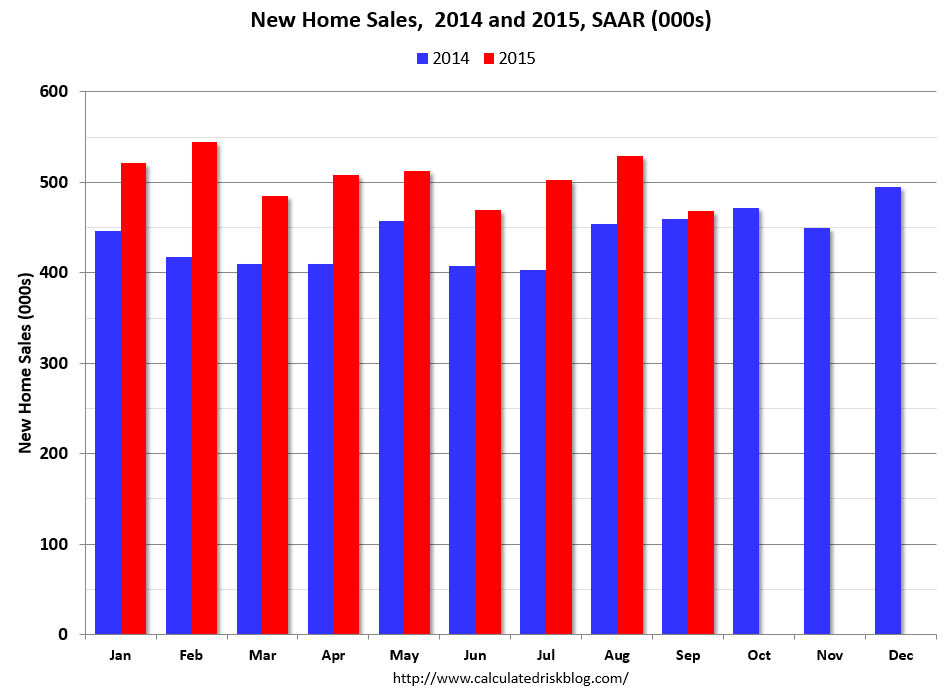

New homes sales disappointed with the M/M figure off 11.5%. The Northeast experienced the biggest decline with a 61% drop. a fall of this magnitude is not unheard of. The Census Bureau revised the previous two months figures lower. Analysts offered several reasons for the drop, ranging from low inventory to tough credit conditions. However, other housing numbers, including new home prices, are positive, meaning this figure is probably temporary. Bill McBride at Calculated Risk pointed out that the Y/Y figures are still very strong:

Even though the September report was disappointing, sales are still up solidly year-to-date. The Census Bureau reported that new home sales this year, through September, were 392,000, not seasonally adjusted (NSA). That is up 17.6% from 333,000 sales during the same period of 2014 (NSA). That is a strong year-over-year gain for the first nine months of 2015!

And as the following chart from his blog shows, each month this year is stronger than the previous years:

Finally, it appears the homeownership rate may have hit bottom. If so, this means the low level of new homes for sale could lead to a large increase in new construction for the foreseeable future.

