets for charitable goals. The couple has a conservative risk profile for their personal portfolio and a more aggressive profile for their charitable portfolio, driven in part by their charitable commitments.

Another sample approach to constructing their portfolio might first involve suggesting that they consult with a trust and estate planning attorney to consider setting up a charitable trust for the assets earmarked for giving, as this may provide some tax benefits. The timeline for the charitable commitment is long—approximately 20 years. Given the long time horizon, a low need for liquidity and an aggressive risk profile, we might design an allocation for the charitable assets that includes a mix of traditional equity and alternative assets. In the personal portfolio, the assets could be allocated to a conservative mix of municipal and taxable bond holdings.

Sample Allocation 3: Separate Portfolios for Personal and Charitable Use

Creating separate portfolios delineates assets by goals. If the charitable assets are located in a charitable trust, there could also be certain tax advantages.

Starting with the end in mind

Individuals and families may not have an exact timeline and specific goals for assets the way that institutions do. Still, incorporating an institutional approach of identifying goals to the extent possible offers us a more nuanced picture of our private wealth clients than we can obtain from risk profile alone. The truth of the matter is that there are many ways to assemble a moderate or conservative portfolio. With goals as the guide, we can tailor a mix of investments to clients’ intended time horizons or liquidity levels, and thereby help them achieve their long-term objectives.

Deploying Skill to Finesse Uncertainty

Establishing differentiated portfolio construction that can address unique needs and goals is a critical first step in the investment process. Extending this active approach to day-to-day investing can help mitigate the impact of an unsettled market environment.

Since the financial crisis, globalization and unprecedented central bank intervention have changed the investment landscape, disrupting traditional correlations between asset classes. Further, periods of volatility associated with these forces suggest we may not soon settle into “normal” patterns.

In our view, investment strategies that rely on backward-looking metrics may not be ideal in an environment characterized by volatility and evolving correlation patterns. As an example, asset allocation models that rely on a mix of stocks and bonds for diversification are not likely to hold up well in a year like 2015 when both the S&P 500 and long-term government bonds are down 4.5% and 4.9%, respectively, year-to-date.

In an environment of unpredictability, choosing an experienced, skillful manager with the ability to draw important distinctions among securities, industries and asset categories can be especially important in seeking to achieve positive outcomes. Similarly, we feel there’s considerable potential upside in selecting active strategies that can leverage uncertainty to their advantage or perform well in an environment of lower correlations where the markets increasingly differentiate between winners and losers.

This material is provided for informational purposes only. Nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. The views expressed herein are generally those of Neuberger Berman’s Investment Strategy Group (ISG), which analyzes market and economic indicators to develop asset allocation strategies. ISG consists of investment professionals who consult regularly with portfolio managers and investment officers across the firm. This material may include estimates, outlooks, projections and other “forward-looking statements.” Due to a variety of factors, actual events may differ significantly from those presented.

Any views or opinions expressed may not reflect those of the firm as a whole. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Third-party economic or market estimates discussed herein may or may not be realized and no opinion or representation is being given regarding such estimates. Certain products and services may not be available in all jurisdictions or to all client types. Indexes are unmanaged and are not available for direct investment. Unless otherwise indicated, returns shown reflect reinvestment of any dividends and distributions. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

This material is being issued on a limited basis through various global subsidiaries and affiliates of Neuberger Berman Group LLC. Please visit www.nb.com/disclosure-global-communications for the specific entities and jurisdictional limitations and restrictions.

The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC.