Weighing the Week Ahead: Can Strong Housing Data Give An "All Clear" Signal for the U.S. Economy?

It is a very unusual week for data, with many of the major housing reports on tap and not much else. China’s GDP will be a big story over the weekend, and important earnings news will continue. Despite this, pundits will turn their attention to housing, asking:

Can a housing rebound signal “all clear” for the U.S. economy?

Prior Theme Recap

In my last WTWA I predicted that the story would be all about earnings, with a special focus on implications for the economy and prospects for 2016. Given the light economic calendar and the importance of this earnings season, it was an easy choice. It was a winning week for stocks, based mostly on Thursday’s big gains. To get the full weekly story, let us look at Doug Short’s weekly chart. This one saves more than a thousand words! (With the ever-increasing effects from foreign markets, you should also add Doug’s World Markets Weekend Update to your reading list).

While I take a weekly focus, Doug’s update provides multi-year context. See his full post for more excellent charts and analysis.

We would all like to know the direction of the market in advance. Good luck with that! Second best is planning what to look for and how to react. That is the purpose of considering possible themes for the week ahead. You can make your own predictions in the comments.

This Week’s Theme

We have an unusually thin economic calendar, with many of the key housing reports in a single week. This should get some attention despite the earnings news.

Housing is important both as a reflection of consumer behavior (concurrent) and also as a driver of economic growth (leading). It is especially interesting since it is not related to the Chinese economy on first-order effects. As usual, there is a very wide range of viewpoints.

- We are in the midst of another housing bubble

- Prices are crazy in some markets but attractive in others

- Artificially low interest rates are spurring some demand

- Housing is in a long, slow recovery

- Demographics are driving a new round of demand, construction, and economic growth

The week will also emphasize earnings reports. By the time you read this, I could also be completely wrong on the theme because of GDP news from China. The market may react to a “six handle” on the report (growth below 7%). Two CNBC anchors discussed this on Friday. One noted the many and varied reasons that the Chinese effect might be overstated. (See Kraneshares for an excellent report on this). The other replied, “The market doesn’t care about that.”

China might well be the story, at least for Monday.

As always, I have my own ideas in today’s conclusion. But first, let us do our regular update of the last week’s news and data. Readers, especially those new to this series, will benefit from reading the background information.

Last Week’s Data

Each week I break down events into good and bad. Often there is “ugly” and on rare occasion something really good. My working definition of “good” has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially – no politics.

- It is better than expectations.

The Good

There was a fair amount of good news and data.

- Options traders lean short. Dana Lyons notes the high level of bearish put activity, despite the recent rally. This is typically a good contrarian signal.

- The U.S. budget deficit hit the lowest point since 2007. (MarketWatch).

- The misery index a popular measure of the economy in the Carter and Reagan eras, is at a 59-year low. Rex Nutting notes that people are still miserable, wondering if a new measure is needed.

- Inflation remained low, falling on the headline numbers for both PPI and CPI. Low inflation permits more aggressive Fed policy aimed at employment growth.

- Weekly jobless claims remained at record low levels – the lowest in 42 years as reported by Eddy Elfenbein.

- Michigan sentiment showed a solid rebound to 92.1 from 87.2 last month. This is generally correlated with job growth and better spending. No one describes this better than Doug Short, who shows the data history, recessions, GDP, and important call-outs in a single chart.

- Retail sales grew slightly. Some sources regarded the data as a miss, but others noted that the declines were mostly at gasoline stations. As usual, Steven Hansen looks at unadjusted data in various time frames, doing an excellent job of sorting through the complexity.

The Bad

There was also some negative data, including some of the important earnings stories.

- Earnings news. The story was mixed, but I am giving it a slight negative score for our purposes. The beat rate versus dramatically lowered expectations is very solid. Revenue beats are much worse, as noted by earnings expert Brian Gilmartin. Brian is still optimistic about next year, but remains cautious. The anecdotal reports from Avondale (a helpful source) also had a bearish tone.

- Philly Fed missed expectations and turned negative. Bespoke has the overall index results as well as analysis of subsectors, including this key chart:

- Job openings are slightly lower. The quit rate was about the same. (Calculated Risk)

- LA Port traffic declined. Both inbound and outbound traffic are down 0.6% versus August’s year-over year numbers. (Calculated Risk)

The Ugly

Social Security benefit hike? Not this year. Social Security benefits are indexed to the CPI for urban workers. It is not based upon the less volatile core, a controversial measure, but instead uses the year-over-year change. This year the decline in energy prices has kept the CPI near zero. While these prices affect many consumption items I will venture a guess that it is less important for seniors. Meanwhile, Scott Grannis notes that inflation is likely to resume the recent 2% trend, probably next year. Adding to the problem, Medicare premiums will move higher.

