Earlier this month, the September housing report showed starts increased 6.5% M-O-M compared to consensus estimates of about 1.5%. Interestingly, this report also shows single-family starts increased only 0.3% M-O-M compared to 17.0% for multi-family starts. And multi-family starts also increased nearly 15% on a year-to-date basis compared to 11% for single-family homes.

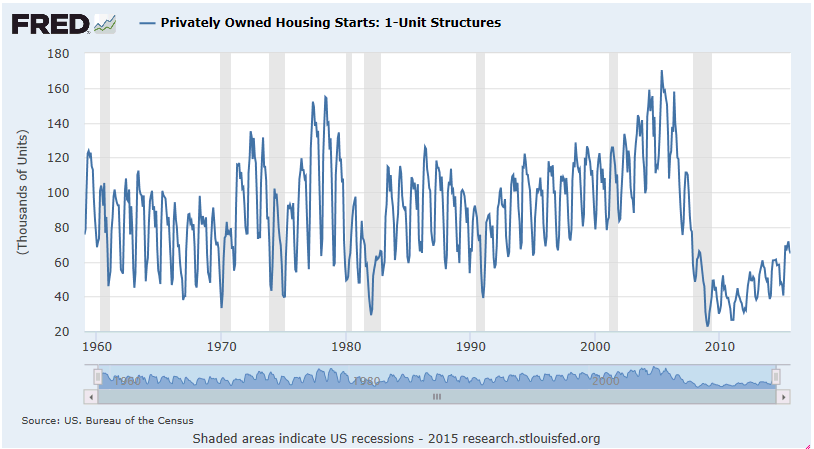

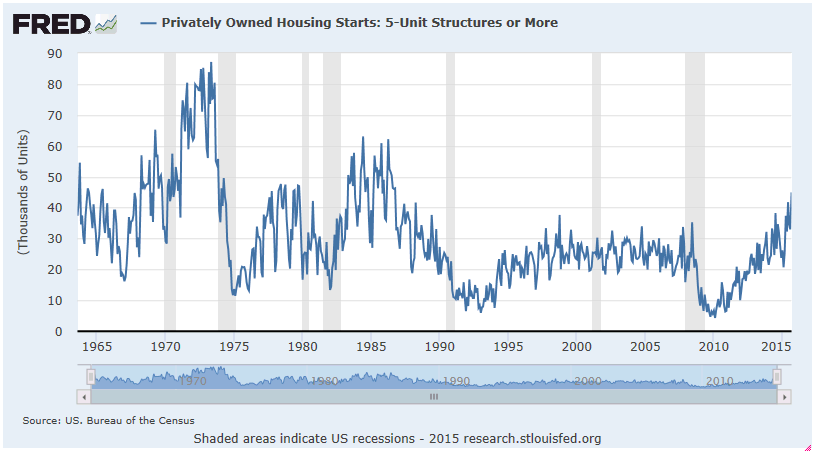

The first graph shows not only the strong rebound for multi-family housing starts since the last recession but also that these starts topped those of the last decade. In comparison, the following graph then shows the lackluster recovery for single-family housing starts.