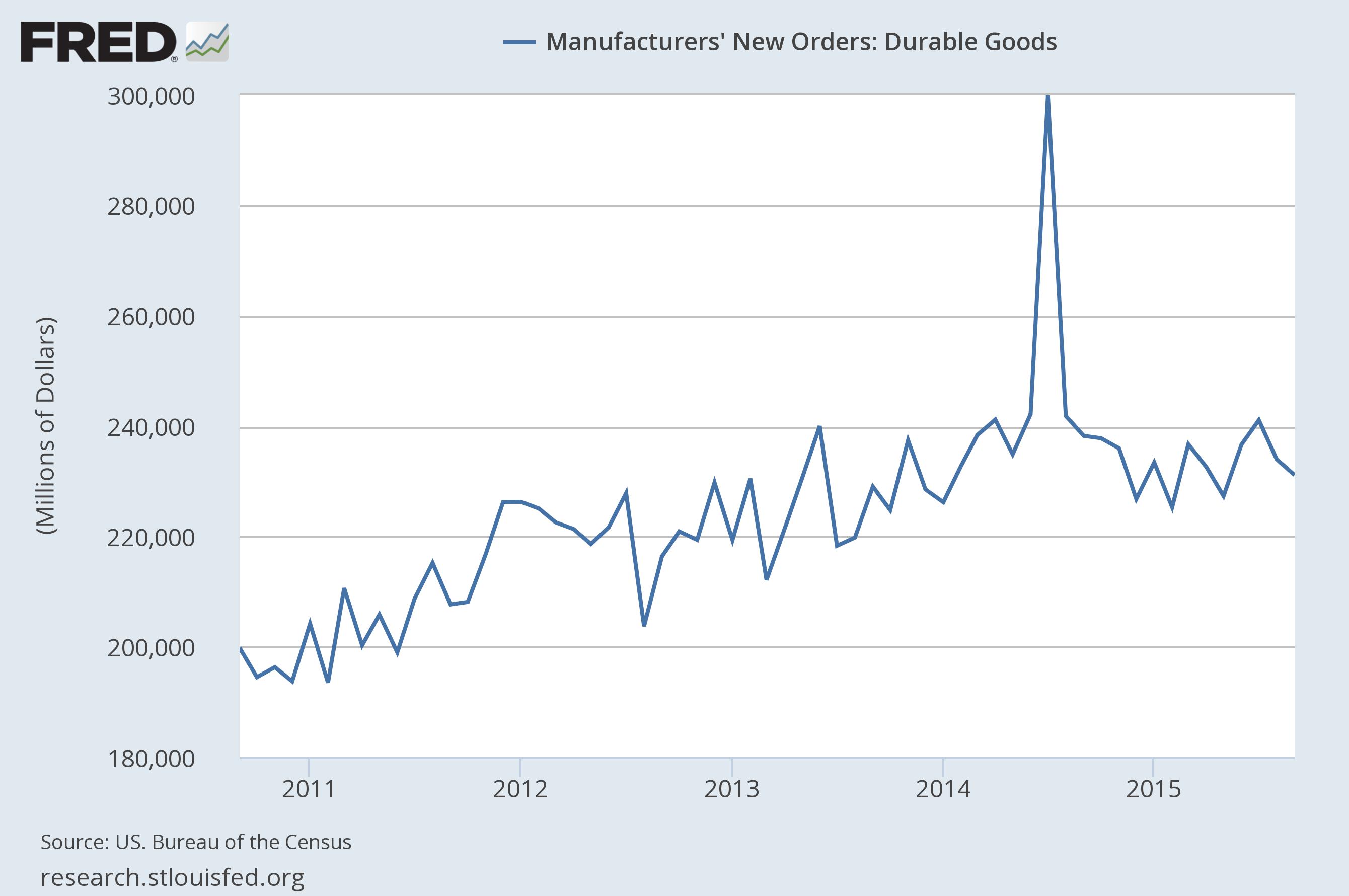

The 1.2% decline in new orders for durable goods indicates the industrial recession continues. Ex-transport, the figure was off .4% and ex-defense the number was down 2%. As shown in the following FRED chart, this data series has printed between 220,000 and 240,000 for 3½ years:

There are several intertwining causes for this weakness: the strong dollar, weak international economies (especially developing markets) and weakness in the oil patch.

The 3Q GDP advance estimate was 1.5%. Consumer spending was very strong, up 3.2%. Spending on durable goods increased 4.5% while non-durable spending gained 6.7%. The biggest reason for the drop was an inventory correction, which subtracted 1.44% from output. Had this number been 0, GDP would have been 2.94%. According to Bloomberg:

A smaller gain in inventories subtracted 1.4 percentage points from growth, the biggest drag since the last three months of 2012, according to the Commerce Department. An annualized $59.8 billion slowdown from the prior quarter was the largest since the third quarter of 2011.

