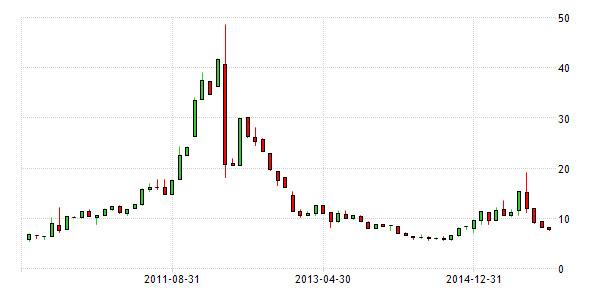

Rahm Emanuel once said “never let a serious crisis go to waste.” Those who heeded the call in buying Greek bonds at the height of the country’s debt crisis hit pay dirt. When Greek bonds cratered, benchmark 10-year government bond yields rocketed to nearly 50 percent the eve of Greece’s debt restructuring March 9, 2012.

As part of the restructuring, the Hellenic Republic struck a deal with bondholders to accept losses as high as 74 percent on their holdings. In return, Greece received a second bailout package of 130 billion euros from the International Monetary Fund, European Union and European Central Bank. The country’s bond prices roared back. Yields plunged to 12 percent by year’s end. Greek government bonds rallied some 80 percent in 2012. Yields fell to the high single digits by the end of 2013 and as low as 5.5 percent in 2014.

Greece Government Bonds 10-Year Yields

TradingEconomics.com: “Greece Government Bond 10-year increased to 7.76 percent on Thursday, October 22 from 7.70 percent in the previous trading day. The Greece Government Bond 10-year yield averaged 7.84 percent from 1998 until 2015, reaching an all-time high of 48.60 percent in March of 2012 and a record low of 3.21 percent in June of 2005.”

Is Puerto Rico America’s Greece?

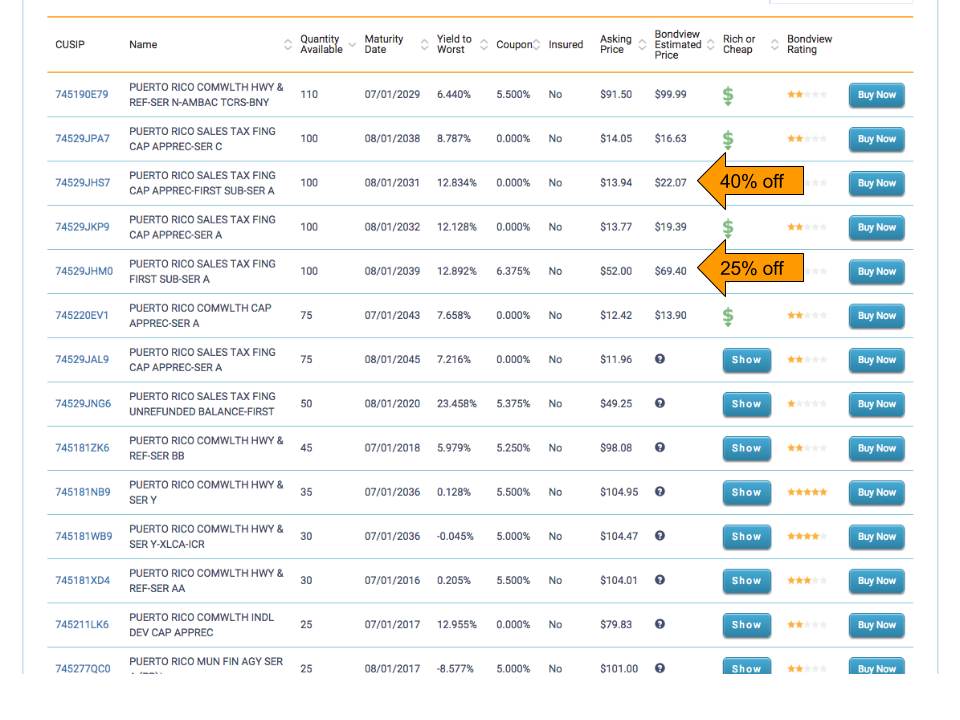

Governor Alejandro Garcia Padilla announced this past summer the Commonwealth cannot make good on its $72 billion debt load. Puerto Rico’s municipal bonds have crashed just like Greek bonds did three years ago. BondView’s database of Puerto Rico bonds shows some long-dated, sales-tax bonds are trading for as little as 12 cents on the dollar. Some short-dated university bonds are showing a yield to worst (the lowest an investor expect) of 100 percent while trading for 49 cents on the dollar.

Puerto Rico’s bonds have been quite popular for decades. Their interest income is free from local, state and U.S. federal income taxes, unlike most other municipal bonds. About 70 percent of municipal bond mutual funds held Puerto Rican bonds as of Feb. 2014, according to Credit Suisse. Other investors include hedge funds and individual investors mostly from the U.S. and Puerto Rico.

Greece’s bonds recovered thanks to a bailout from its financial fairy godmother, aka the European troika. If Puerto Rico’s financial fairy godmother, in this case Uncle Sam, comes to the rescue, Puerto Rico bonds will most likely recover as well.

