It's Darkest Before the Dawn – but Is the Time Now 1am or 5am?

Historic context is useful to understanding the energy sector.

What is causing oil prices to fall so far?

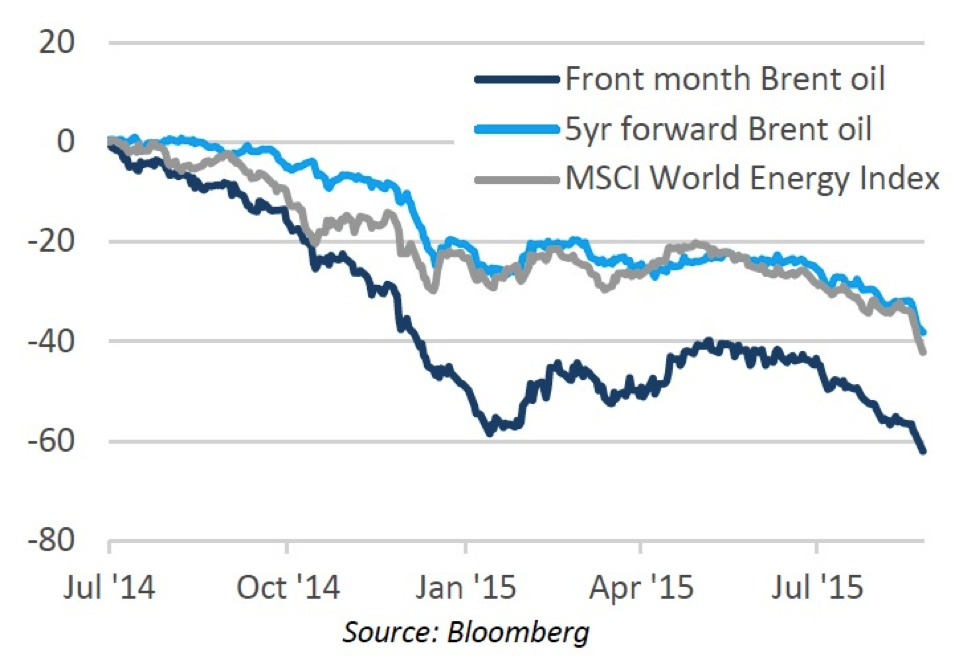

It has been a pretty brutal summer for the energy markets. Brent oil fell from $65 in May to below $40, and the MSCI World Energy Index was down around 25% over the same period, leaving energy as the worst performing sector year-to-date and the most out-of-favour among all the portfolio manager surveys that we see. Long-dated Brent oil has also fallen; having started the year at $78 and traded in a fairly tight $75-$80 range until the end of June, it fell to a low point of just over $60, over 40% off its highs last year.

The reasons for this, in our opinion, are as follows:

- The US production trajectory is still unclear, although we think it is now declining. Monthly US oil production data for April and May showed that production had stopped growing and is starting to trend downwards (month over month). Weekly data (including data up to mid-August) contradicts this somewhat. The weekly data is low quality (but timely) while the monthly data is good quality (but heavily delayed). As we are writing, new monthly oil production data from the EIA for June has been released and it shows a clear downward trend in US oil production (June production was 9,296k b/d versus May 9,400k b/d and April 9,612k b/d). We are still in the eye of the storm for the US, but the trend looks downwards to us – it looks like April 2015 probably was the peak for US oil production.

- The rest of non-OPEC has been relatively steady. Russia has been remarkably robust in terms of production (as the weaker RUB has helped domestic producers) but significant capex cuts across the industry will likely lead to big production declines. We’ve seen 6 million barrels/day of new projects being cancelled in recent months – not impactful in 2015, but these will start to have relevance in 2016/17 in terms of rebalancing the market. $60 oil or less is clearly not sufficient for new projects to be economic in these regions.

