Third Quarter 2015 Economic & Capital Market Summary

There are three essentials to leadership: humility, clarity and courage. —Fuchan Yuan

On the one hand, the domestic economic story is playing out pretty much as we had thought. Economic growth is muddling along in the 2% area. The unemployment rate is low, but job growth is still limited to service sector jobs which pay lower wages. Inflation is barely rising as commodity prices continue to plunge and wage growth has been flat. The Federal Reserve is poised to raise interest rates, but has deferred making the first increase in over nine years under pressure from global economies who fear that an increase in short term interest rates will impair the fragile global growth.

On the other hand, we have entered a new phase of, well, whatever you call this. I guess it’s a recovery. Volatility has increased as the time for the Fed’s rate increase nears. But, it doesn’t really make sense to us that a miniscule interest rate increase that is widely anticipated and mostly symbolic would warrant this level of market volatility. The rapid decline in economic growth in China this past quarter is partly to blame for the heightened volatility. The decline in oil prices has forced restructuring in the energy sector which has weighed on credit markets. Corporate earnings will likely be mixed, but markets over the past two years have shaken off deteriorating fundamentals in earnings. We believe that the increased market volatility, which is warranted, has more to do with the embedded structural problems in our economy and capital markets than anything related to fundamentals. And, it’s about to get more interesting.

The world is a different place today. Small businesses are not able to borrow from banks like the old days. Global deflation is a bigger concern than inflation. The majority of developed countries have all implemented debt backed asset purchase programs to lower interest rates to spur economic growth. The European Union is struggling to govern itself and spur economic growth after wrestling with Greece this last summer. Japan has not experienced sustained economic growth in almost twenty years. We have been dealing with structural problems in our capital markets since the Financial Crisis. In turn, these structural problems have distorted valuations of bonds, stocks, real estate and other assets. With the lack of leadership in Washington DC, these structural problems are here to stay and are a part of our evolving capital markets.

There has been a consistent failure of our elected officials to create a vision for America since the Financial Crisis and there appears to be no significant change on the horizon from what we are seeing from the Republican primary and Congress. Domestically, we have begun the circus which will lead to the next presidential election. At the same time the Republican Party is in disarray with no clear leadership in the House. In the absence of any real leadership or catalyst for change, we expect that nothing meaningful will get done over the next two years in Washington DC.

As our process to elect a president has begun to look more like a made-for-television reality show, the stakes for global leadership are increasing rapidly. The Russians have made their military presence known in Syria in an unveiled initiative to prop up Bashar al-Assad. The Cold War is definitely not over. If Russia isn’t hacking our databases, China is. When pressed last month about cyberattacks during his visit to the United States, President Xi was noncommittal. We expect that China’s economy will begin to stabilize over the near term after slowing every year over the past five years. In addition, we believe that Europe should show growth aided by the European Central Bank’s asset purchase program.

Our investment thesis continues to be one of caution and to approach the capital markets with prudence and discipline. While we expect the domestic economy to continue to grow at a much lower rate, we need to see private credit expansion and business formation. The structural problems in the economy and capital markets have been barriers to economic growth. We have not shown the political will or understanding of the issues to address these structural problems. These include the Dodd-Frank Act, the lack of progress on derivatives and the Volcker Rule, the Affordable-Care Act, the endless fines and the penalties that the banks continue to pay to settle the lawsuits resulting from the Financial Crisis.

Where there is no vision, the people perish. —Proverbs 29:18

The Economy

Following the Financial Crisis, the Federal Reserve implemented a new form of stimulus in which it purchased bonds in the open market to the tune of $4.5 trillion. As we’ve written before, the ramifications of this powerful tool are being felt throughout the capital markets. In our opinion, we would not be experiencing the growth in our economy today if it were not for these programs. But, at the same time, we are not experiencing sustained economic growth.

