US Bond Market Week in Review: Using Last Year's Model For This Year's Problem, Edition

The Fed issued its latest statement on Wednesday. It offered the following assessment of the current economy:

Information received since the Federal Open Market Committee met in September suggests that economic activity has been expanding at a moderate pace. Household spending and business fixed investment have been increasing at solid rates in recent months, and the housing sector has improved further; however, net exports have been soft. The pace of job gains slowed and the unemployment rate held steady. Nonetheless, labor market indicators, on balance, show that underutilization of labor resources has diminished since early this year. Inflation has continued to run below the Committee's longer-run objective, partly reflecting declines in energy prices and in prices of non-energy imports. Market-based measures of inflation compensation moved slightly lower; survey-based measures of longer-term inflation expectations have remained stable.

…..

Inflation is anticipated to remain near its recent low level in the near term but the Committee expects inflation to rise gradually toward 2 percent over the medium term as the labor market improves further and the transitory effects of declines in energy and import prices dissipate.

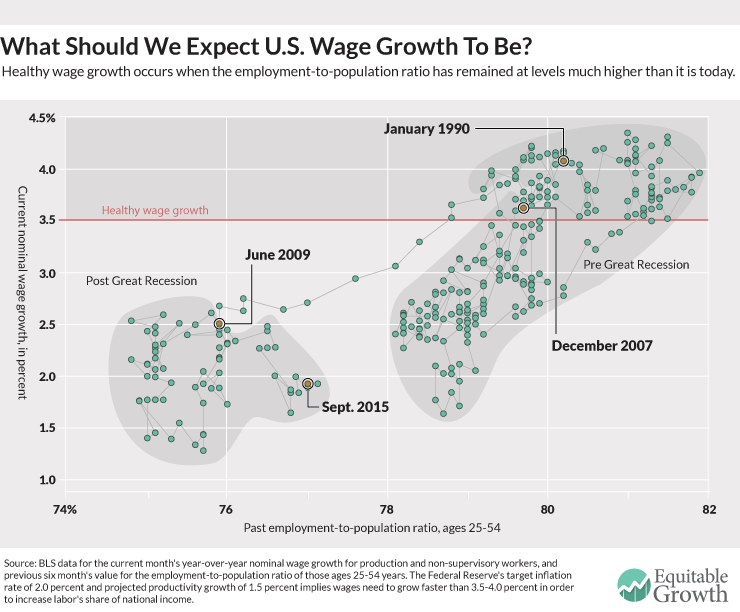

There are several problems with the above passages. First, they’re placing a great deal of importance on the decline in under-utilization, assuming that, as broader measures such as U-6 decline, wage pressures will increase. In short, they still believe in the Phillip’s Curve. But recently Fed President Brainard and Tarullo argued the Phillips Curve was at best very weak in the current environment. And Nick Bunker at the Center for Equitable Growth offers this chart using inflation and a modified employment/population ratio:

The chart does show a positive correlation. But, the current employment/population ratio is too low to provide a meaningful boost to wages. This leads to a more disturbing question: has the decline in the labor force participation rate taken the employment/population ratio to a low too low to have an impact on wages?

As for prices, they then note that energy and import prices are the primary reason for the decline in CPI, but they’re still assuming these are transitory developments. However, thinking on this is changing as well. At his latest press conference, Mario Draghi noted something had changed with inflation, but didn’t know exactly what. He did mention the subject needed more study when he stated, “Most notably, the strength and persistence of the factors that are currently slowing the return of inflation to levels below, but close to, 2% in the medium term require thorough analysis.” Fed President Brainard offered a more detailed answer in her most recent speech:

Downgrades to foreign growth affect the U.S. outlook through several channels. First, weak growth abroad reduces demand for U.S. exports. Second, the expected divergence in U.S. growth increases demand for U.S. assets, putting upward pressure on the dollar, which, in turn, weighs on net exports. The estimated effect of dollar appreciation on net exports has been shown to be substantial and to persist for several years. Weak demand weighs on global commodity prices, which, together with the effects on the dollar, restrains U.S. inflation. Finally, the anticipation of weaker global growth can make market participants more attuned to downside risks, which can reduce prices for risky assets, both abroad and in the United States--as we saw in late August--with attendant effects on consumption and investment.

There are several moving pieces in the above analysis. Declining Chinese demand for raw materials is lowering emerging market growth. This makes the US a more attractive investment, increasing the dollar. This has the ancillary effect of further lowering commodity prices. And lower commodity prices along with a stronger dollar lower inflation. Brainard’s causal chain also has a far longer timeline, unlike the Fed’s statement which implies higher inflation is right around the corner. And assuming Brainard is right, then the economy faces a far longer period of weaker commodity prices, due in large part to the long arc of the commodity super cycle.

The problems inherent in the Fed’s reasoning makes it look more and more that they’re using last year’s ideas for this year’s problems. It appears more and more that central bankers need to drastically rethink their models and assumptions, as recently noted by Antonio Fatas (with a big hat tip to Mark Thoma):

The comparison with the 70s when stagflation produced a large change in the way academic and policy makers thought about their models and about the framework for monetary policy is striking. During those year a high inflation and low growth environment created a revolution among academics (moving away from the simple Phillips Curve) and policy makers (switching to anti-inflationary and independent central banks). How many more years of zero interest rate will it take to witness a similar change in our economic analysis?

(c) Hale Stewart

http://community.xe.com/blog/xe-market-analysis