- OPEC production has been substantially stronger than expected. This has been a surprise. OPEC was producing 30.6m b/day in December 2014, and has risen by 1.5m b/day to around 32.1m b/day in July 2015, with Saudi production up by 0.9m b/day and Iraq up by 0.7m b/day. These countries are following their market share strategy very firmly. Both Saudi and Iraq are producing at 30yr+ record levels. We question how much spare capacity remains here. In addition, Iran is likely to restart oil exports later this year, and there is a wide range of opinion on what Iran can add to the mix (Iranian oil minister says 1.2m b/day in six months, we think more like 0.5-0.7m b/day in 6 months). Either way, Iran could delay the global rebalancing. There’s also the prospect of Libya returning, although there appears to be no improvement in the political situation at this stage. If Iran and Libya come back, we see little to no spare capacity in OPEC or in the world.

- Concerns over global economic growth (led by China) are driving recent poor performance (both energy sector and the broad market). Despite this, China (representing 10% of world oil demand) is growing oil demand as expected (around 0.5-0.6m b/day in 2015), while the rest of the non-OECD world is robust. US demand is particularly strong. World oil demand growth expectations are being steadily increased (now about 1.6m b/day in 2015, the strongest year since 2010), and will likely trend higher while oil prices should remain low. This is a relief, but not enough to bring balance today, given how strong OPEC production has been.

We can observe these moving parts of the supply/ demand equation for oil, but the question remains: how long does energy equity weakness persist? Answering this with any precision is of course difficult. Energy equities appear to be pricing in around $55 long-term oil prices (on our calculations), while the five-year-forward Brent oil price is around $65/bl. Energy equities will only start to work once Brent oil shows signs of recovering and long-dated Brent oil prices stabilise.

Why have energy equities not followed spot oil prices?

We usually compare energy equities with forward oil prices (as opposed to spot) – correlation is better and absolute percentage changes tally up better over time. This current bear market appears to be no different to what we would have expected, given the move in long-dated prices. The MSCI World Energy Index is down 36.7% from 23rd June 2014 (the oil price peak) to 27th August 2015, while five year forward Brent oil is down by 34.1%. That’s very close in terms of movement, and (as we usually expect) the equities led the commodity price movement at the start of the downturn. We would expect the equities to lead on the way up as well.

On the chart below, five year forward Brent oil has declined broadly in line with the MSCI World Energy Index, and both have outperformed the front month Brent oil price.

What makes Brent oil stabilise?

The market continues to search for signs of a definitive tightening in the balance between oil supply and demand. Most likely it will be a supply sign: either that US shale oil production is in clear decline, or action from OPEC to reduce their supply. There have been rumours of an emergency OPEC meeting. Various members are under economic stress from the low oil price; a number of Middle East countries are raising debt – their budgets are not covered at current oil prices (and barely covered at $75 oil prices). In terms of an oil price floor, we have judged $40 to be the cash cost of supply for the highest cost oil producers today. That cost is gradually coming down, with notable efficiency gains made this year (maybe we are at $35 or so now), but we have touched the cash cost of supply level in August. Historically this has signified the bottom of the oil price cycle, but this could be sustained for a while yet. Seasonal refinery downtime (and recent unplanned downtime) in the US in the third quarter will probably see US crude oil inventories continue to build, though once through this shoulder period, we would expect solid confirmation of US supply declines, limited OPEC growth and some signs that other non-OEPC production growth is starting to slow.

The history of the oil price over its whole life has been dominated by two key factors. First, small imbalances of supply and demand can cause disproportionately large price fluctuations (because short-run price elasticity of demand and supply is very low). But the second key factor is that these can be dampened by the behaviour of one or more large market participants if and when they decide to play a price management role. Standard Oil, the Texas Railroad Commission and the seven sisters have all played this role in the past. Most recently, from 1999-2014, it’s been OPEC who were happy to act as the swing producer.

Shifting to the bigger picture, is there enough world growth to drive demand for oil?

