Normally, analysts’ projections diverge somewhat around a statistical norm. That is, it’s usual for a group of 40 analysts to project the upcoming quarterly GDP growth rate between 1% and 3%. Currently, however, there is a fair degree of uniformity among analysts regarding the outlook. And that’s not a good sign. From the Financial Times:

Instead, the gap between optimists and pessimists is close to all-time lows. The standard deviation of forecasts for the US, UK, eurozone and Japan are all close to their lows, according to Consensus Economics (see chart). For Europe, slow growth helps narrow the gap, but even so it is surprising to see such a clustering of predictions.

When economists have all thought the same thing in the past it has usually been a sign of trouble ahead: 2007, 2011 when investors wrongly thought the eurozone problems were past, just before the Asian crisis in 1997. In Japan, economists herded into a narrow range of forecasts just before last year’s recession, while in the US they were in close agreement (and wrong) at the end of 2013, when bond yields had soared to 3 per cent, a level not seen since.

Obviously, this is no guarantee that the global economy is headed for trouble. But it does indicate that, given the incoming data, there are fewer conclusions that can be drawn. And that’s what’s really concerning.

In a bid to hit its 7% GDP growth forecast, China officially threw the kitchen sink at its economy this week:

China’s central bank cut its benchmark lending rate and reserve requirements for banks, stepping up efforts to cushion a deepening economic slowdown.

The one-year lending rate will drop to 4.35 percent from 4.6 percent effective Saturday the People’s Bank of China said on its website on Friday. The one-year deposit rate will fall to 1.5 percent from 1.75 percent.

Reserve requirements for all banks were cut by 50 basis points, with an extra 50 basis point reduction for some institutions. The PBOC also scrapped a deposit-rate ceiling.

All three moves, announced Friday, demonstrate that the Chinese political hierarchy is deeply concerned about the state of the economy. The 6.9% 3Q growth rate announced on Monday surely spurred them into action. Fixed investment increased 10.3% for the first three quarters of 2015 – the slowest pace since 2000. Real estate investment was up 2.6% for the same period. Other statistics released this week add to the concern. Y/Y industrial production rose 5.7% and retail sales gained 10.8%. Both of this coincidental indicators continue their 5 year downward trend:

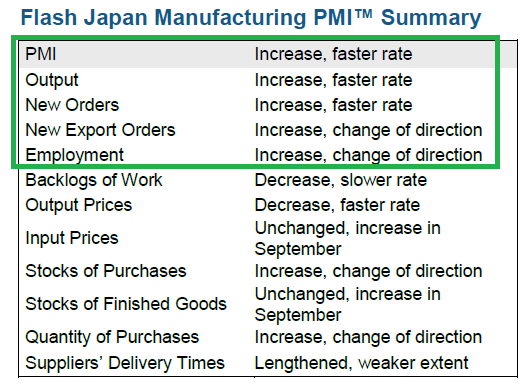

With the exception of the Flash Markit number, Japanese news was bearish. Exports increased a paltry .6% Y/Y. This dovetails with the latest BOJ Minutes, which describe the international trade situation as weak:

Exports had recently been more or less flat, due mainly to the effects of the slowdown in emerging economies. The background to such recent developments in exports -- which had been picking up since last winter -- was stagnant trade and production activity worldwide amid the slowdown in emerging economies, including China, and commodity-exporting economies, as well as weak IT-related demand. Exports were expected to remain more or less flat for the time being, but subsequently were likely to increase moderately, as emerging economies moved out of their deceleration phase.

Imports slumped 11.1%. The weak yen is partially responsible for the drop, but not entirely. Leading indicators declined .9% while coincident numbers fell 1.5%. The only good numbers came from Markit, where the headline Flash number (52.5) printed its highest level in a 1 ½ years. More importantly, all the sub-indexes shows improvement:

The latest minutes also highlighted the potential growth in the industrial sector:

Business fixed investment had been on a moderate increasing trend as corporate profits continued to improve markedly. Looking at corporate profits in the Financial Statements Statistics of Corporations by Industry, Quarterly, current profits had seen a sharp quarter-on-quarter increase in the April-June quarter of 2015, and the ratio of current profits to sales had posted a record-high level. The aggregate supply of capital goods (excluding transport equipment) -- a coincident indicator of machinery investment -- had been trending moderately upward, albeit with fluctuations. Looking at leading indicators, machinery orders (private sector, excluding orders for ships and those from electric power companies) had registered a quarter-on-quarter increase for four quarters in a row since the July-September quarter of 2014, but had dipped recently. Construction starts (floor area, private, nondwelling use) had picked up, albeit with fluctuations, since the turn of the year. Business fixed investment was projected to continue increasing moderately as corporate profits followed their marked improving trend.