There is no easy solution to this problem, but at least the lag is only a year. Before indexation was adopted in the 70’s, benefits were adjusted only by revisions in the law. After about 40 years, it may be time to revisit the methodology.

See also the St. Louis Fed on predicting oil price impacts, the SSA on this history of automatic increases, and the entire history with great charts from Doug Short.

Noteworthy

People in financial media overestimate the involvement and interest of the average person. My personal pet peeve is when pundits interpret consumer sentiment or confidence in stock market terms. Most people simply do not know and are not paying attention.

Michael Johnston (following up on Josh Brown) had an interesting list of comparisons from TV, books, movies and Google searches. How many people do you think could name the Fed Chair? Do more people watch Jim Cramer or Cosmo Kramer? Are people interested in Berkshire Hathaway or Anne Hathaway?

You can probably guess the basic idea, but here is the answer to one question

The Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger. No award this week, despite the abundance of really bad analysis. I am thinking of starting a nominee section. This would include items that have obvious errors but which have not attracted any replies or refutation. Almost any two-variable chart these days is a candidate.

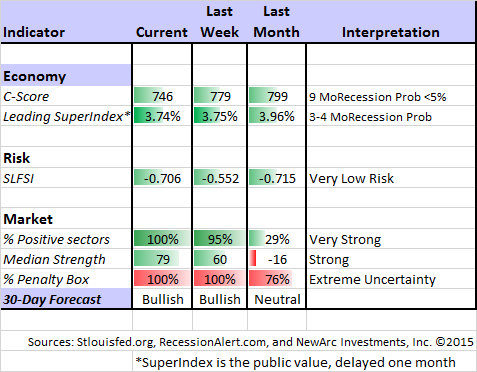

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update.

Recent Expert Commentary on Recession Odds and Market Trends

Bob Dieli does a monthly update (subscription required) after the employment report and also a monthly overview analysis. He follows many concurrent indicators to supplement our featured “C Score.”

RecessionAlert: A variety of strong quantitative indicators for both economic and market analysis. While we feature the recession analysis, Dwaine also has a number of interesting systems. These include approaches helpful in both economic and market timing. He has been very accurate in helping people to stay on the right side of the market.

Georg Vrba: An array of interesting systems. Check out his site for the full story. We especially like hisunemployment rate recession indicator, confirming that there is no recession signal. He gets a similar result from the Business Cycle Indicator.

Doug Short: Provides an array of important economic updates including the best charts around. One of these is monitoring the ECRI’s business cycle analysis, as he does in this week’s update. The ECRI story is becoming repetitive and even more unhelpful. It seems too related to commodity prices, and only slightly changed from their failed recession forecast. It would be refreshing to see them do a complete reset and adopt a fresh approach.

New Deal Democrat has a nice study of retail sales and real consumption expenditures. His take on the data is that we are past the mid-point of the cycle, but that we can expect expansion through Q3 2016. Here is a key chart.

The Week Ahead

It is a pretty normal week for economic data. While I highlight the most important items, you can get an excellent comprehensive listing at Investing.com. You can filter for country, type of report, and other factors.

The “A List” includes the following:

- China GDP (S). Before the market opening on Monday.

- Housing starts and building permits (T). Permits are a good leading indicator.

- Leading indicators (Th). A popular indicator which might slip into negative territory.

- Initial jobless claims (Th). The best concurrent news on employment trends, with emphasis on job losses.

The “B List” includes the following:

- Existing home sales (Th). Not the direct importance of new construction, but still a good read on the market.

- Crude oil inventories (Th). Current interest in energy keeps this on the list of items to watch.

There are several less important reports on housing – the homebuilder’s index, the mortgage index, and FHFA home prices. These will add to the interest in the housing story.

Earnings remain important with plenty of big names on the calendar. Expect more than the normal level of FedSpeak as well.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a “one size fits all” approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix has remained bullish, but with little commitment. The penalty box indicator remains on full tilt so prediction confidence is low. Stay small or not at all. For more information, I have posted a further description — Meet Felix and Oscar. You can sign up for Felix’s weekly ratings updates via email to etf at newarc dot com. Felix appears almost every day at Scutify.

Do things get to “noisy” when you are on a losing streak? Dr. Brett helps you to avoid the “yips.”

Consider holding positions overnight. That is where the action is, and buying the opening may be the worst.

According to Bespoke analyst George Pearkes, the overnight period from the prior market close until 10 a.m. ET offers the best longer-term performance.

“The broad take-away is that the majority of gains have happened when the market wasn’t trading,” Pearkes said in an interview Wednesday. “If you are only trading between 9:30 a.m. and 4 p.m. and going out flat every night, you are missing a huge amount of the overall moves the index is making.”

