Despite the persistence of low inflation, the Fed will probably rasise rates in December. This begs the question, why? A Bloomberg article last week provides the answer:

The Federal Reserve Board released an updated version of its large-scale model on the U.S. economy that may hold clues into why policy makers pivoted at their meeting earlier this week toward a December interest-rate increase.

The revised inputs and calculations on Friday suggest the economy will use up resource slack by the first quarter of 2016, according to an analysis by Barclays Plc, and that also indicates Fed staff lowered their near-term estimate for how fast the economy can grow without producing inflation -- a concept known as potential growth.

“The output gap appears closed,” said Michael Gapen, chief U.S. economist at Barclays’s investment-banking unit in New York. “This means further progress would lead to resource scarcity and potential upward pressure on inflation in the medium term.”

In other words, the Fed will raise rates in anticipation of the output gap closing. While the following charts are far less sophisticated, they potentially counter the Fed model’s conclusions. Let’s start with capacity utilization:

Over the last three expansions, utilization peaked at continually lower levels. And since January, the oil market contraction, strong dollar and weak export markets further lowered this metric. Both facts imply a fair amount of manufacturing slack exists. As for employment, the U-6 unemployment rate is just now hitting levels that were the peaks of previous expansions. In fact, Martin Wolf recently argued the US labor market is simply not working (for more detail, see this article in the FT). However, some at the Fed believe the long-term unemployed will not be rehired. If so, then it’s less advantageous to use U-6 as an indicator of labor slack.

Friday’s jobs report all but guaranteed a December rate hike. The headline number was a gain of +271,000. As I noted on Twitter, “temporary, retail and construction added 99,300 total jobs. Add professional services, the number rises to 177,300.” All of those gains are abnormal based on recent experience. I previously argued that the industrial recession was the primary cause for weak job growth. It appears that the effects of that event have been reversed, at least for one month. Obviously, we’ll need a few more strong reports before signaling all clear.

Other news from the report was positive:

In October, average hourly earnings for all employees on private nonfarm payrolls rose by 9 cents to $25.20, following little change in September (+1 cent). Hourly earnings have risen by 2.5 percent over the year. Average hourly earnings of private-sector production and nonsupervisory employees increased by 9 cents to $21.18 in October. (See tables B-3 and B-8.)

The change in total nonfarm payroll employment for August was revised from +136,000 to +153,000, and the change for September was revised from +142,000 to +137,000. With these revisions, employment gains in August and September combined were 12,000 more than previously reported. Over the past 3 months, job gains have averaged 187,000 per month

The lack of meaningful wage growth has concerned analysts for the duration of this expansion. The latest numbers were very positive. And, obviously, the increase in total jobs created is welcome.

Two more fixed income stories deserve mentioning. First, the Financial Times reported the number of companies with weakening credit positions has increased:

Lists maintained by both Standard & Poor’s and Moody’s of the weakest companies in their respective coverage universes have started to swell. S&P counts 167 issuers with some $216bn in debt outstanding among its lowliest rated groups. Yields for these borrowers in turn have soared, hitting a high of 8.2 per cent at the start of October from a low of 5.9 per cent in March.

.....

“Absent the central banks, we would be in the later stages of a credit cycle,” says David Blake, chief investment officer for Principal Global Investors, an asset manager. Yet while he sees a slow deterioration in credit metrics, he continues to find investment grade credit attractive. “We’re in the eighth inning of an extra inning game,” he says.

