At first blush, the economy’s growth rate in the third quarter (+1.5%) suggests a significant slowing of activity after its solid performance in the second quarter. However, doubts should be set aside, as it was largely a reduction in inventories that held back overall gross domestic product (GDP) growth. In fact, final sales remained strong. Headline growth should pick up as firms increase inventories in the quarters ahead.

The U.S. Congress passed the Bipartisan Budget Act of 2015, which prevents unnecessary debt ceiling dramas until March 2017. The stance of the central banks of China and the eurozone are supportive of economic growth. Against this backdrop, the Federal Reserve was in a position to downplay concerns of global headwinds and prepare financial markets, via its October policy statement, for a December policy rate increase.

The positive developments on the policy front and the nature of incoming data support forecasts of continued U.S. growth during the coming quarters. The U.S. economy is predicted to advance at an annual rate of almost 2-3/4% in the final quarter of 2015.

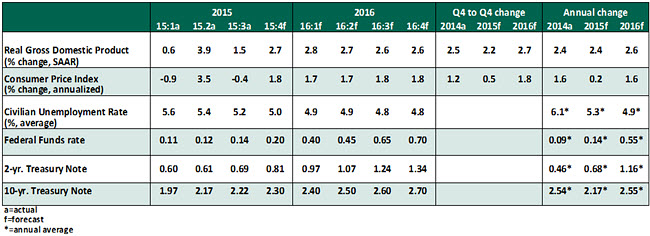

Key Economic Indicators

Key Elements of Forecast: M

- Consumer spending averaged 3.4% in the six months ended September. Employment data support projections of continued growth in the near term. October auto sales (18.2 million units) were higher than expected, which provides an extra boost to overall consumer expenditures. Low gasoline prices are another positive factor. There is little, if any, evidence that points to a possible weakening of consumer spending.

- The upward trend of the trade-weighted dollar has set back performance of the factory sector. Industrial production advanced only 1.6% from a year ago in the third quarter, the slowest pace of activity since the first quarter of 2014. Although business equipment spending moved up on a sequential basis in the third quarter, the gain from a year ago is the smallest in the current expansion. Manufacturing accounts for 12% of GDP and close to 9% of total employment.

- The forward momentum of the non-manufacturing sector offsets the deceleration of the factory sector. In particular, the Institute of Supply Management’s (ISM’s) non-manufacturing index moved up in October (59.1), close to the high for the expansion (60.3), after slipping in September.

- Recent housing market data point to three prominent developments. First, sales of existing homes fared better than that of new homes in the third quarter. Inventories of unsold homes, both new and existing, are not worrisome, as they are below the historical average. Second, construction of new homes was biased toward single-family homes, while starts of multi-family homes slipped. The rental vacancy rate of homes moved up slightly in the third quarter, implying that multi-family home construction activity may slow. Third, the homeownership rate held steady in the third quarter after declining mostly since 2004. We will be watching this closely to ascertain if it is only a one-off event or the beginning of a new turning point for the better.

- Exports of goods and services advanced in September, following a large drop in the prior month. On net, the trade numbers do not affect the advance estimate of third quarter real GDP. Overall, there are questions about the likely trend of exports. The strength of the dollar and the weak performance of major U.S. trading partners suggest that a positive contribution from exports to GDP growth is unlikely in the near term. The latest ISM factory survey points to a weak export index. A widening trade deficit in the near term should reflect a further increase in U.S. imports and a lack of export growth.

- Labor market data were near perfect in October. Payrolls advanced at a solid clip; the jobless rate edged down; hourly earnings recorded a 2.5% year-to-year increase (the highest since 2009); part-time employment fell; the broad measure of unemployment declined; and jobless claims are close to the cycle low.

- Despite bullish economic data, inflation continues to hover below the Fed’s 2.0% target. The personal consumption expenditure (PCE) price index has risen by 0.3% from a year ago, the third straight quarterly reading below 1.0%. The core PCE price index, which excludes food and energy, has recorded year-to-year gains of 1.3% for three straight quarters. The confluence of subdued energy prices and non-energy commodity prices and a strong dollar is holding down inflation. The resilience of the domestic economy is expected to lift inflation toward the Fed’s target.

- The bar is very high for the Fed to leave the policy rate unchanged at the upcoming meeting. Only a major international crisis will prevent the Federal Reserve from instituting a higher policy rate at the December 15-16 meeting.