The domestic economy is experiencing growth, but we would argue that it is still not experiencing sustained economic growth. The domestic economy, measured by GDP, is growing at roughly 2.3% and is showing more balance across manufacturing and the consumer sector. Low interest rates have had a positive impact on the consumer which is illustrated in both the housing and auto sectors during the last quarter.

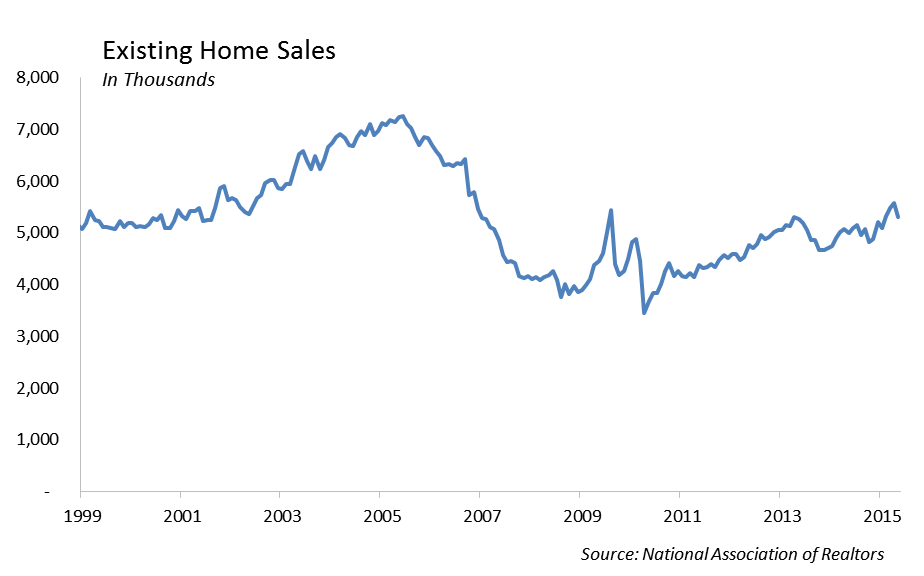

The housing market is an important part of the domestic economy and will likely be negatively impacted by any rise in interest rates. The housing market was hindered by more punitive regulation over the past several years in spite of low interest rates, but now is showing solid growth. Sales of previously owned homes increased 6% year over year since August of last year. In addition, home sales around the country are at their highest level since the recession.

Auto debt owed by U.S. households increased to over $1 trillion for the first time last quarter. The auto industry was brought to its knees during the Financial Crisis, but is now showing that it is an important pillar of the domestic economy. A combination of low interest rates, cheaper gas prices, access to easy credit and pent up demand has brought buyers back into the auto market. So far in 2015, car and light truck sales are on pace to increase above 17 million units this year for the first time since 2001. The concern is that the increase in subprime loans, which are loans to borrowers with lower credit quality, has also increased.

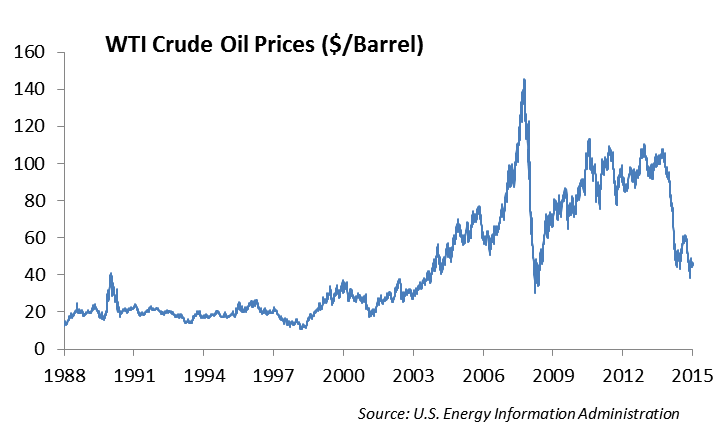

One of the critical issues facing the economy is the price of oil. While the consumer clearly benefits from declining oil prices, it has a negative impact on the energy sector which represents the third largest industry in the United States economy. Billions of dollars in wages as well as potential long-term investments by energy companies rests on the near term price of oil. We are expecting that declining U.S. crude production will eventually put a floor on oil prices; however, those declines have been elusive during the summer. In addition, we expect the new treaty with Iran over their nuclear program will have some oil related import component which will put further pressure on oil prices.

Job Growth Remains a Conundrum

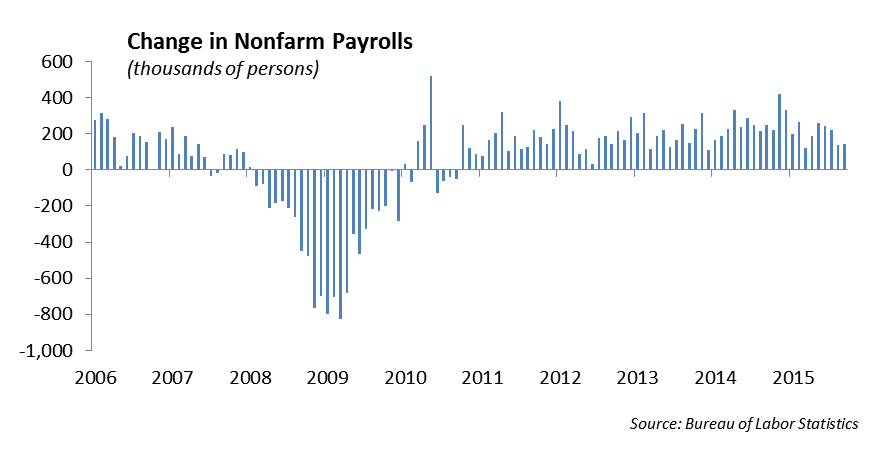

According to the Labor Department, initial jobless claims, an important measure of lay-offs in the economy, hit its lowest level since 1974 last quarter. For those keeping score at home, Richard Nixon was president. So far this year the economy has produced 1.3 million jobs and this growth has helped to push the unemployment rate down to 5.1%.

We expect that employment growth is more than strong enough for the unemployment rate to keep declining. This will provide the foundation for the Federal Reserve’s initiative to raise interest rates still this year. But, the problem remains that the jobs being created are mostly lower level service sector positions which don’t pay as much. Median household incomes are stuck at similar levels seen in the 1990’s and the top 10% of the population controls over three quarters of the wealth in the country. The growing income inequality in the United States is a significant concern as the middle class dream seems further out of reach. The Federal Reserve has acknowledged its concern over the subdued wage growth and the number of Americans that are sitting on the side lines of the labor force.

We would expect that we are close to the point where scarce resources and productivity gains would culminate in wage pressure. We believe the key driver that will allow the economy to move into the next gear is wage growth.

The Global Economy Continues to Slow

The economies of the developed countries are stuck with weak growth, high unemployment and low productivity. There is little prospect on the horizon that will move these economies to accelerate growth. Countries including Japan, Europe and the United Kingdom have implemented large asset purchase programs in an attempt to jump start economic growth. The jury is still out. At the same time, the emerging economies, which have been powerful engines for growth following the Financial Crisis, are slowing or contracting this year. As uncertainty grips the global economy, credit expansion remains impaired as the banks continue to deleverage and capital investment is much weaker than we expected.

China’s economy, the second largest in the world, has been the focus this year as growth continues to slow and their demand for commodities has waned. We expect that China’s growth likely slipped further to 6.8% in the third quarter, and likely missed the government’s growth target for the year. It remains unclear if China can transition their economy to a new growth model that emphasizes consumption from the growing middle class. We don’t think it can do it without serious government support.