“The story on inventories is that it’s a big adjustment that occurred quickly, and should be far less of a drag” in the next few quarters, Stuart Hoffman, chief economist at PNC Financial Services Group Inc. in Pittsburgh, said before the report.

Overall, this wasn’t a bad report for the weakness. As one commentator noted:

(1) the consumer has not been harmed, and continues to power the US economy forward;

(2) the bleeding in the import/export sector has been staunched; and

(3) affected industries are making progress working through their accumulated inventories

The BEA issued personal income and spending figures on Friday. The report also contained inflation adjusted data:

Real DPI -- DPI adjusted to remove price changes -- increased 0.2 percent in September, compared with an increase of 0.4 percent in August.

Real PCE -- PCE adjusted to remove price changes -- increased 0.2 percent in September compared with an increase of 0.4 percent in August. Purchases of durable goods increased 0.6 \ percent in September, the same increase as in August. Purchases of nondurable goods decreased 0.3 percent in September, in contrast to an increase of 0.3 percent in August. Purchases of services increased 0.3 percent, compared with an increase of 0.4 percent.

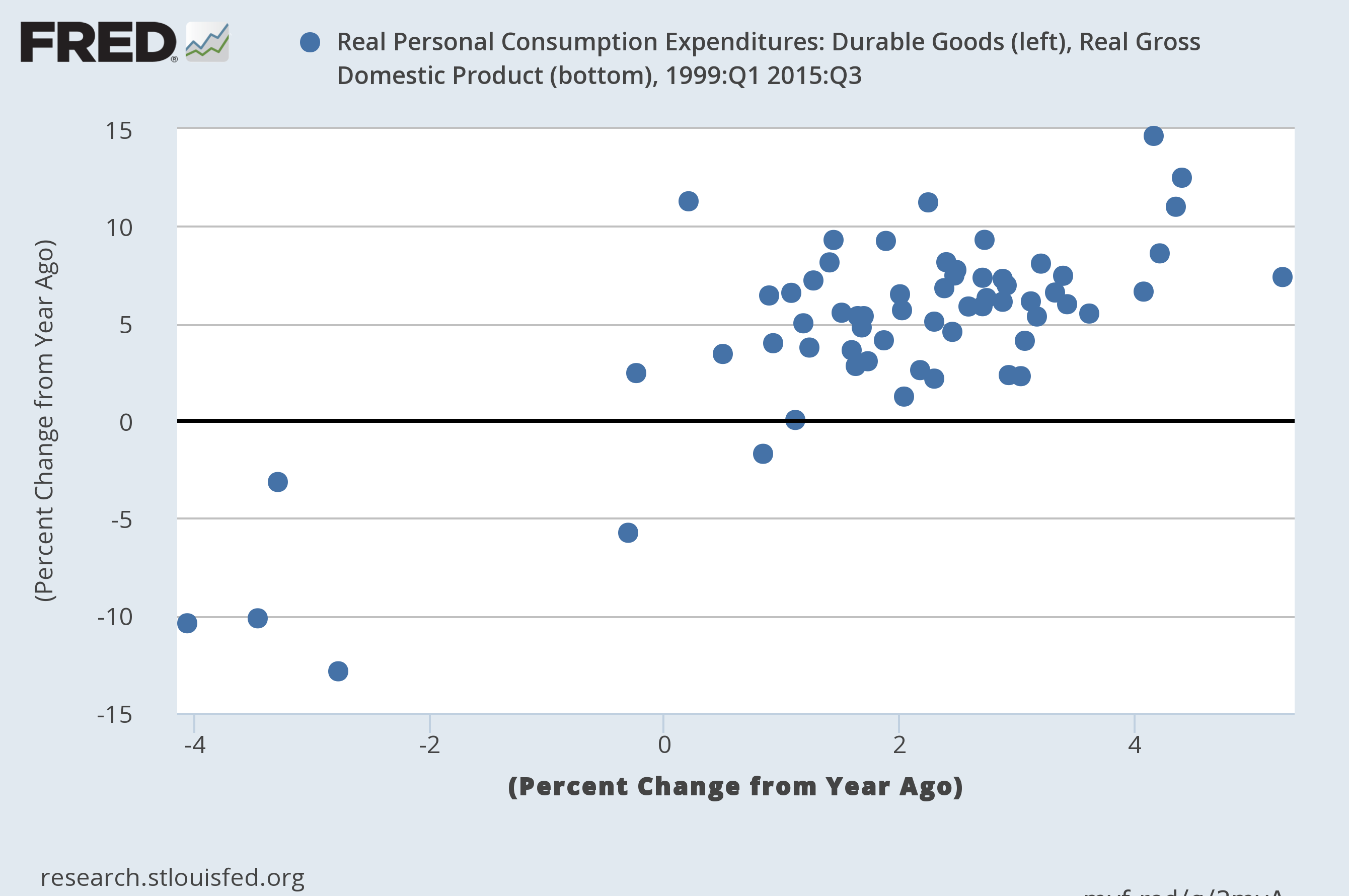

The durable goods number was very encouraging; it indicates the consumers are still spending, and, more importantly, have enough confidence in the future to make large purchases. As this chart from the FRED database shows, there is a very strong correlation between positive Y/Y real durable goods purchases and positive real GDP growth:

Economic Conclusion: this week’s news was weak. Most importantly, the shallow industrial recession continues. And with continued international and energy sector weakness, it’s doubtful we’ll see a meaningful increase in the foreseeable future. The 3Q GDP figure may be a one-off caused by an inventory drawdown; we’ll have to wait and see how Moody’s and the Atlanta Fed start to project 4Q numbers. Although the headline PCE number was the weakest in 8 months, the strong durable goods purchases number was encouraging.