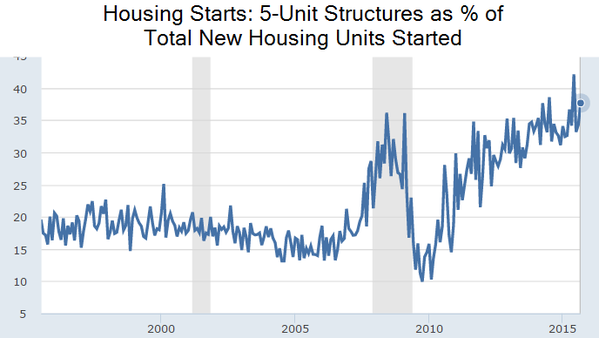

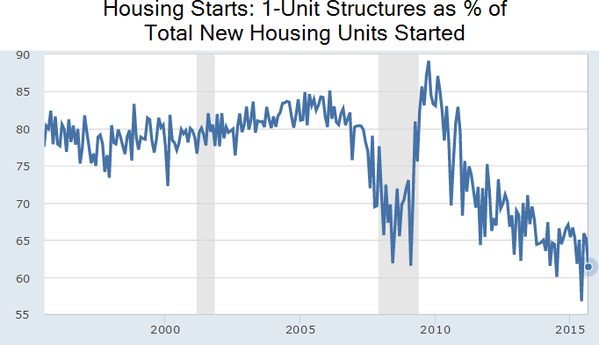

The next two graphs come from “the daily shot” and show the changing mix of multi- family and single family housing starts as a proportion of total housing starts. In our view, the continued strength of multi-family growth reflects the influences of economic and social factors that leads to what we call the rental society not only in housing but also in employment and in other sectors. But before outlining our basis for that conclusion, we thought it important to review again the overall importance of housing to U.S. economic growth.

Source: St Louis Fed

Source: St Louis Fed

Housing Holds Back GDP Recovery

After most recessions, housing and autos spark the initial recovery. Autos played its role. Housing did not. In 2014, residential fixed investment (RFI) accounted for just over 3% of GDP compared to an average of 4.5% over the last 45 years. While that reflects a small share of GDP, RFI can contribute an important share of GDP growth during a recovery. At times in the past, RFI contributed 15-20% of annual GDP growth. Because GDP accelerated last year, RFI contributed just 2% of GDP growth. And in dollars, at its peak in the last decade—2005—the annual value of single family housing construction totaled approximately $525 billion. Last year, the comparable figured showed a total of $192 billion. These two numbers clearly picture what the economy lost in actual spending. If that modest contribution from housing continues, GDP growth will likely remain lethargic.

The Rental Society

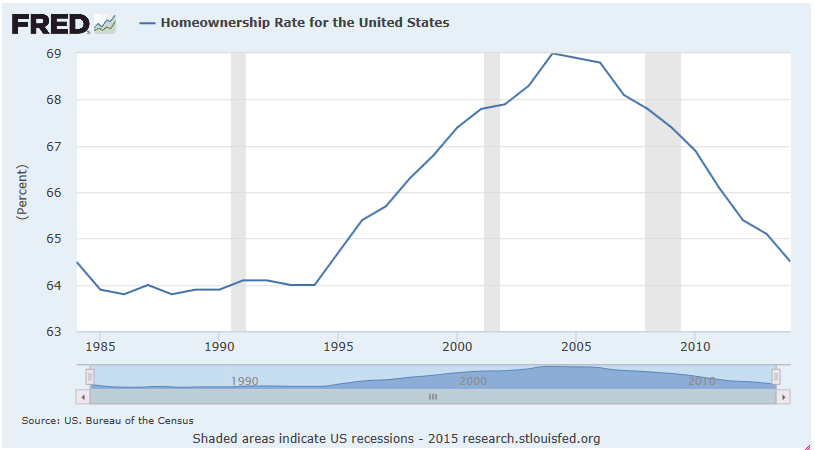

Declining Rate of Single Family Homeownership—Some Influences

The graph above shows the declining rate of home ownership in the United States. Since its peak in 2006, home ownership declined over 1.7 million households. This graph may overstate the peak rate of homeownership since those who bought their homes with little or no equity at the peak, using sub-prime mortgages, for all practical purposes, rented their homes.

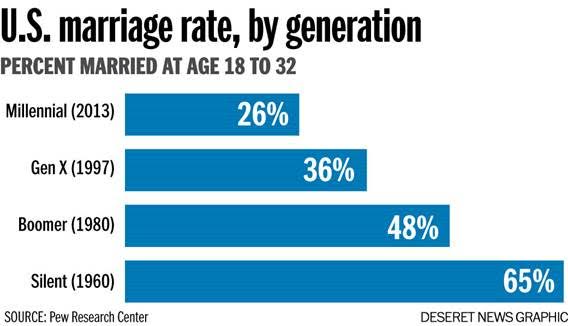

Our July 2013 commentary (at our prior firm) looked for the development of a rental society. In that commentary we wrote: “Our conclusion, rentals rather than home buying will benefit from this witches’ brew of long-term uncertainties facing new home buyers. It will also delay when they will marry (see chart below). In this great circle of life cycle variables, this delay will add another reason to push off buying a house.”