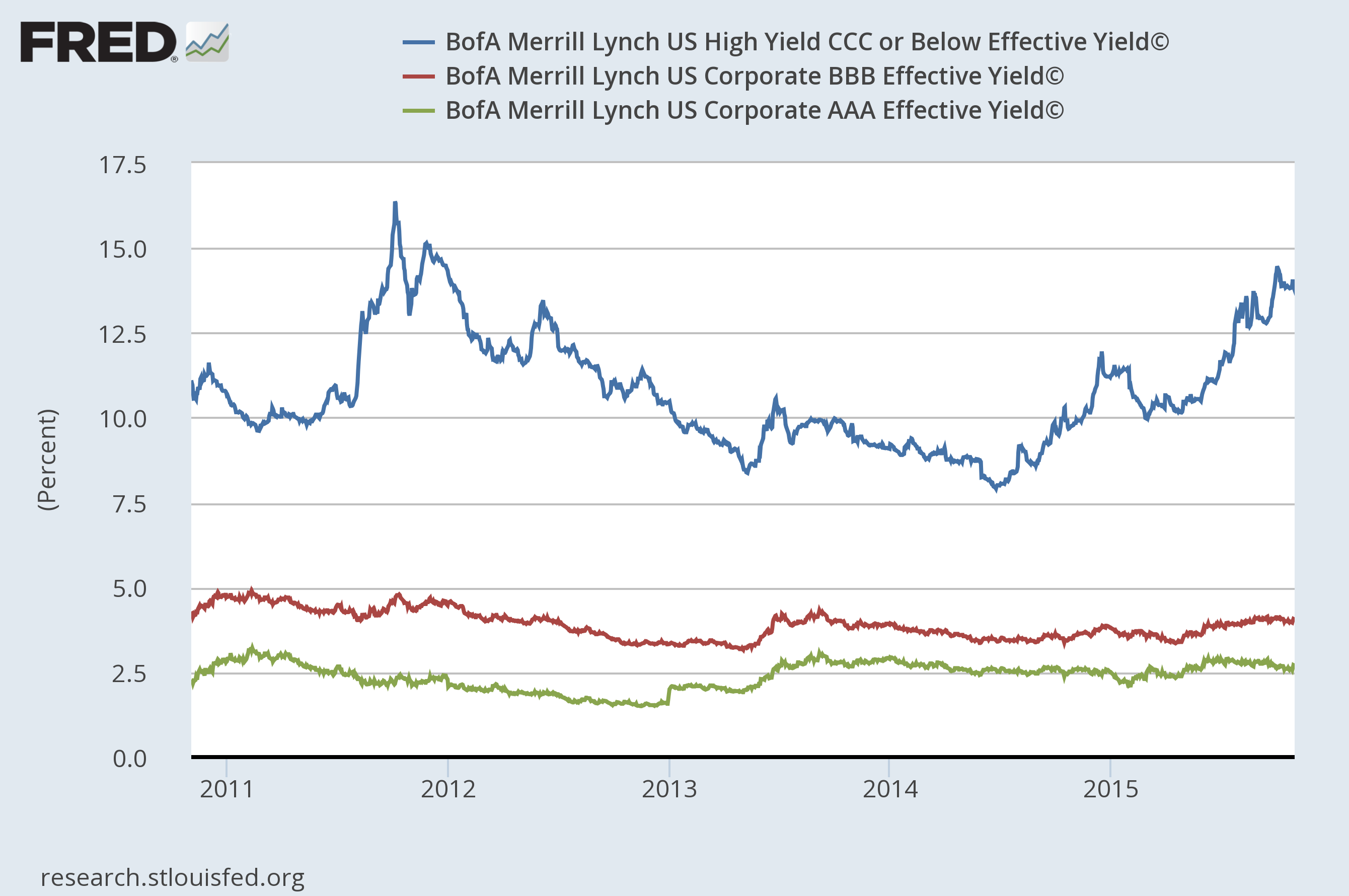

As this chart from the FRED system shows, CCC yields have risen, but other credit ratings have been stable:

This tells us that weaker companies could begin having problems. The key will be when the higher rated issuers (BBB and AAA) start to widen.

Second, and also from FT, is this: the change in Treasury bond ownership means an increase in volatility:

“Price insensitive buyers (such as foreign officials, banks, and the Fed) have been replaced by price sensitive buyers. This suggests that demand for Treasuries could become somewhat more volatile . . .”

This is the natural result of ownership changing from central banks to investors.