Puerto Rico cannot file for municipal bankruptcy protection. But the U.S. House of Representatives has introduced legislation to extend Chapter 9 bankruptcy protection to Puerto Rico. It would have to show insolvency and good-faith negotiations with creditors to qualify.

A bailout may not be necessary. The U.S. could make a handful of moves to help Puerto Rico return to solvency with little to no cost to U.S. taxpayers, says Ted Hampton, vice president and senior credit officer at Moody’s Investors Service.

A “superbond” in which the U.S. Treasury would hold Commonwealth revenues in a trust for debt repayment along with a financial control board could speed up restructuring negotiations.

“Other measures to provide relief for Puerto Rico without burdening U.S. taxpayers include loosening federal minimum wage requirements, or granting the commonwealth's employers a reprieve in future minimum wage increases. Congress could also exempt Puerto Rico from Jones Act shipping restrictions,” Hampton said in a statement.

In many ways, Puerto Rico’s economy is much better off than Greece. Puerto Rico’s debt-to-GDP at 66 percent is sky high compared to the 7 percent average for U.S. states. But it pales in comparison with Greece’s debt, which comes 177 percent of GDP.

How to Find Babies Thrown Out With the Bathwater

Puerto Rico issues hundreds of different types of bonds. They shouldn’t be viewed as a homogeneous hoard. They have varying degrees of credit quality and risks. Some are insured. Many have become mispriced because of the company they keep and are trading at a steep discount to face value. Some lower-risk, sales-tax bonds listed in BondView’s database are trading as much as 40 percent below real value. The Commonwealth appears to be making up for its poor track record in income-tax collections by raising sales taxes, which shot up from 7 percent to 11.5 percent in July.

Investment Risks

Investors can potentially hit pay dirt with Puerto Rico’s bonds as they did with Greece’s. But many risks must be considered. The Puerto Rico Fiscal and Economic Growth Plan (FEGP) released in September suggests the island plans to restructure all of its debts. The rating for all of the Commonwealth debt rated by Fitch is 'CC,' which means Fitch concludes default appears likely. Bonds with a 'CC' Rating Watch Negative by Fitch include:

- Commonwealth of Puerto Rico GO and GO-guaranteed bonds

- Puerto Rico Sales Tax Financing Corporation (COFINA) senior and subordinate lien sales tax revenue bonds

- Employees Retirement System of the Commonwealth of Puerto Rico (ERS) pension funding bonds

- Puerto Rico Aqueduct and Sewer Authority (PRASA) senior lien revenue bonds

- Puerto Rico Electric Power Authority (PREPA) power revenue bonds

“The government's direction and interactions with debtholders are highly dynamic, limiting the predictability of outcomes,” Laura Porter, managing director of U.S. Public Finance at Fitch Ratings, and a colleague said in a statement issued Sept. 11. “As the commonwealth's restructuring plans become clearer, Fitch expects to downgrade to 'C' on a security-specific basis at the point that default pursuant to Fitch's rating definitions appears to be inevitable.”

PIMCO, the world’s largest fixed-income investment firm, does not hold Puerto Rico’s bonds in its muni portfolios.

“Puerto Rico’s debt is not sustainable without real economic growth and a consolidated surplus,” Sean McCarthy, a senior vice president and head of the municipal credit research team in PIMCO’s New York office, wrote in a July 16, 2015 note. “These will remain elusive over the next several years by any reasonable estimate. One-off improvements in socioeconomic metrics do not imply debt sustainability. Yes, federal transfers will soften the blow. But difficult fiscal adjustments will occur and sacrifices will fall disproportionately on creditors.”

Puerto Rico’s debt service will eat up more than 30 percent of consolidated revenues excluding federal transfers from 2016 to 2025. Getting to a more viable payment term would require larger haircuts through a decrease in principle, McCarthy says. Otherwise, like Greece, Puerto Rico will need more restructuring.

“Uncertainty over debt modifications may exert further pressure on bond prices,” Sean McCarthy, a senior vice president and head of the municipal credit research team in PIMCO’s New York office, wrote in a July 16, 2015 note. “We expect discussions to devolve to litigation, particularly between holders of general obligation and sales tax bonds. Puerto Rico’s adjustment will take time, hardship, litigation and substantial debt relief.”

Puerto Rico never recovered from the 2008 global recession. Puerto Rico’s unemployment rate remains high at 12.4 percent, as of May 2015. Its labor-participation rate is only 40 percent because workers have little incentive to get a job when welfare pays better than the minimum wage. Greece has a much higher unemployment rate 25.6 percent but a much higher labor-participation rate of 53 percent, as of 2013.

“Puerto Rico has the additional problems of emigration and declining U.S. military presence, making its situation extreme,” said David A. Levy, chairman of the Jerome Levy Forecasting Center in Mount Kisco, N.Y. “Economic conditions in the mid-2010s will only aggravate the situation. Puerto Rico will default on a great deal of debt unless the federal government steps in, as eventually it will probably have to.”

Robert Kane is the CEO of BondView, the leading provider of municipal bond data and analytics. Features include third-party independent estimated bond prices, bond stress testing, portfolio analysis, alternative bond ratings, fund ratings, real time market data and alerts. He can be reached at [email protected].

© BondView