The US Bond Market: A Welcome "Nonstory" During August's Turmoil

SUMMARY

- The August stock market turmoil was sparked not by the expected risk of inflation and rising rates, but by concerns over sluggish global growth.

- Losses and volatility in most fixed-income sectors in August were modest relative to stocks.

- Bond liquidity held up relatively well, as fixed-income funds had net redemptions but no large-scale exodus of investors.

- Concerns over dealer bond inventories appear misplaced. Their inventories have always been small relative to the market, and institutional buyers have stepped up when prices have fallen.

Fans of the "Jurassic Park" movie from years ago probably recall the scene where the hunter is staring intently at a raptor in the bushes ahead of him. However, the hunter’s undoing doesn't come from the risk he is watching, but from the raptor that lunges at him from the side. Much in that fashion, the turmoil that racked the financial markets in August wasn't sparked by the risk most were focused on – rising interest rates to head off potential inflation – but by concerns over sluggish global growth and deflation.

China's surprise move on August 10 to devalue the yuan, accompanied by fears of a greater-than-expected slowdown in the country's growth, was the spark. The S&P 500 soon tanked, giving up 11% during seven trading days starting on August 17, and the VIX (a measure of volatility based on equity options pricing) spiked to over 40 – almost three times its 60-day moving average. Researchers at the IMF have defined the start of "risk-off" episodes to be when the VIX trades at 10% above its 60-day moving average, so August’s tumult clearly qualifies. In keeping with the risk-off "flight-to-quality" tradition, yields on the 10-year U.S. Treasury note fell 28 basis points to 2.01% from the end of July to August 21, after which it rebounded slightly to 2.14% and ended the quarter at 2.04%.

Other than the emerging-market sector, the reaction by the bond market was notable largely for what did not occur. Bond mutual funds have grown significantly in recent years, and there have been concerns that fund shareholders might stampede for the exits at the first sign of trouble. We did see a pickup in net redemptions by bond fund shareholders, but nothing like a major exodus. For all bond fund categories the net outflow was 0.9% in August, a modest uptick, compared with net withdrawals of 0.2% in June and July, according to Morningstar. Over the quarter, net outflows were slightly higher for below-investment-grade categories than for bond funds as a whole.

In general, bond liquidity remained sufficient

A related concern has been whether liquidity in various fixed-income sectors would be sufficient to enable fund managers to meet possible shareholder redemptions. As I noted in my second-quarter report, we are in a period of elevated liquidity costs, where volatility can result in prices gapping up and down. At the same time, history has shown that there is likely to be a clearing price for fixed-income assets, thus reducing the risk of not meeting shareholder redemptions.

In this respect, the experience of Eaton Vance’s trading desks in August was not a surprise. Most sectors in the U.S. bond market had relatively low volatility, with one exception – the energy sector, which sold off over low oil prices and sluggish global growth. For similar reasons, emerging-market (EM) bonds experienced the biggest price decline and had the greatest volatility among fixed-income categories. Overall, however, the bond market functioned relatively well in the risk-off month of August – it did its job in reflecting relative value among sectors, without indiscriminate, across-the-board selling.