We would add that the growing level of student loans adds a further burden that delays millennials from moving on to the next stage in their life cycle—such as marriage (see graph below)—and then homeownership. The average student loan outstanding for the 43 million borrowers reaches nearly $27,000.

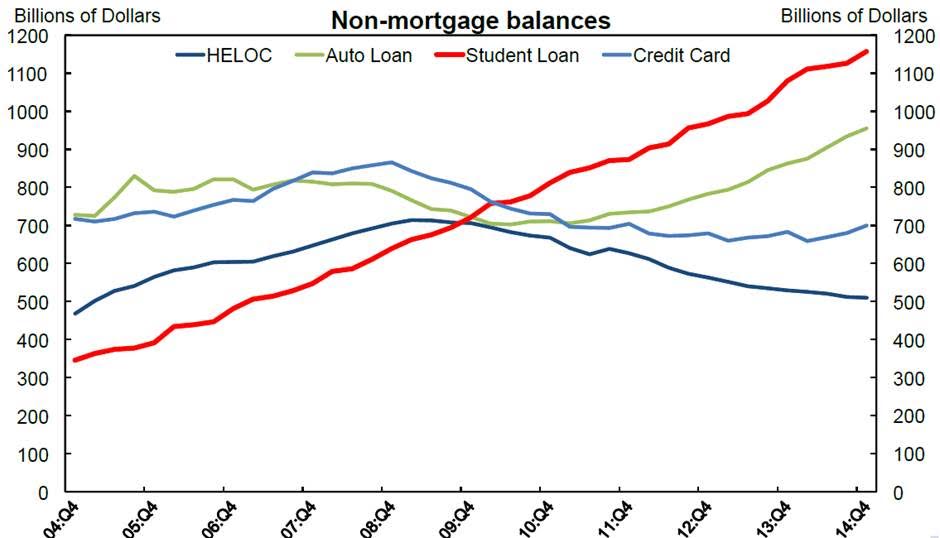

SOURCE: FEDERAL RESERVE BANK OF NEW YORK

The key to stimulating greater strength in the housing market will be the return of first-time home buyers. Without their return, the housing market simply becomes a game of musical chairs. Normally, first-time home buyers comprise about 40% of the market and that rate reached a peak of 50% in 2009. Since that peak, their share declined and most recently, in September, stood at 29%. The factors referred to above, as well as the decline in real median household income since the beginning of the recession, makes it difficult to expect a significant increase in first-time buyers.

Finally in that 2013 commentary, we wrote: “The net result will be a continued increase in multi-family house construction for rentals and a decline in the rate of home ownership.” We still expect that trend to continue for the near future. And even multi-family construction shows a shift to rentals. In 2014, more than 90% of multi-family unit starts went to the rental market. In comparison, in the last decade, rentals comprised 60% of multi-family starts.

Rental Society More Than Homes—Renting Workers and Things

Rental Society—Renting Workers

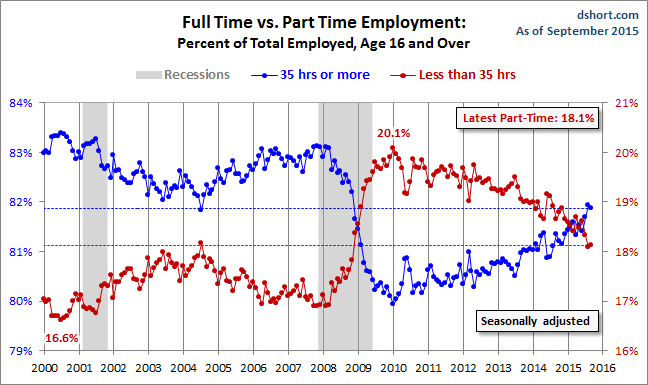

The so-called great recession led to a substantial increase in part-time employment—or what we call renting workers. The number of part-time or rental workers remains substantially higher than the level before the last recession (see next graph).

The following graph further shows the sharp growth in the percentage of part-time or rental employment since the onset of the great recession. Part time or rental employment peaked at roughly 20% of full-time employment in 2010. That rate compares to under 14% in 1968. Since that peak in 2010, the percentage of part-time or rental employment shows only a modest decline. The key question remains, how much of this change reflects the slow recovery as opposed to structural change.

