KEY TAKEAWAYS

· Our new Corporate Beige Book indicates that China remains a primary focus for investors during third quarter earnings season.

· Management commentary suggests China’s economy is not suffering a hard landing and its impact on overall U.S. corporate profits may be minimal.

· Sentiment broadly among management teams that have reported third quarter results so far is pretty upbeat.

According to our new Corporate Beige Book, China has been a popular subject of discussion among corporate management teams this earnings season. Similar to the Federal Reserve’s (Fed) Beige Book, a qualitative assessment of the U.S. economy and each of the 12 Fed districts, conference call transcripts for third quarter 2015 company earnings reports can be used to create a Corporate Beige Book — a window into corporate America. As we do with the Fed’s Beige Book (see the Weekly Economic Commentary, “Beige Book: Window on Main Street”), we believe a Corporate Beige Book can provide useful perspective when interpreted quantitatively by measuring how the descriptors change over time.

CHINA REMAINS IN FOCUS

China has been a primary focus among investors during earnings season. As we highlighted in our earnings preview commentary, between the second and third quarters of 2015, the market received more evidence that the Chinese economy had slowed, bringing it more to the forefront for this reporting season.

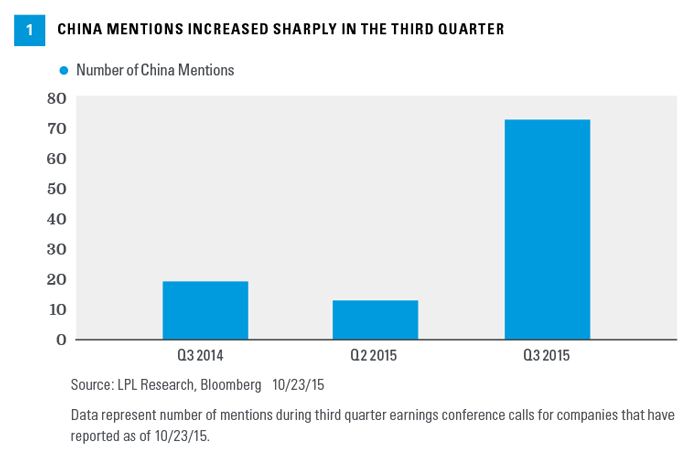

China has been a much more common topic of management conversation during this quarter’s earnings conference calls than in the prior quarter. Figure 1 shows how many times “China” was mentioned during the first one-third of this earnings season, as compared with the same point in time during the reporting seasons for the third quarter of 2014 and second quarter of 2015. Clearly investors are asking more questions about China, and management teams are proactively sharing more insights.

These data points help put China into perspective as an important topic, but shed little light on the business environment there. To assess conditions in China, we can look at comments from various management teams that have discussed China on their earnings conference calls. These comments, listed below, provide a balanced picture of the business environment in China and suggest stability. Two-thirds of the earnings reporting season is still left to go, but we are seeing very little to support the case for a “hard landing” in China.

Consumer

· “While we are very mindful of the macroeconomic volatility in China, our brand has never been stronger and our marketplace has never been more healthy.”

· “Number one, extraordinary volatility in financial markets, the surprise currency devaluation, and overall softer economic conditions are weighing more heavily on the higher ticket casual dining sector in China.”

· “Now, this strong focus on costs has allowed us to step up investments in advertising and trade promotion…and to accelerate our emerging markets business in key countries like China, a market that continues to perform extremely well.”

Financials

· “Turning to the economic environment, the global economy showed some signs of weakness in the third quarter primarily in China and other emerging markets. This weakness impacted the financial markets and the rising value of the U.S. dollar has caused the trade deficit to widen.”

Healthcare

· “Sales outside the U.S. were negatively impacted by softer demand and a reduction in inventory levels, primarily in China.”

Industrials

· “Business for us in China is still pretty good, which is a big market. And so we still see a fair amount of opportunities out there even amongst the volatility.”

· “Sales in China increased 10% for the full year and 7% in the fourth quarter due to new distribution, much of which came from Southern China and ongoing promotional activities throughout the country. We continue to be optimistic about the long-term opportunities in this region although we expect a lot of volatility along the way.”

Materials

· “Demand from China continues to be strong.”

· “China volumes were soft earlier in the quarter, including customer inventory management, but stabilized with demand improvement later in the quarter.”

· “So, we’re optimistic that China will continue to resume its growth. We know the Chinese government is very interested in the economy growing. They’re taking a lot of right moves to have the economic growth.”

Technology

· “So general macroeconomic weakness, it’s pronounced in China, but we see it elsewhere in the enterprise segment being offset by, I’d say, torrid growth rates in cloud computing.”

· “We continued to see solid performance across most developed markets while the challenging macro conditions in Brazil, China, Japan, and Russia persisted this quarter.”

Because of its narrow focus, specialty sector investing, such as healthcare, financials, or energy, will be subject to greater volatility than investing more broadly across many sectors and companies.