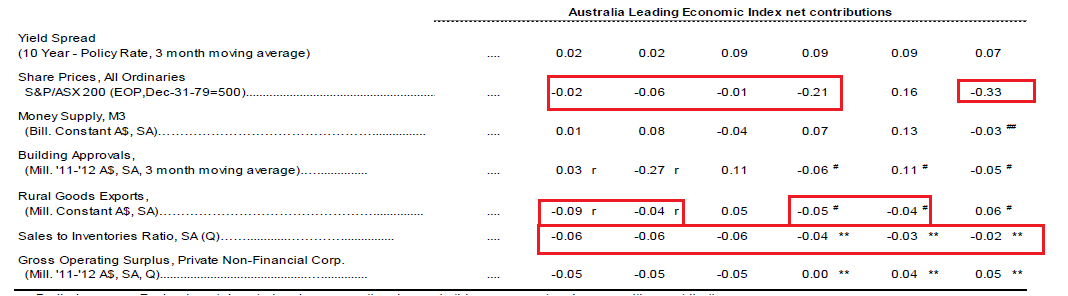

The Reserve Bank of Australia released their latest meeting minutes last week. Regarding the international environment, they noted the Asian slowdown, which centered on China. Japan – another big trading partner – was mixed, with weak GDP growth but low unemployment. As for the domestic economy, moderate consumption growth continued. While mining was declining, services were up. Overall, the picture continues to be an economy poised for moderate growth. The Conference Board released the latest leading indicators, which declined for the fifth time in seven months. The sales/inventory ratios, shares prices and rural goods exports have all subtracted from growth for a majority of the last six months:

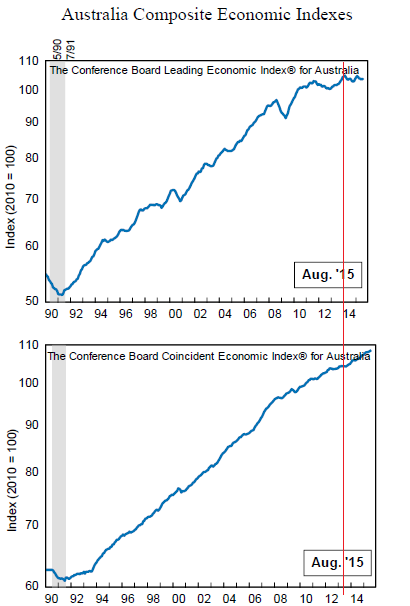

Yet, the coincident indicators continue moving higher:

LEIs are designed to telegraph movement six to nine months in advance. Under that criteria, the CBs LEIs may need some fine tuning.

The Bank of Canada maintained rates at .5%, offering the following analysis with their policy release:

Total CPI inflation remains near the bottom of the Bank’s target range, owing to declines in consumer energy prices. Core inflation is close to 2 per cent as the transitory effects of the past depreciation of the Canadian dollar are roughly offsetting disinflationary pressures from economic slack, which has increased this year. The Bank judges that the underlying trend in inflation continues to be about 1.5 to 1.7 per cent.

.....

Canada’s economy has rebounded, as projected in July. In non-resource sectors, the looked-for signs of strength are more evident, supported by the stimulative effects of previous monetary policy actions and past depreciation of the Canadian dollar. Household spending continues to underpin economic activity and is expected to grow at a moderate pace over the projection period. However, lower prices for oil and other commodities since the summer have further lowered Canada’s terms of trade and are dampening business investment and exports in the resource sector. This has led to a modest downward revision to the Bank’s growth forecast for 2016 and 2017.

Canadian inflation experience compares to most developed countries: weak energy prices are keeping total prices below core. The latest CPI Y/Y reading of 1% supports the bank's analysis. However, the broader negative impact of low oil prices on the Canadian economy continues: exports are down and business investment is weak. While the economy grew in July, this was only a one month rebound from a technical recession in 1H15. However, the .5% M/M retail sales increase – the fourth in a row – could be a harbinger of an overall turnaround. The number was flat outside of car sales, but the strong increase in that sub-index indicates two things: decent consumer confidence and the positive impact of the Bank of Canada’s rate cut a few months ago winding through the economy.

The ECB kept rates unchanged and maintained their current asset purchasing policy. The biggest part of Draghi’s speech was this passage:

The Governing Council has been closely monitoring incoming information since our meeting in early September. While euro area domestic demand remains resilient, concerns over growth prospects in emerging markets and possible repercussions for the economy from developments in financial and commodity markets continue to signal downside risks to the outlook for growth and inflation. Most notably, the strength and persistence of the factors that are currently slowing the return of inflation to levels below, but close to, 2% in the medium term require thorough analysis. In this context, the degree of monetary policy accommodation will need to be re-examined at our December monetary policy meeting, when the new Eurosystem staff macroeconomic projections will be available. The Governing Council is willing and able to act by using all the instruments available within its mandate if warranted in order to maintain an appropriate degree of monetary accommodation. In particular, the Governing Council recalls that the asset purchase programme provides sufficient flexibility in terms of adjusting its size, composition and duration. In the meantime, we will continue to fully implement the monthly asset purchases of €60 billion. These purchases are intended to run until the end of September 2016, or beyond, if necessary, and, in any case, until we see a sustained adjustment in the path of inflation that is consistent with our aim of achieving inflation rates below, but close to, 2% over the medium term.

For the last year, central banks viewed weak CPI numbers as transitory; once oil prices increase, so too will total inflation. But what if oil prices specifically and commodities in general continue to be weak for several years? In that case deflationary pressures may become entrenched, putting additional pressure on banks to stimulate inflation. The ECB clearly believes they must acknowledge this possibility. The markets viewed these comments as dovish. Most importantly, they could indicate an important change in the way developed market central banks consider inflation, especially as it relates to the commodity super-cycle ending. In other news, the Markit flash composite for the region increased to 54, with a services number of 54.2 and manufacturing total of 52. Output, new orders and employment for both sectors was positive. However, manufacturing is weakening a bit, largely due to the emerging market slowdown.

There is clearly a change in the analytical winds over the last few months. Participants replaced their guarded optimism with concern for the next few quarters. The Chinese slowdown started the process, and the drop in emerging market currencies accelerated the trend. Now with the ECB acknowledging the potential need for additional stimulus, a new, more bearish outlook is the norm.