Why Rising Interest Rates Matter

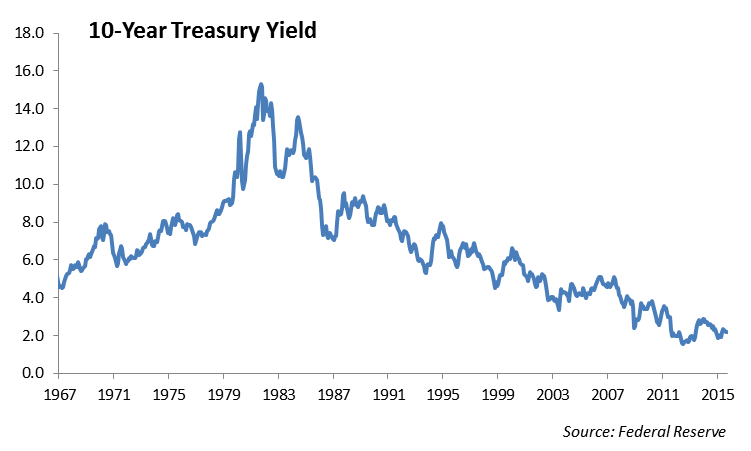

Make no mistake, the Federal Reserve wants to move short term interest rates higher. The Fed has surpassed every milestone it has set to measure progress. Fed Chairwoman Janet Yellen has indicated clearly to the markets that the Fed intends to raise interest rates as long as the economy remains on track and there are no heightened global risks that would impede our economic growth. However, the International Monetary Fund has been outspoken with their concern that attempts to raise interest rates in the United States will derail progress that Europe has made on jump starting its lagging economy. Global interest rates still have not normalized as the yield on the ten year US Treasury is over 25 basis points higher than lower rated Italy and Spain.

The capital markets are shaped much differently than 20 years ago and more bond “inventory” is held in liquid mutual funds and exchange traded funds and no longer at Wall Street firms. The concern is that, as the Fed pushes short-term interest rates higher, investors redeem shares of fixed income mutual funds and Exchange Traded Funds forcing the sale of corporate bonds. Without a natural buyer for the debt, bond prices will experience heightened volatility. In our minds it’s not a question of if it will happen, it’s a question of when it will happen. Investors should expect to experience an increase in volatility in the bond market as the Federal Reserve pushes short term rates higher.

As short term interest rates move higher, we expect the long end to increase to less of a degree. As a result, we would expect the yield curve, measured by the yield on the two year US Treasury and the yield on the 30 year US Treasury to flatten.

Higher interest rates will effectively increase the discount rate for valuation models across all asset classes including equities and real estate. While we expect the yield on the 10 year U.S. Treasury to be range bound between 2.35% and 2.85%, higher rates will lower the valuations for other assets. Ultimately, since U.S. interest rates are already higher than the yields of other developed countries, we expect there will be a natural ceiling to how high interest rates will actually move.

We expect the remainder of the year to be interesting in the capital markets as investors adjust to a shift in Federal Reserve policy. We expect to see interest rates move higher and an increase in market volatility. Our attention in the United States will shift to the election and the dysfunction in Congress. The world’s attention will shift to new diplomatic relations with Iran and lower oil prices, stagnant growth in China, and Russia’s role in the conflict in the Middle East. It’s about to get more interesting.

This report is published solely for informational purposes and is not to be construed as specific tax, legal or investment advice. Views should not be considered a recommendation to buy or sell nor should they be relied upon as investment advice. It does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors. Information contained in this report is current as of the date of publication and has been obtained from third party sources believed to be reliable. WCM does not warrant or make any representation regarding the use or results of the information contained herein in terms of its correctness, accuracy, timeliness, reliability, or otherwise, and does not accept any responsibility for any loss or damage that results from its use. You should assume that Winthrop Capital Management has a financial interest in one or more of the positions discussed. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Winthrop Capital Management has no obligation to provide recipients hereof with updates or changes to such data.

© 2015 Winthrop Capital Management