I attended a university that stressed the study of original texts. We read the classic Greek and Roman histories, Newton’s “Principia Mathematica,” and Darwin’s “On the Origin of Species.” We were expected to interpret the meaning of these works for ourselves, as opposed to learning about them through the interpretations of others.

When it came to economic study, then, “An Inquiry Into the Nature and Causes of the Wealth of Nations” was a foundational work. Adam Smith was not the first to describe the operation of markets and the actors within them, but his synthesis of both was path-breaking. Nearly 240 years after its publication, it remains influential.

The creation and influence of wealth within economies has been the subject of special attention since the 2008 financial crisis. In particular, central banks have pursued programs of quantitative easing (QE) with the goal of promoting wealth-producing investments and the “wealth effects” that result from strong market performance.

In general, these efforts have been successful but to differing degrees in different places. Understanding the reasons for these variances can help inform the conduct of monetary policy across nations.

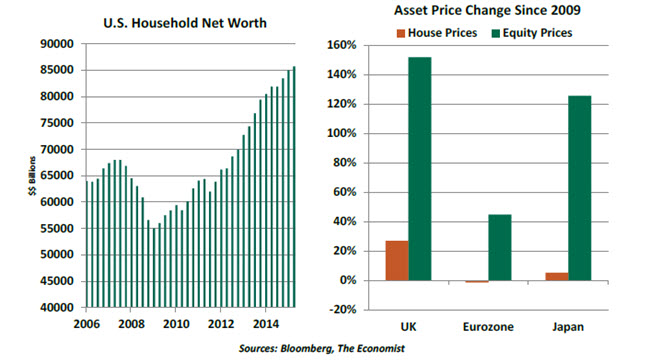

A great deal of wealth was destroyed in 2008. Corrections in the values of equities and homes erased $13 trillion of household net worth in the United States. It might certainly be said that stock and house prices had risen well beyond their fundamental values, but that did not make the retreat any less painful.

Happily, the recovery of asset values across markets since then has been powerful. Led primarily by equity markets, ground lost during the crisis has been regained – and then some.

It is difficult to decompose the contributors to market gains, but some of the progress is certainly due to monetary policy. Bringing interest rates down to (or, in some cases, beyond) the zero lower bound makes real returns on cash negligible or negative. This, in turn, can prompt a reallocation into risk assets; the increased demand results in higher prices for these assets. The QE programs extend on this influence.

All of this may sound very artificial, but there is a method to the madness. Households that see their net worth increasing tend to spend more. Their demand creates jobs, which create more incomes and more consumption. In this way, “wealth effects” can serve as a catalyst for better growth which, in turn, justifies higher asset prices.

Central banks have made little secret of their motivations on this front. But the effectiveness of their efforts depends critically on the composition of household asset holdings and the propensity of those households to consume more when their wealth increases. These factors can vary considerably across markets and time.

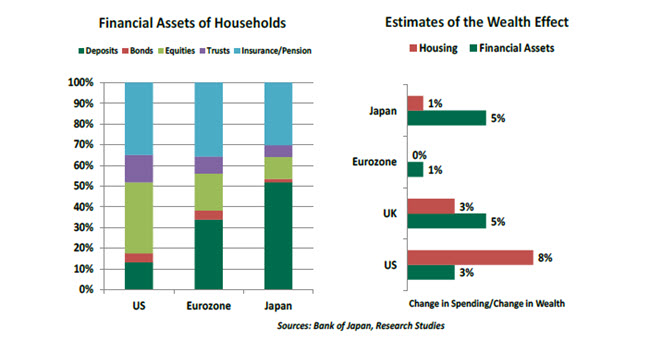

One basic source of difference is the breadth of asset ownership in a given country. If wealth is heavily concentrated, wealth effects will typically be smaller because the wealthy typically have lower propensities to spend. The more democratically the holding of wealth, the more powerful wealth effects are.

The fraction of households that benefitted from the equity market recovery of the last five years varies quite a bit between countries. Further, the structure of these holdings can influence their impact on spending; if held in a structured account like a retirement fund, gains are much less likely to trigger additional outlays.

Once accrued, wealth gains have very different influences across countries. Estimating the influence of increased net worth on spending is very difficult, and the results vary greatly from study to study and over time. For the United States, rates of 3 cents in additional consumption for each dollar gain in financial assets and 8 cents for each dollar gain in home values seem to be common rules of thumb. The analogous figures for the eurozone are much lower.

The ability to liquefy assets plays a role in explaining this divergence. The liberal availability and use of home equity lines may explain why the multiplier on U.S. house price gains is well in excess of that seen elsewhere.

There are suspicions that recent asset price gains are not generating the same level of wealth effects that they have in the past. The correction endured seven years ago may have compromised the ability of households to see gains as lasting. Further, incremental resources are being applied to curtailing debt as opposed to increasing consumption.

The presence of mitigating factors can also blunt the power of wealth effects. In particular, the wealth effects of QE in Japan have been relatively muted. This is due in large part to the strain of increased consumption taxes and the weaker yen on Japanese households.

In sum, QE is not a one-size-fits-all solution. The design of such programs must account for local variances in the ways that wealth is created and applied.

Adam Smith probably would not have approved of using monetary policy to steer asset values and consumption. Such actions stray from reliance on the invisible hand. But markets don’t always function optimally. And in those instances, properly crafted monetary policy can lend a helping hand in those instances.