Market Overview: the market is still expensive. The current and forward PE ratios for the SPYs and QQQ are 22.65/22.98 and 17.89/19.85. More importantly, 3Q revenue growth has been weak. From Zacks:

It is hard to characterize this earnings season as anything but weak – the overall growth picture remains challenged, with companies struggling to beat lowered top-line expectations and estimates for the current period coming down at an accelerated pace. At this stage in the reporting cycle, the ratio of companies beating revenue estimates is the lowest that we have seen in the recent past.

As shown in this table from the same report, total revenue was down 4.9% and was up a mere 1.5% ex-energy:

Factset.com offers a more nuanced interpretation of the data:

The blended revenue decline for Q3 2015 is -2.9%. If this is the final revenue decline for the quarter, it will mark the first time the index has seen three consecutive quarters of year-over-year revenue declines since Q1 2009 through Q3 2009. However, seven sectors are actually reporting year-over-year growth in revenue, led by the Telecom Services and Health Care sectors. Only three sectors are reporting a year-over-year decline in revenue, led by the Energy and Materials sectors.

As I noted last week, there is a growing possibility that revenue has peaked for this expansion.

Looking at the SPYs on a daily basis, we see the following chart:

Prices formed a double bottom after the late August sell-off. They rallied through the initial resistance level between 198 -200 and are now a few points away from their all-time high. But the MACD is very extended. Mid-caps are still hitting resistance at the 200 day EMA while the IWMs (Russell 2000) have retreated below their 50 day EMA (which is still below the 200 day EMA). The percentage of NYSE and NASDAQ stocks above their 50 day EMAs is approaching overbought territory. And the NASDAQ cumulative advance/decline line is negative. Fundamentally, the primary push for the latest move higher came from the EU’s dovish statement; the Fed, in contrast, is far more hawkish.

If the SPYs hit a record high, I don’t see it lasting, barring a change in the underlying fundamentals.

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis