Is Reserve Bank of India ignoring household inflation expectations?

The Reserve Bank of India (RBI), India’s central bank conducts a quarterly survey of Indian households to gauge their expectations of future inflation. The survey is carried out in nearly 5000 households across 16 cities of India with 30% respondents being housewives. Inflation expectations has played an important role in the new RBI inflation-targeting regime and RBI governor Dr. Raghuram Rajan has alluded to households’ inflation expectations in every policy decision speech he has made as well as in his opening speech upon joining as RBI governor in September 2013. But that was the past.

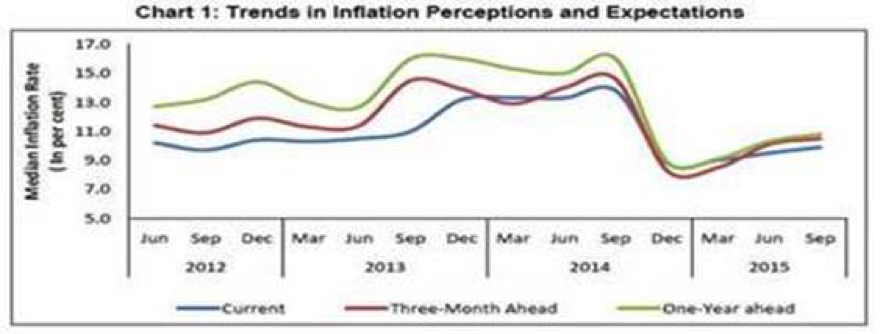

As per data released by RBI a fortnight ago, household inflationary expectations for 3 months ahead rose by half a percentage to 10.5% from June 2015 survey. During the same period, Consumer Price Inflation (CPI) has softened by 100bps and food inflation by around 150bps. Household inflation expectations have remained stubbornly high despite inflation (both retail and wholesale) having cooled off substantially in the last 6 months in India. The wedge between household inflation expectations and actual inflation in India is hard to ignore. The one year ahead inflation expectation is marginally higher than the three month ahead expectations implying households expect inflation trajectory to move further up.

Household Inflation expectations

Expectations of prices three month ahead

Respondents’ profile

Deciphering Dr. Rajan’s commentary

Monetary Policy – Dec-14: Dr. Rajan decided to keep policy rates unchanged at 8%; median household inflationary expectations (three months ahead) was uncomfortably high at 15%

“If the current inflation momentum and changes in inflationary expectations continue, and fiscal developments are encouraging, a change in the monetary policy stance is likely early next year, including outside the policy review cycle”

Data for survey carried out in December 2014 was published on January 15th, 2015; household inflationary expectations had come down by 630bps on a sequential basis in 3 months. RBI swung into action and reduced interest rates by 25bps outside the cycle.

However, in the Jun-15 monetary policy when Dr. Rajan cut rates by another 25bps, household inflationary expectations were on the rise and this is what he had said:

“Inflation expectations remain in high single digits, although they may adapt further to current low inflation”

In September 2015, RBI delivered a bazooka 50bps rate cut, surprising everyone. This was despite three month ahead inflationary expectations rising ~60bps on a sequential basis. This is what the RBI governor had to say about a sharp increase in food prices in months preceding September 2015:

“They will have to be carefully monitored as they tend to be sticky and impart an upward bias to inflation and inflation expectations. This assumes significance in view of households’ inflation expectations rising again”

There are reasons to believe that the RBI may have started to ignore household inflation expectation data in its anchoring of inflation. Governor Rajan has repeatedly underlined the importance of managing inflation expectations but the pertinent question is whether he has shifted focus on actual inflation trajectory instead of surveyed expectations? And will the RBI’s stance hurt the nascent financial savings creation in India?

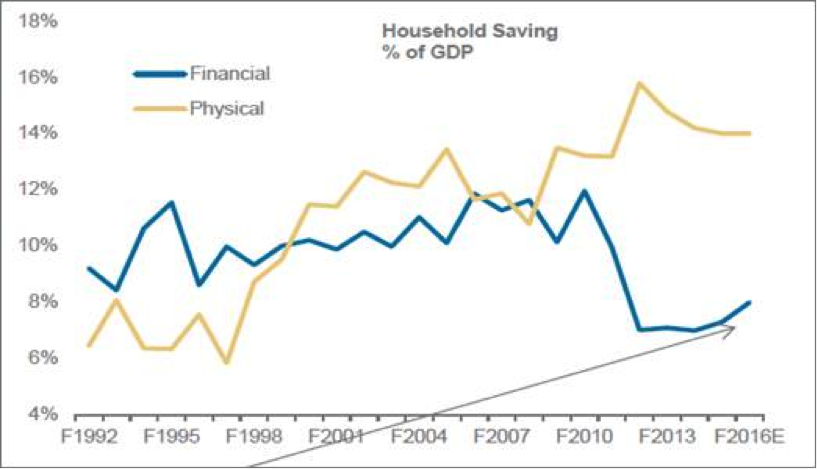

Household Savings trend

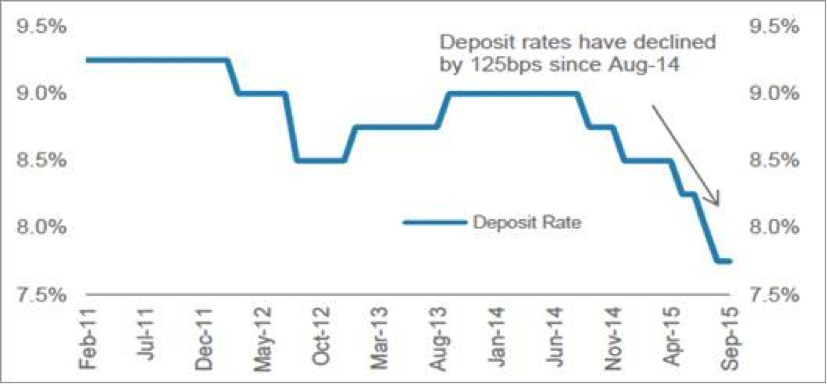

Deposit Rate: SBI

State Bank of India (SBI) is India’s largest bank with a market share of 16%

Dr. Rajan has repeatedly said he intends to maintain real interest rates of 1.5-2%; he wants to incentivize savers to invest in financial assets by providing them with real interest rates. Post 2008, a lot of incremental household savings moved into physical assets (real estate & gold). Household inflation expectations are a very important indicator of changes in financial saving patterns and without any doubt Dr. Rajan understands this more than anybody else. But since the governor has cut interest rates without household inflation expectations coming down, the question that needs to be asked is whether it is a premature move by the governor? Will it discourage households even before the nascent recovery in financial savings gets a chance to mature into a longer term trend? Uneven monetary policy transmission by banks has done little to help; banks have been reluctant to reduce their lending rates in a benign credit off take scenario while mimicking monetary policy action in their deposit rates. Leading banks have cut their deposit rates for up to one year bucket by 100-125bps in 2015 effectively matching RBI’s moves. On the other hand, despite under pressure from RBI, banks reduced their base lending rates by less than half of policy action thereby diluting monetary policy transmission. Moreover, lenders hiked the spread for new mortgage borrowers by 10-15 bps effectively diluting the base rate cut further. If deposit growth falters hereon, we will be looking at one more round of financial savings lost to other forms of investment. India’s household savings are at a nascent stage of recovery after already having lost half a decade of precious savings to physical assets leading to a real estate bubble. Household investment in financial assets has shrunk from roughly 11.5% of India’s GDP in 2007 to ~7.5% now. For a nation whose industry has historically suffered from high cost of capital, this does not bode well.