Watch U.S. Health Care Inflation

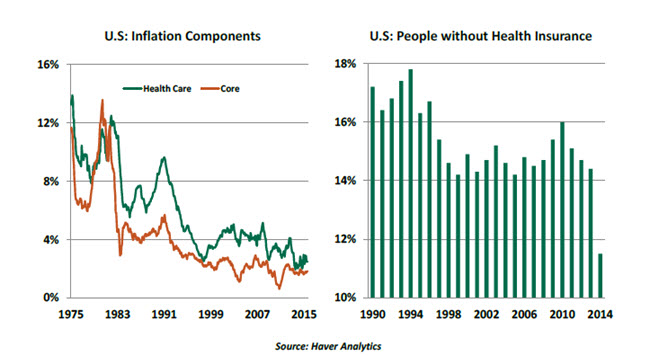

The future path of health care costs in the United States is a source of much debate, and it is largely unsettled. Contained health care inflation has helped to cap overall inflation, despite a six-year-old expansion. Will this favorable trend continue to prevail?

Health care expenditures make up nearly 18% of gross domestic product (GDP), up from 15.5% 10 years ago. They are projected to advance to about 20% of GDP by 2024.

From an inflation perspective, health care prices have slowed significantly. Health care accounts for 10% of the core consumer price index (CPI), which excludes food and energy, and reflects only out-of-pocket expenses. The personal consumption expenditure price index (PCEPI) includes employer costs of providing insurance to employees, Medicare, and Medicaid costs. As a result of this difference, health care is a larger share of PCEPI. The Federal Reserve Bank of Cleveland estimates that health care makes up 25% of core PCEPI (excludes good and energy).

Historically, health care inflation has exceeded overall and core inflation trends. The recent muted trend suggests that health care inflation has been a smaller influence on inflation. Examining the major components of health care goods and services, one finds a widespread deceleration in health care costs, excluding prescription drugs.

Health care services (close to 75%) are a larger share than goods and health insurance in price measures. Medical care services price data (physician services, hospital services) maintain a long-term deceleration that began in 2003.

Containing health care costs is a complex task. The number of uninsured has dropped in the United States since 2014, mostly due to the Affordable Care Act. In general, the reduction of the uninsured helps to trim health care expenses as providers’ costs associated with caring for the uninsured declines.

Looking ahead, there are different factors that can change the promising health care inflation picture. Continued development of high-cost treatments will raise health care inflation. Specialty drug approvals have surpassed those of traditional drugs in the past five years. High-cost drugs for hepatitis C, cystic fibrosis, breast cancer and melanoma are a few examples of the growing trend toward specialty drugs.

The slowdown in health care costs is not visible to the average consumer, as out-of-pocket expenses have risen. The Kaiser Family Foundation estimates that deductibles of the insured have risen 67% in the last five years. A PwC survey shows that 25% of employers offer only high-deductible plans compared with 13% three years ago. High deductibles result in a short-term reduction in demand for medical care. Strong employment conditions can modify this outcome and raise health care costs.

Health organizations are concerned about data breaches, and they have strong incentives to spend on cyber security to avoid the high costs of such events. It is estimated that post-breach costs are 25 times larger than prevention costs. Cyber security costs should contribute to higher health care costs.

Although there is media coverage of off-shoring of medical services, barriers to carrying out these tasks, such as professional licenses, prevent transferring medical diagnostic jobs to cost-effective international centers.

Employment and wage growth in the health care sector are both above-average in recent months. Unless there are major productivity gains, pressure on health care inflation cannot be ruled out. And if it eventually appears, the Federal Reserve might have greater confidence about reaching its 2% inflation target.

Seeing the Little Picture

It’s often said that an economist is someone who thinks that the temperature is fine, on average, if his head is in the freezer and his feet are in the fire. Our tendency to look at things in aggregate, condensing millions of transactions and people into single demand curves, limits our ability to understand what’s going on underneath the mean.

Angus Deaton, a Princeton professor, was awarded the 2015 Nobel Prize in Economics for a lifetime of digging into the details. His work studies the relationship between consumption and income at the micro level through painstaking review of large data sets. Deaton embraced this orientation before computers made it significantly easier to acquire and analyze information.

This approach has won many adherents. A recent extension is the analysis of the U.S. labor force, which looks at micro data to understand why fewer people have been participating. This sort of insight helps to calibrate policy aimed at dealing with the decline.

Deaton has been a stickler for data hygiene. Errors in sampling, data gathering and aggregation can skew raw information and lead to improper conclusions. To limit the impact of these potential imperfections, he rolled up his sleeves and assisted in the design of economic surveys.

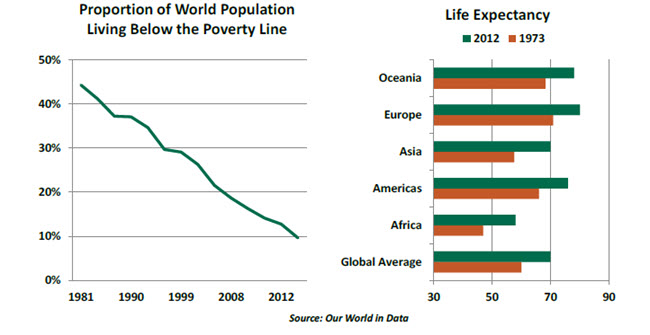

Deaton’s main interest has been in development economics, that branch of our discipline centered on understanding and steering the dynamics of emerging nations. His measurement of poverty and progress featured in his book, “The Great Escape: Health, Wealth, and the Origins of Inequality.” Deaton is encouraged by the progress made in reducing poverty, which has been remarkable over the past generation.

Nonetheless, Deaton frets about expanding levels of income inequality and the pernicious impact it can have on societies. He often found standard prescriptions for developing nations wanting, much to the chagrin of some major foundations working in that space.

This year’s award continues a trend toward recognizing economists who do hard work reconciling data and theory. We hope this trend continues.

(c) Northern Trust