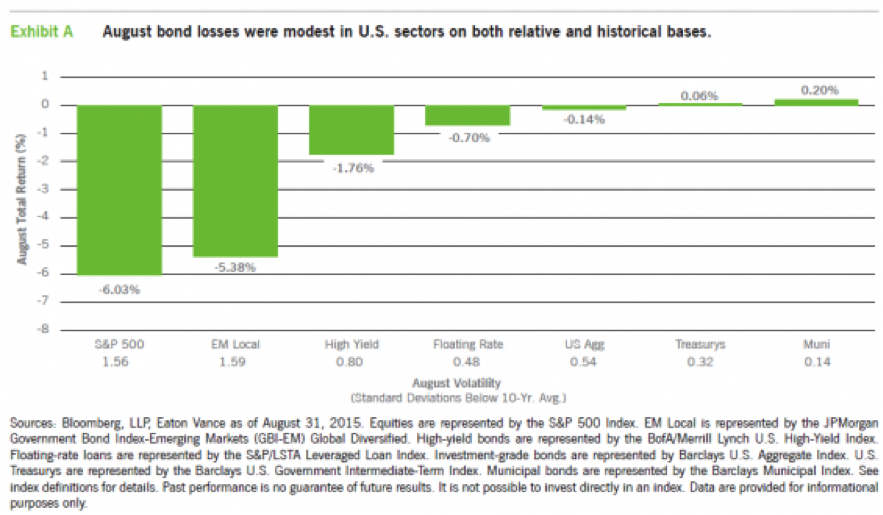

Volatility was modest in most sectors

There will inevitably be episodes that stress the markets further, particularly with the rising rate scenario looming. But from our perspective, the August risk-off episode underscored our belief that the bond market is fundamentally sound. The August performance shown in Exhibit A bears this out. In terms of total return, the overall investment-grade bond market, represented by the Barclays U.S. Aggregate Index, lost just 0.14% versus a 6.03% drop for the S&P 500. Sectors with more corporate credit risk, like high-yield and floating-rate loans, fell a little more.

Municipal bonds managed a gain of 0.20%. Based on a straightforward comparison of absolute returns, these bonds followed their historical pattern of being less volatile than stocks.

But there are two related questions that the horizontal axis of Exhibit A addresses. Bonds were less volatile than stocks, but how much less so? Were they more or less of a safe harbor, relative to stocks, than other periods? The standard deviation figures show that bonds were more of a safe harbor this time around.

To see this, consider that the 10-year average monthly return of the S&P 500 is 0.67%, and its monthly standard deviation over the period was 4.29%; thus, its loss of 6.03% in August was 1.56 standard deviations below the average return. Compare that, for example, with floating-rate loans. Their 10-year monthly standard deviation of 2.33% is about 200 basis points (bps) lower than stocks, meaning that on average, it is a less volatile sector. But in August, the return of floating-rate loans was just 0.48 standard deviations lower than its 10-year monthly average of 0.42%, versus 1.56 lower for stocks. So, in August loans were less volatile versus stocks than they have been historically.

Another nonstory: dealer inventories

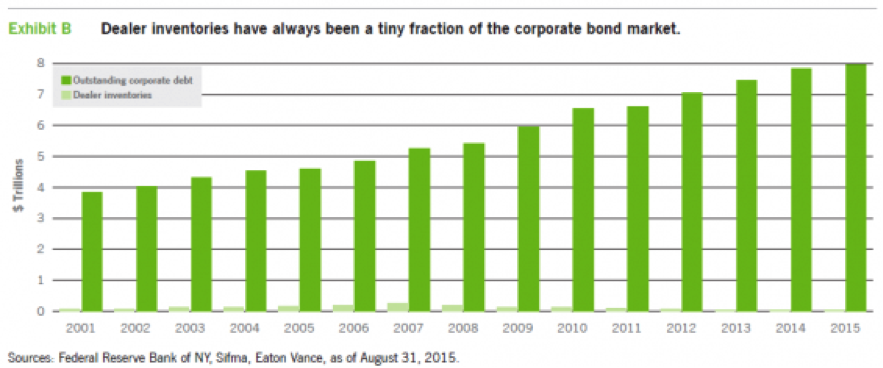

Looking to potential future volatility episodes, the most publicized one has been the potential impact of rising-rates, and whether there will be sufficient liquidity in this scenario. A concern that has garnered much attention is the fact that post-crisis reforms such as the Dodd-Frank Act and the Volcker Rule have increased capital charges for banks, which have made holding bond inventories more expensive. This has led to a significant reduction in bond dealer inventories, pegged by the SEC as a drop of more than 75% since the precrisis period. Traditionally, the willingness of dealers to make markets by holding inventories of fixed-income securities provided investors with a source of initial liquidity.

We believe that concerns over smaller dealer inventories are misplaced. As Exhibit B shows, dealer inventories have historically been a very small percentage of outstanding corporate debt – not enough to hold off significant selling pressure for very long. In the financial crisis years of 2007 and 2008, dealer inventories of corporate bonds averaged $227 billion – twice their average level over the past 15 years.