We believe so. We work on the assumption of world oil demand growing, on average, between 1.0 and 1.5m b/day each year. Last year was an exception (as a result of European weakness and China slowdown), with demand rising only 0.7m b/day, while 2015 has seen significant improvements, with demand expectations growing from 1m b/day at the start of 2015 to around 1.6m b/day now. The key driver here has been lower oil prices incentivising consumers to buy bigger, less efficient cars, and to drive greater distances. Fears of China’s recent devaluation causing economic weakness in Asia (and subsequently in the rest of the world) are only partially relevant for oil demand in our opinion. We are concentrating more on driving and transportation dynamics and, as it stands, the world demand outlook remains robust.

Growth in demand for energy has been a key feature of economic progress for 250 years. For 100 years oil has been the key transport fuel because its energy density is unequalled by any other transport fuel. After a spurt in the 1950-70 period as the developed world adopted the motor car, over the last 19 years global oil demand has grown steadily at between 1 and 2% p.a. behind GDP growth. Thus, from 1995 to 2014, oil demand has grown 31% (from 70.3 million b/day to 92 million b/day), or 1.4% p.a., while real global GDP has grown 68.4% (from $44.9tn to $77.5tn, or 2.8% p.a. Over this period oil has mostly been displaced from electricity generation and heating by cheaper alternatives. But its place as transport fuel du jour has not been seriously challenged.

We see no reason for this picture to change much over the next 30 years as the 6 billion non-OECD population raise their standard of living to match those of the OECD’s 1.25 billion inhabitants. We estimate, for example, that the world vehicle fleet is expanding from 1 billion vehicles in 2010 to 2 billion in 2030. None of the current considered projections of electric or gas powered vehicles make a significant dent in this picture. We forecast oil demand in 2035 to be 115 million b/day.

When might supply and demand get squeezed and we begin to see an impact on oil prices?

When OPEC changed its strategy at the end of November 2014, we thought that US unconventional oil supply growth would slow in the middle of 2015. We are now just past the middle of 2015 and the signs are still tentative that this is happening. US supply is one part of the overall mix and the convergence of supply and demand at a global level has been delayed by substantially greater OPEC production (especially Saudi Arabia and Iraq), more robust non-OPEC production outside the US, and upward revisions of historic US oil production levels. Nonetheless, the convergence is coming and, all things being equal, global oil demand will outpace global oil supply in 2H 2016, with global oil inventories peaking at that time. With little or no spare oil production capacity in the world at that time, the global oil inventory overhang will get worked off and oil prices will have to be stronger to incentivise investment in new production.

What will this imply about the upside for equities?

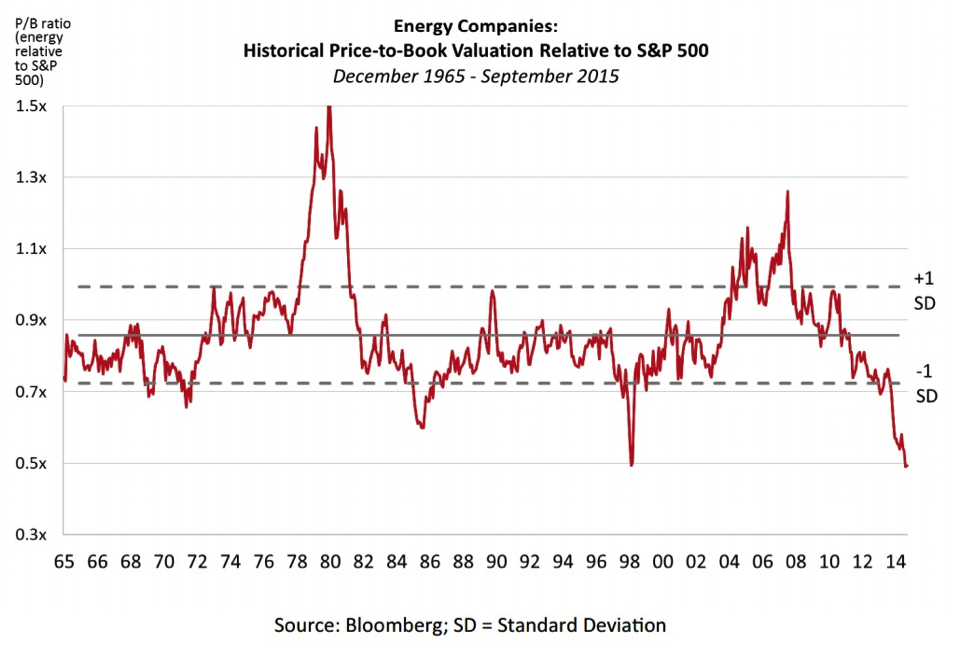

Energy equities are unloved (institutional under-ownership, for example, is at an extreme level) and the sector’s valuation, on some metrics, is at extreme lows. Energy equities will recover when sentiment towards crude oil improves; given the poor sentiment currently, the recovery is likely to be significant. The fall in the long-dated oil price (five year forward Brent oil trading at $65) explains the fall in energy equities; should sentiment in the commodity markets improve, we would expect to see long-dated oil improve as well. As it stands, we believe that energy equities are reflecting an oil price of around $55/bl long-term (based on current cost and taxation assumptions). If the companies deliver further cost control and efficiency gains then the implicit oil price that they are reflecting will be lower than $55/bl. Nonetheless, on current assumptions we see the sector as pretty close to fair value at around $50-55 long-term oil while offering over 25% upside at $65 oil, over 40% upside at $75 oil and over 100% at a long-term oil price of $100.

What is the likely timing of all this playing out?

On the basis of analysis that suggests a rebalancing may not come until the second half of 2016, perhaps it is only 1am. However, there is an important element this analysis overlooks – Saudi behaviour. We believe there is a strong likelihood that when Saudi’s objective is achieved (say evidenced by nine months of successive US production decline, perhaps next March, and signs that global oil inventories are peaking), they will start to manage supply again. At the end of last week, OPEC’s tone shifted somewhat, with the following statement: “Cooperation is and will always remain the key to oil’s future and that is why dialogue among the main stakeholders is so important going forward”; and, “if there is a willingness to face the oil industry’s challenges together, then the prospects for the future have to be a lot better than what everyone involved in the industry has been experiencing over the past nine months or so”. Saudi won’t aim to get the price up to $100/bl immediately, more likely $70-80/bl. On this basis, maybe it is more like 4am, and given equity markets typically are anticipatory by 6-9 months it may even be 5am – the very darkest moment before the dawn.

- The Guinness Atkinson Global Energy team

The Fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The statutory and summary prospectus contains this and other important information about the investment company, and it may be obtained by calling 800-915-6566 or visiting gafunds.com. Read it carefully before investing.

Mutual fund investing involves risk and loss of principal is possible. The Fund invests in foreign securities which will involve greater volatility, political, economic and currency risks and differences in accounting methods. The Fund is non-diversified meaning it concentrates its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. The Fund also invests in smaller companies, which involve additional risks such as limited liquidity and greater volatility. The Fund’s focus on the energy sector to the exclusion of other sectors exposes the Fund to greater market risk and potential monetary losses than if the Fund’s assets were diversified among various sectors. The decline in the prices of energy (oil, gas, electricity) or alternative energy supplies would likely have a negative effect on the fund’s holdings.

MSCI World Energy Index is an unmanaged index composed of more than 1,400 stocks listed on exchanges in the U.S., Europe, Canada, Australia, New Zealand and the Far East. The MSCI World Energy Index is the Energy sector of the MSCI World Index

One cannot invest directly in an index.

Capital expenditure, or CapEx, are funds used by a company to acquire or upgrade physical assets such as property, industrial buildings or equipment.

Correlation is a statistical measure of how two securities move in relation to each other.

Standard & Poor's 5000 (S&P 500) is an index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors. The S&P 500 is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe.

Price to book ratio (P/B Ratio) is a ratio used to compare a stock's market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter's book value per share.

Standard Deviation is a measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is calculated as the square root of variance.

Distributed by Quasar Distributors, LLC.

Opinions expressed are those of Guinness Atkinson Funds, are subject to change, are not guaranteed and should not be considered investment advice.