SOURCE: dshort.com-ADVISOR PERSPECTIVES

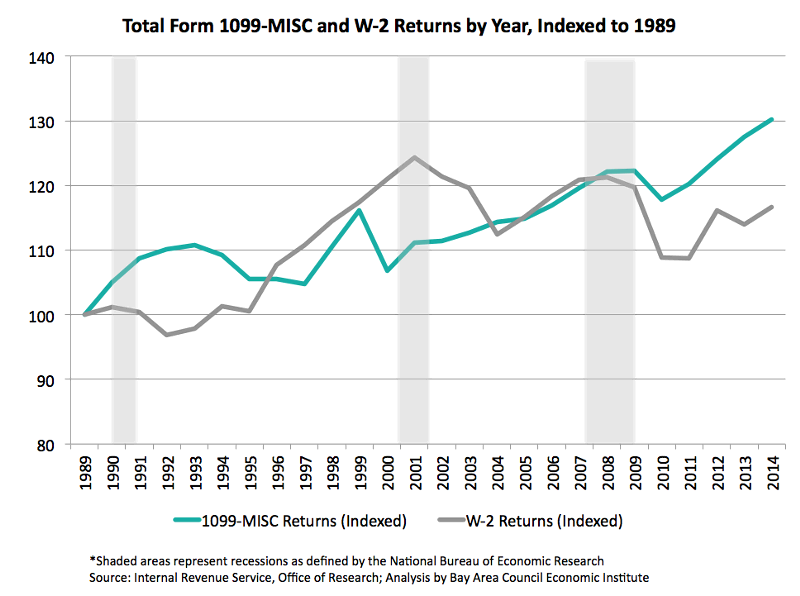

Rental Society—Renting Contractors—the “Gig” Economy

The “uberization” of the taxi industry broadened itself out to renting contractors. And it must have been a former jazz musician that labelled it the “gig” economy. The number of rented contractors in the so called “gig” economy cannot easily be determined. Some observers gauge its potential size by the number of 1099s. The next graph shows the growth in 1099s vs W-2s indexed to 1989. The graph shows the meaningful growth in the number of 1099s began to show up during the recession at the beginning of the last decade. At the same time, that recession marked the peak in the number of W-2s issued. Since then, the number of W-2s issued remains below that peak. And this decline occurred while both the potential working population and 1099s increased.

Note: businesses paying at least $600 to independent contractors and other businesses must file a 1099 form.

Rental Society: Renting Cars and Things—the Monthly Rental Payment

Strong auto sales helped propel the economic recovery. In part, this strength resulted from the increasing use of leasing/renting to finance mid-priced cars. Today, leasing/renting accounts for 27% of car sales compared to 15-20% before the recession. And before the recession, leasing/renting activity focused primarily on luxury vehicles. And now, for example, about one-third of mini brand sales come from leases. Your friendly new car dealer will lease/rent mid-priced cars for just $199/month.

Not only autos but recently smart phones went to monthly rentals. The telephone companies, as well as Apple, heavily marketed renting your smart phone separately from the cost of the wireless service. More and more “things” will be rented with the growth of the rental society. In the growing rental society, consumers focus on monthly rental payments rather than total cost.

For investors, one example how the rental society of things can benefit companies shows up in auto retailing. In three to four years, increased leasing/rental of mid-priced cars will provide substantial low cost “raw material” for used car lots. Publicly owned car dealers, that run many of these used car lots, will profit. And there will be many more examples.

The Rental Society—Consequences—Investment Implications

If the rental society in housing continues at the expense of single home construction, then economic growth, at best, will remain at its current modest growth levels. This shortage of growth will bring higher multiple valuations to the benefit of those companies that can demonstrate consistent above average growth in a low growth economic environment. I am sure readers could list many more.

The Rental Society—Other Implications

If the United States moves to a greater rental rather than ownership society, it could bring substantial unintended consequences and other changes. The psychology of renting differs from owning. This effects not only the upkeep of assets rented instead of owned, but also could dramatically affect local communities. Renters rather than owners will likely be less involved in community affairs and perhaps school activities. And this just cites one example of the possible implications.

- Andrew J. Melnick, Chief Investment Strategist, BPV Capital Management