Nevertheless, as I discussed in my second-quarter commentary, it became clear at the outset of the crisis that dealers had become less willing to continue making markets using their balance sheets, and liquidity would have to come from other buy-side investors (e.g., hedge funds and institutional investors). With the aid of some emergency action, other investors did step in, and within a year from the trough in prices for high-yield bonds and floating-rate loans, both markets regained all lost ground. Market participants understood that elevated liquidity costs and higher market volatility created unique buying opportunities for assets whose intrinsic values were well above their current market prices.

In 2013, when the market was concerned about rising rates in the so-called “taper tantrum,” the pattern was similar. After a sell-off, longer-term buyers stepped up to buy investment-grade bonds and the sector recouped its losses in a year. What about the next sell-off? A fixed-income head at a major U.S. insurance company told Bloomberg News: “If we get another situation similar to that taper tantrum … it starts to shift from a challenge to an opportunity.”

The prospect of a rising rate environment can understandably prompt a degree of anxiety among bond investors, and clearly the expansion of fixed-income mutual fund ownership adds the potential for greater short-term volatility. But with a great deal of cash on the sidelines, we believe other investors will seek to “leg in” to generate attractive risk-adjusted returns over the longer term and provide a buffer.

As a further example, The Wall Street Journal reported in August that corporations have become major investors in each other’s debt – Apple was noted for having about half of its $203 billion worth of its investments in corporate bonds. This is significant because major U.S. companies represent a new potential source of institutional demand that was not present at this scale in earlier interest-rate cycles.

Y2K redux?

For us, the hand-wringing over dealer inventories and liquidity when the Fed raises rates is reminiscent of the “Y2K” scare. Y2K ended up being an example of how misinformation can lead to a large-scale misestimation of risk. Bond investors should focus on the raptors most likely to bite.

Index Definitions

BofA/Merrill Lynch U.S. High Yield Index is an unmanaged index of below-investment-grade U.S. corporate bonds.

S&P/LSTA Leveraged Loan Index is an unmanaged index of the institutional leveraged loan market.

JPMorgan Government Bond Index - Emerging Markets Global Diversified (GBI-EM) is an unmanaged index of local currency bonds with maturities of more than one year issued by emerging-market governments.

Barclays Municipal Bond Index is an unmanaged index of municipal bonds traded in the U.S.

Barclays U.S. Aggregate Index is an unmanaged index of domestic investment-grade bonds, including corporate, government and mortgage-backed securities.

Barclays U.S. Government Intermediate-Term Index is an unmanaged index of U.S. government bonds with intermediate-term maturities.

BofA Merrill Lynch Indexes: BofA Merrill Lynch™ indexes not for redistribution or other uses; provided “as is,” without warranties, and with no liability. Eaton Vance has prepared this report, BofA/Merrill Lynch does not endorse it, or guarantee, review, or endorse Eaton Vance’s products.

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent the past or future performance.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. As interest rates rise, the value of certain income investments is likely to decline. An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Investments involving higher risk do not necessarily mean higher return potential. Diversification cannot ensure a profit or eliminate the risk of loss. Elements of this commentary include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risk and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging-market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown, such as municipal and investment-grade bonds, carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum.

Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, excepting U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

Important Information and Disclosure

This material is presented for informational and illustrative purposes only as the views and opinions of Eaton Vance as of the date hereof. It should not be construed as investment advice, a recommendation to purchase or sell specific securities, or to adopt any particular investment strategy. This material has been prepared on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and Eaton Vance has not sought to independently verify information taken from public and third-party sources. Any current investment views and opinions/analyses expressed constitute judgments as of the date of this material and are subject to change at any time without notice. Different views may be expressed based on different investment styles, objectives, opinions or philosophies. This material may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions. Actual portfolio holdings will vary for each client.

Investing entails risks and there can be no assurance that Eaton Vance, or its affiliates, will achieve profits or avoid incurring losses. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com