12 pieces of advice from Paul Tudor Jones (via NewtraderU). All good. “#11 “Don’t be a hero. Don’t have an ego. Always question yourself and your ability. Don’t ever feel that you are very good. The second you do, you are dead.”

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Major market declines occur after business cycle peaks, sparked by severely declining earnings. Our methods are focused on limiting this risk. Start with our Tips for Individual Investors and follow the links.

We also have a page summarizing many of the current investor fears. If you read something scary, this is a good place to do some fact checking.

Other Advice

Here is our collection of great investor advice for this week.

If I had to pick a single most important article, it would be the cover story in this week’s Barron’s. If you are not a regular reader, this might be a good issue to try. Jack Willoughby’s objective report on their biannual poll data. The information was gathered during the recent market correction. There are interesting comments and anecdotal evidence to support each conclusion. Those surveyed are a different group than you often see in other sources – they manage a lot of money and do not generally discuss it on TV. Their conclusions are much more optimistic than the sources commonly followed by investors. They are more bullish about the economy and the stock market, even though they name some of the popular concerns. This table is a nice summary of results, but no substitute for reading the whole article. (There are also articles on wireless real estate companies and financial stocks).

Investor Psychology

The big money conclusions are all in sharp contrast to the high level of skepticism and fear among individual investors. (Bloomberg).

Following meetings with clients in the U.S., Europe and Asia over the past few weeks, we make the following observations: Confusion: Never have we seen so many clients who just do not know what is happening and have cashed up. … The wall of bearishness was extreme in the US – roughly 80 percent of meetings – but much more balanced outside the U.S. (maybe because markets started to rally in the meantime). Often in the U.S., the question was ‘why isn’t this a bear market?’. In Asia, on the other hand, most investors were less concerned about China (though, we have always found the closer you get to China geographically, the less concerned investors are about China).

And similarly from Chuck Jaffe at MarketWatch, citing the high level of investor fear.

Stock Ideas

Energy stocks have lagged the rebound in energy prices. Dana Lyons takes note of the continuing high level of skepticism:

Now eventually, the sector is going to need to see some inflows. That is how rallies are fueled. However, at the onset, bulls want to see enthusiasm at low levels. As long as there is a healthy amount of skepticism, there are potential eventual buyers on the sidelines. This is the proverbial wall of worry.

Chuck Carnevale has done it again, with another great article in his series on retirement investing. This week he covers how to reinvest dividends, and how that differs from dollar cost averaging. He also provides another list of good stock ideas. Chuck’ work should be a regular stop for individual investors, especially those who appreciate methods for finding real value.

The Value Investing Approach

Alpha Architect surveys academic literature that you might not have time to read, providing summaries of important work. This week Wesley R. Gray describes research showing that the value investing approach identifies mispriced stocks and shows solid gains as the pricing returns to normal. You probably knew that, but it is easy to forget when markets are driven by fear or greed.

Personal Finance

Professional investors and traders have been making Abnormal Returns a daily stop for ten year. Congratulations to Tadas for reaching his tenth anniversary – better than ever. The average investor should make time (even if not able to read every day as I do) for a weekly trip on Wednesday. Tadas always has first-rate links for investors in this special edition. As always, there are several great links, but I especially liked these money tips for new or expecting parents. Hint: Despite what Mrs. OldProf told me, it is not cheap!

Market Outlook

Last week I highlighted the bearish Bill Gross. There are also some legendary fund managers who are very bullish.

Leon Cooperman has seven thoughts about the market upside.

Bill Miller thinks it is a perfect time to invest – and he provides a number of his favorite picks.

Watch out for…

An ETF based on social media results? The Market Prophit [sic] Social Media Sentiment Index tracks Twitter, using posts that include a cashtag – a dollar sign preceding the stock symbol. I sense opportunities for manipulation and also outracing the average investor, but we shall see.

A copper price rebound. Rio Tinto’s head of copper opines that prices do not reflect the fundamentals in China. He suggests that too many hedge funds are taking dangerous short positions.

Final Thoughts

I am watching several things next week. I see it as a possible week of opportunity for investors.

China. The China effects are overemphasized, but that may still be the story at the start of the week. It is amazing how much fuss there is over a number that few really believe anyway. This is yet another example of something that will have a trading effect, but is not very important for long-term investors.

Housing. If prices, affordability, and building permits remain strong, this is a happy hunting ground. In my town there is plenty of new construction and also solid demand. Except for a few areas, this story seems typical. Consider construction and home improvement stocks.

Earnings. Here is an idea to help find opportunities. Many companies are citing the effect of a strong dollar. Do you expect dollar strength to continue? At the same pace? Do you have a good reason for that opinion? If not, maybe you should view the dollar strength effects as temporary and do some shopping among companies where this is a theme.

The earnings and housing stories can work for you if you are prepared for the possibilities.