These management comments on China paint a mixed picture but not one that is consistent with a significant drop in economic activity, or a hard landing. Some companies did cite slower growth, but many of the comments suggest stability in the Chinese economy and stable business conditions. Based on earnings results thus far, and the fact that China represents less than 5% of S&P 500 profits, we would conclude that, besides the commodity sectors, the slowdown in China is having a limited impact on corporate profits.

We continue to expect China to pull out all the stops to kick-start its economy in the coming weeks and months. Last week, China’s central bank, the People’s Bank of China (PBOC) cut lending rates by 25 basis points (0.25%) and its reserve ratio requirement by 50 basis points (0.50%). The PBOC interest rate cuts, along with selected fiscal and legislative actions in China, should further help to calm fears of a hard landing.

CURRENCY MENTIONS

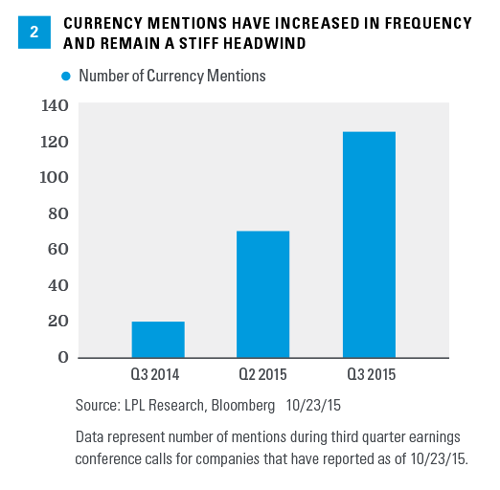

Currency has also been a popular topic during the current earnings season. The strong U.S. dollar was an estimated 3 – 4% drag on S&P 500 profits during the second quarter of 2015 and will be a similar drag during the third quarter. Figure 2 shows a steep ramp-up in the number of currency (or dollar, or foreign exchange) mentions on conference calls since not only last year, when currency was largely a non-factor, but also since last quarter.

Due to the magnitude of the earnings impact, we will continue to look at results with and without currency effects — third quarter earnings growth would likely be tracking toward positive growth (rather than a 2.8% decline, based on Thomson Reuters data) excluding currency effects, even with the 60%-plus drop in energy earnings. Heavy currency drag will almost certainly be with us next quarter, but we expect it may abate beginning in the first quarter of 2016, assuming the U.S. dollar does not move significantly higher between now and then.

Currency risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

ENCOURAGING SENTIMENT READING

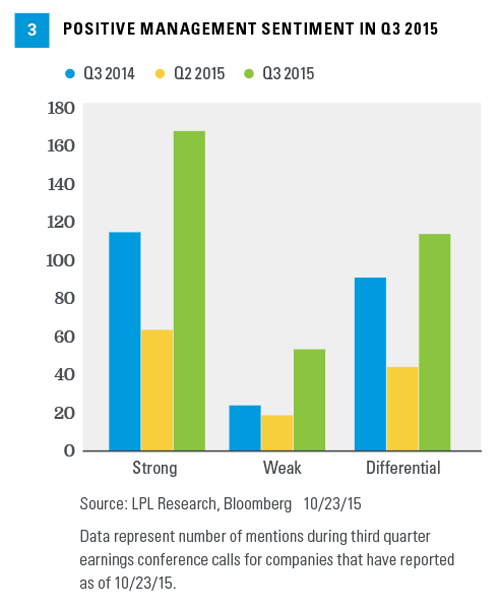

We can also use the conference call transcripts to gauge overall sentiment of corporate management teams as we have done with the Fed’s Beige Book to create our Beige Book Barometer. To do this, we count the number of strong words (or variations of “strong”) and the number of weak words (or variations of “weak”) and calculate the difference between the two. (Examples of strong words include “robust,” “solid,” and “optimistic”; examples of weak words include “weak,” “soft,” and “fragile.”) We can then compare that differential to prior quarters to make comparisons over time. As shown in Figure 3, management sentiment was far more positive during the third quarter of 2015 than it was the prior quarter and also more positive than the third quarter of 2014, before China had become such a widespread concern. We consider this to be an encouraging sign and expect this trend to generally continue throughout the rest of the season.

CONCLUSION

About one-third of the way through third quarter earnings season, our Corporate Beige Book tells us that not only is China a big focus for investors, but it also suggests China’s economy is not suffering a hard landing and its impact on overall U.S. corporate profits may be minimal. More importantly, sentiment among management teams that have reported third quarter results so far is relatively upbeat, which has helped to support the October stock market rally. The headline numbers are not great, but so far the forward-looking market seems to like what it sees out of corporate America. Look for a third quarter earnings season recap in the weeks ahead.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal, and potential liquidity of the investment in a falling market.

All investing involves risk including loss of principal.

INDEX DESCRIPTIONS

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.